Years of War

How central banks are reacting and implications for markets

On Feb. 24, 2022, exactly 1 year ago Russia invaded Ukraine. One year later, Russian support is consolidating as Putin leads the country into its second year of war. To bolster support, his government has doled out cash payments to citizens in the country's impoverished regions and shut down the few remaining media outlets that questioned official version of events. Although casualties have reached tens of thousands, a majority of Russians say they are ready to continue fighting, according to independent polls (just in case they are). Tensions spread to Belarus, which is being pulled in for provocation by both sides: when there is war, propaganda is rampant. Now it is Moldova's turn, with the tense situation in Transnistria: any excuse is good to blow the wind of conflict. Although there are rumors of possible secret negotiations in neutral ground (Switzerland), today we are one year into the invasion and nothing has changed. Attrition of deployments is evident, losses numerous, entire territories destroyed, migration flows amplified, complications in air routes, commodity crisis, and inflation still galloping.

What is happening in the heart of Europe? Will Eurozone be able to avoid recession? How will central banks try to stem this?

Il 24 Febbraio 2022, esattamente 1 anno fa la Russia invadeva l’Ucraina. Un anno dopo, il sostegno russo si sta consolidando mentre Putin conduce il Paese verso il secondo anno di guerra. Per sostenere l'appoggio, il suo governo ha elargito pagamenti in contanti ai cittadini delle regioni impoverite del Paese e ha chiuso i pochi media rimasti che hanno messo in discussione la versione ufficiale degli eventi. Sebbene le vittime abbiano raggiunto le decine di migliaia, la maggioranza dei russi si dice pronta a continuare a combattere, secondo sondaggi indipendenti (nel caso lo fossero). Le tensioni si allargano alla Bielorussia che viene tirata in mezzo per provocazione dall’una e dall’altra parte: quando c’è guerra la propaganda è dilagante. Adesso è il turno della Moldavia, con la tesa situazione in Transnistria: ogni scusa è buona per soffiare sul vento del conflitto. Sebbene si spargono voci di possibile segreto negoziato in terra neutra (Svizzera), oggi siamo giunti ad un anno dall’invasione e nulla è cambiato. Il logoramento degli schieramenti è evidente, le perdite numerose, interi territori distrutti, flussi migratori amplificati, complicazioni nelle tratte aeree, crisi delle materie prime e un inflazione ancora galoppante.

Cosa sta succedendo nel cuore dell’Europa? Riuscirà l’Eurozona ad evitare la recessione? Come le banche centrali cercheranno di arginare tutto ciò?

How Germany tries to stand up to recessionary winds

The German economy has been more resilient despite a long series of crises in 2022 threatened to push it into a deep recession. The reason for this resilience is Black-Zero policies and government's massive funding toward businesses. For nearly 20 years, Germany has been pushing with a fiscal stimulus no one can afford in Europe, and which is regularly criticized by other countries: having enjoyed three defaults in its history has been a major factor in ensuring this. The mild climate, introduction of price cap and a series of interventions aimed at containing rising cost of commodities in the first phase of the war played another key role. Will be enough? Let’s dig in.

Contrary to popular belief and to what German governments have often preached to other European governments, genuine fiscal stimulus is preferred in times of crisis. This was the case during financial crisis, the pandemic and now as a response to the war and energy crisis. Germany has perfected the use of big figures shot into the headlines to analysts and macro-economists; these had expected impact, hope that in the end all money promised would not have to be used. During pandemic, the actual fiscal stimulus amounted to more than 10% of GDP. Last year, after a few months of hesitation, the government decided to adopt several stimulus and restraint packages, amounting to about 8% of GDP, as well as a 65 billion aid plan for citizens and businesses launched at the end of 2022.

The reading of ZEW and IFO indices is good news touches on business sentiment and is part of a picture of gradually improving confidence. At the same time, however, there is no cause for celebration. The second consecutive decline in current valuations suggests the economy could see another quarter of economic contraction. In addition, we should not forget since last summer there has been something of a disconnect between economy (data) and finance (company valuations): markets up and major DAX40 stocks up but earnings down and expectations revised down. It should be mentioned for the record despite the sharp decline in confidence indicators, German economy grew in the third quarter of 2022 and even the small contraction in the fourth should have been much stronger judging by indicators. In essence, negative data but better than expected as only Wall Street knows how to do in times of earnings release. Looking forward, question is whether the recent improvement in leading indicators will really translate into positive hard data or whether we may not first see a reversal from last year, i.e., good improving data but disappointing hard data.

In more general terms, latest improving data suggests that German and eurozone economies are in the midst of a typical cyclical recovery. I fear that all these favorable winds are temporary, however. Any recovery this year will be less frothy than markets expect and short-lived, with subdued growth rather than a strong recovery. This is my baseline scenario I’ve reported in previous letters. The expectation of a good year on my part is confirmed by current levels well above the opening of DAX index in the 13850 area: to think we are in the midst of an economic boom from the current levels (15,500 points) really seems to me to be something incredible, which must necessarily be re-balanced. Not falling off the cliff is one thing, staging a strong rebound, however, is a different matter. In Germany, industrial orders have weakened since the beginning of 2022, consumer confidence, despite some recent improvements, is still near record lows, the loss of purchasing power will continue in 2023, and full impact of monetary tightening has yet to manifest itself. China's reopening and lower wholesale gas prices are clearly positive effects, but they may be transitory and overstated.

Come la Germania prova a resistere ai venti recessivi

L'economia tedesca è stata più resistente nonostante una lunga serie di crisi nel 2022 che hanno minacciato di spingerla in una profonda recessione. La ragione di questa resilienza è da ricercare nelle politiche Black-Zero e dall’imponente finanziamento del governo verso le imprese. Da quasi 20 anni la Germania spinge con uno stimolo fiscale che nessuno può permettersi in Europa, e che viene criticato regolarmente dagli altri paesi: aver usufruito di tre default nella sua storia è stato un fattore determinante per garantire tutto questo. Un altro ruolo fondamentale lo ha giocato il clima mite, l’introduzione del price cap e una serie di interventi mirati a contenere il costo galoppante delle materie prime nella prima fase della guerra. Basterà? Scaviamo a fondo.

Contrariamente a quanto si crede e a quanto i governi tedeschi hanno spesso predicato agli altri governi europei, in tempi di crisi si preferisce lo stimolo fiscale vero e proprio. È stato così durante la crisi finanziaria, la pandemia e ora come risposta alla guerra e alla crisi energetica. La Germania ha perfezionato l'uso di grandi cifre sparate in prima pagina ad analisti e macro-economisti; queste hanno avuto l’impatto atteso, nella speranza che alla fine non si doveva utilizzare tutto il denaro promesso. Durante la pandemia, lo stimolo fiscale vero e proprio ammontava a più del 10% del PIL. L'anno scorso, dopo alcuni mesi di esitazione, il governo ha deciso di adottare diversi pacchetti di stimolo e di contenimento dei prezzi, pari a circa l'8% del PIL, oltre ad un piano di aiuti a cittadini e imprese da 65 miliardi varati alla fine del 2022.

La lettura dei vari indici ZEW e IFO è una buona notizia che tocca con mano il sentiment delle imprese e si inserisce in un quadro di graduale miglioramento della fiducia. Allo stesso tempo, però, non c'è motivo di festeggiare. Il secondo calo consecutivo delle valutazioni attuali suggerisce che l'economia potrebbe vedere un altro trimestre di contrazione economica. Inoltre, non dobbiamo dimenticare che dall'estate scorsa si è verificata una sorta di scollamento tra l’economia (i dati) e la finanza (quotazioni delle aziende): mercati su e i principali titoli del DAX40 al rialzo ma utili in calo e aspettative riviste al ribasso. Va ricordato ad onor di cronaca che, nonostante il forte calo degli indicatori di fiducia, l'economia tedesca è cresciuta nel terzo trimestre del 2022 e anche la piccola contrazione nel quarto avrebbe dovuto essere molto più forte a giudicare dagli indicatori. In sostanza, dati negativi ma migliori delle aspettative come solo Wall Street sa fare in tempi di rilascio degli utili. In prospettiva, la domanda è se il recente miglioramento degli indicatori anticipatori si tradurrà davvero in dati concreti positivi o se non si possa prima assistere a un'inversione di tendenza rispetto all'anno scorso, ovvero a dati buoni in miglioramento ma dati concreti deludenti.

In termini più generali, l'ultimo miglioramento dei dati suggerisce che l'economia tedesca e quella dell'eurozona si trovano nel mezzo di una tipica ripresa ciclica. Temo che tutto questi venti favorevoli siano però temporanei. L'eventuale ripresa di quest'anno sarà meno spumeggiante di come i mercati si aspettano e di breve durata, con una crescita contenuta piuttosto che una forte ripresa. Questo è il mio scenario di base che ho riportato nelle precedenti lettere. L’aspettativa di un anno positivo da parte mia è confermata dai livelli attuali ben superiori all’apertura dell’indice tedesco DAX in area 13850: pensare di essere in pieno boom economico dai livelli attuali (15,500 punti) mi sembra davvero un qualcosa di incredibile, che va necessariamente ri-bilanciato. Non cadere dal precipizio è una cosa, mettere in scena un forte rimbalzo, tuttavia, è una questione diversa. In Germania, gli ordini industriali si sono indeboliti dall'inizio del 2022, la fiducia dei consumatori, nonostante alcuni recenti miglioramenti, è ancora vicina ai minimi storici, la perdita di potere d'acquisto continuerà nel 2023 e il pieno impatto della stretta monetaria deve ancora manifestarsi. La riapertura della Cina e la riduzione dei prezzi del gas all'ingrosso sono chiaramente degli effetti positivi, ma potrebbero essere passeggeri e sopravvalutati.

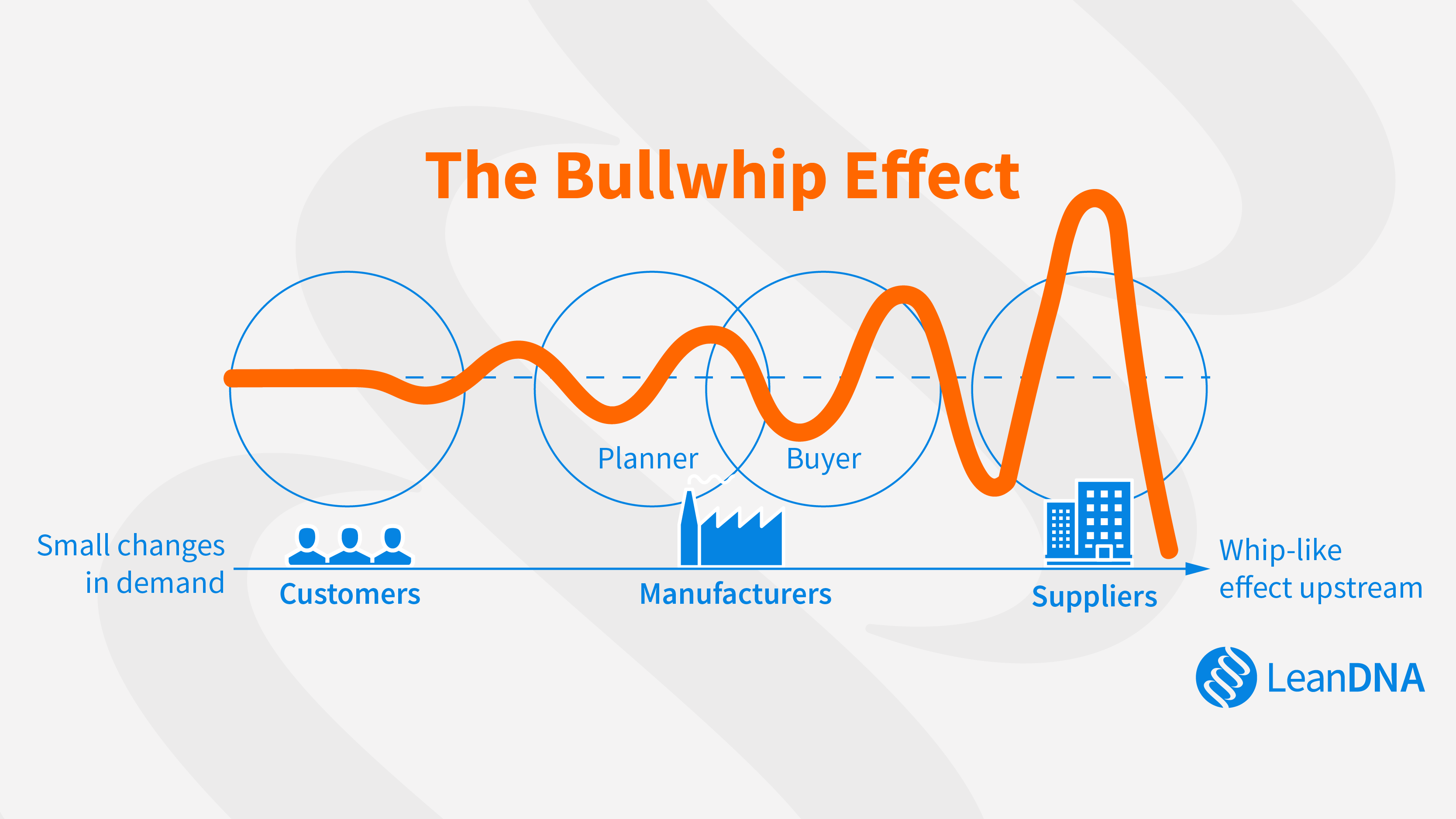

Bullwhip effect in the Eurozone

The past few years have been crazy times for warehouse stock managers. After a long trend of declining inventory-to-sales ratios, thanks to more integrated supply chains and just-in-time management, pandemic proved to be a brutal wake-up call. Suddenly, companies were faced with disrupted supply chains and input shortages. And this was at a time when consumers spent much more on goods (especially durables) because consumption of services was hampered by shutdowns. The rush for inputs, fostered by a new just-in-case-management philosophy, may even have led to a «bullwhip effect» (which Michael J. Burry has discussed in the past): a situation in which firms, in the wake of uncertainty, order more inputs than they actually need. This has obviously promoted economic growth. Fully filled warehouses, rising cost of working capital and the gradual return of just-in-time management will likely weigh on inventory accumulation in the coming months. This will be a modest headwind for economic growth in the first half of the year.

However, beginning in late 2021, consumer demand began to soften due to rising energy prices, and as the pandemic wore off, there was a gradual shift from consumption of goods to consumption of services. People preferred to go on vacation or dine at restaurants rather than spend money on yet another piece of fitness equipment for the home gym in the attic. Not surprisingly, assessment of inventory levels at factories and retailers, thought to be low at the end of 2021, is now quite high. With a reduction in supply chain snags and lead times, there is also less need to keep inventory levels high. In addition, significant increase in the cost of working capital, courtesy of ECB's tightening, is pushing companies to be more efficient in inventory management. The latest data for February signaled a sharp decline in factory purchases as companies remained focused on reducing inventories.

L’effetto «bullwhip» nell’Eurozona

Gli ultimi anni sono stati tempi folli per i gestori di stock di magazzino. Dopo una lunga tendenza alla diminuzione del rapporto scorte/vendite, grazie a catene di fornitura più integrate e alla gestione just-in-time, la pandemia si è rivelata un brutale campanello d'allarme. Improvvisamente le aziende si sono trovate di fronte a catene di approvvigionamento interrotte e a carenze di fattori produttivi. E questo in un momento in cui i consumatori hanno speso molto di più per i beni (soprattutto quelli durevoli), perché il consumo di servizi è stato ostacolato dalle chiusure. La corsa ai fattori produttivi, favorita da una nuova filosofia di "just-in-case-management", potrebbe persino aver portato a un «effetto bullwhip» (di cui ha parlato Michael J. Burry in passato): una situazione in cui le imprese, sulla scia dell'incertezza, ordinano più fattori produttivi di quelli di cui hanno effettivamente bisogno. Ciò ha ovviamente favorito la crescita economica. I magazzini completamente pieni, l'aumento del costo del capitale circolante e il graduale ritorno della gestione just-in-time peseranno probabilmente sull'accumulo di scorte nei prossimi mesi. Questo sarà un modesto vento contrario per la crescita economica nella prima metà dell'anno.

Tuttavia, a partire dalla fine del 2021 la domanda dei consumatori ha iniziato ad attenuarsi a causa dell'aumento dei prezzi dell'energia e, con l'esaurirsi della pandemia, si è verificato un graduale spostamento dal consumo di beni a quello di servizi. Le persone hanno preferito andare in vacanza o cenare al ristorante piuttosto che spendere soldi per l'ennesimo attrezzo da fitness per la palestra di casa in soffitta. Non c'è da stupirsi che la valutazione dei livelli di scorte presso le fabbriche e i rivenditori, ritenuti bassi alla fine del 2021, sia ora piuttosto alta. Con una riduzione degli intoppi della catena di approvvigionamento e dei tempi di consegna, c'è anche meno bisogno di tenere alti i livelli di scorte. Inoltre, il significativo aumento del costo del capitale circolante, per gentile concessione della stretta della BCE, sta spingendo le aziende ad essere più efficienti nella gestione delle scorte. Gli ultimi dati di Febbraio hanno segnalato un forte calo degli acquisti da parte delle fabbriche, in quanto le aziende sono rimaste concentrate sulla riduzione delle scorte.

Markets are made to surprise

Financial markets as usual do what they do best: frustrate people. Everyone thought Q1 2023 would be negative and Q2 positive, but to fool everyone, what might happen is exactly the opposite. Traders and investors have been crushed by the «Fear of Missing Out» (FOMO) phenomenon and on false expectations of an impending Fed pivot may not see this year. As central banks become even more hawkish and restrictive as economies slow to adjust to rate stimulus, headline inflation remains persistently higher and Fed Funds are beginning to price in something different than the fairy tale expectations being told every day by stock values.

None of those on the upside seem to be comfortable. This is what comes out of reading the Cot Report and option positioning of traders on the world's major assets. Those who are down (like me) are distressed but confident that something is about to happen. What is perplexing is the speed and frequency with which public opinion (as ZeroHedge does for example) shifts its focus to what might crash the market, leaving out anything might hold it back. It’s a game of mind: when you are in position you see only what you would like to see. The list of concerns is long, this is true, but it is also true that we have discussed them ad nauseam and financial markets are no longer as sensitive as they used to be to macro data. Sometimes correlations stop working: this historical period seems to be one of those cases.

I mercati sono fatti per sorprendere

I mercati finanziari come al solito, fanno quello che sanno fare meglio: frustrare le persone. Tutti pensavano che il Q1 2023 fosse negativo e il Q2 positivo, ma per fregare tutti, ciò che potrebbe accadere è esattamente il contrario. Trader e investitori sono rimasti schiacciati dal fenomeno «Fear of Missing Out» (FOMO) e sulle false aspettative di un imminente pivot della Federal Reserve che forse non vedremo quest’anno. Mentre le banche centrali diventano ancora più falco e restrittive, a causa delle economie che tardano ad adeguarsi agli stimoli dei tassi, l’inflazione globale rimane persistentemente più alta e i Fed Funds iniziano a prezzare qualcosa di diverso rispetto alle attese da favola che viene raccontata ogni giorno dai valori delle azioni.

Nessuno di quelli che sono al rialzo sembra essere a proprio agio. Questo è quello che viene fuori dalla lettura del Cot Report e dal posizionamento in opzioni degli operatori sui principali asset mondiali. Quelli che sono al ribasso (come me) sono in sofferenza ma confidenti che qualcosa stia per accadere. L’aspetto che lascia perplessi è la velocità e la frequenza con cui l’opinione pubblica (come fa ZeroHedge ad esempio) sposta l’attenzione su ciò che potrebbe far crollare il mercato, tralasciando tutto quello che potrebbe trattenerlo. E’ un gioco della mente: quando sei in posizione vedi solo quello che vorresti vedere. L’elenco delle preoccupazioni è lungo, questo si, ma è anche vero che ne abbiamo discusso fino alla nausea e che i mercati finanziari non sono più sensibili come prima ai dati macro. A volte le correlazioni smettono di funzionare: questo periodo storico sembra uno di quei casi.

ECB hawks don't let up

The European Central Bank's policy has become restrictive. In my opinion, impact on the economy is probably one of the most underestimated things for 2023. Just think of banking sector yields, on wings of enthusiasm for the return of profitability on rates. Last summer, when ECB began raising interest rates, markets immediately wondered how far Bank would dare to go. Ending an era of negative interest rates and unconventional monetary policy when inflation approaches 10% is one thing, but actively destroying the economy is another. With an interest rate hike of 300 basis points, as ECB has done so far, and with more hikes on the way, question is not if cycle of hikes will slow down Eurozone economy, but rather when.

If we look at asset prices, we notice that stocks and bonds have corrected significantly in 2022. Bank rates have also risen considerably since beginning of 2022: this is beginning to dampen investment, as growth in bank lending has almost stopped for households and is significantly negative for businesses. Traditionally, business loans react with a greater lag to rising rates than consumer loans. As we know actual impact of monetary policy on real economy has always been difficult to calculate. In theory, it is assumed it takes 9 to 12 months for monetary policy to affect the real economy more. Recently, some central bankers have suggested the lag may currently be shorter than in the past. In any case, transmission of monetary policy can often be clouded by other factors.

At the current juncture, energy crisis is playing an important role in slowing the economy and has also helped ease inflation as recent developments have caused gas and electricity prices to fall from their peaks. Supply chain problems have eased recently and demand for goods has weakened (as we saw earlier), helping to rebalance supply and demand in goods markets. It is therefore too early to declare victory over price trends. Wage growth also continues to rise cautiously. Although not enough to raise concerns about a wage-price spiral, labor market remains hot and wage growth as well: supply and demand in labor markets therefore still need to adjust.

In conclusion, many things are moving in the right direction for ECB to bring inflation back on target, but uncertainty remains. No one knows how persistent inflation will be. There is also uncertainty about how long it will take for GDP and inflation to be impacted by ECB's aggressive rate hikes to date. Having recently moved to a more restrictive level and having more hikes planned, I think it will be very difficult for the economy to recover. Although all eyes are currently on the rate hike and liquidity withdrawal, any meaningful recovery and this market rally will see its end or at least a pause.

I falchi della BCE non demordono

La politica della Banca Centrale Europea è diventata restrittiva. A mio avviso, l'impatto sull'economia è probabilmente una delle cose più sottovalutate per il 2023. Basti pensare ai rendimenti del settore bancario, sulle ali dell’entusiasmo per il ritorno di redditività sui tassi. La scorsa estate, quando la BCE ha iniziato ad aumentare i tassi di interesse, i mercati finanziari si sono subito chiesti fino a che punto la Banca avrebbe osato spingersi. Porre fine a un'era di tassi d'interesse negativi e di politica monetaria non convenzionale quando l'inflazione si avvicina al 10% è una cosa, ma distruggere attivamente l'economia è un'altra. Con un aumento dei tassi di interesse di 300 punti base, come ha fatto finora la BCE, e con altri aumenti in arrivo, la questione non è se il ciclo di aumenti rallenterà l'economia dell'Eurozona, ma piuttosto quando.

Se guardiamo ai prezzi degli asset, notiamo che le azioni e le obbligazioni hanno subito una correzione significativa nel 2022. Anche i tassi bancari sono aumentati considerevolmente dall'inizio del 2022: ciò sta iniziando a frenare gli investimenti, poiché la crescita dei prestiti bancari si è quasi arrestata per le famiglie ed è notevolmente negativa per le imprese. Tradizionalmente, i prestiti alle imprese reagiscono con un ritardo maggiore all'aumento dei tassi rispetto ai prestiti ai consumatori. Come sappiamo l’impatto effettivo della politica monetaria sull'economia reale è sempre stata difficile da calcolare. In teoria si presume che siano necessari dai 9 ai 12 mesi prima che la politica monetaria influisca maggiormente sull'economia reale. Recentemente, alcuni banchieri centrali hanno suggerito che il ritardo potrebbe essere attualmente più breve che in passato. In ogni caso, la trasmissione della politica monetaria può spesso essere offuscata da altri fattori.

Nell'attuale congiuntura, la crisi energetica sta giocando un ruolo importante nel rallentare l'economia e ha anche contribuito ad alleggerire l'inflazione, poiché i recenti sviluppi hanno fatto sì che i prezzi del gas e dell'elettricità scendessero dai loro picchi. I problemi della catena di approvvigionamento si sono attenuati di recente e la domanda di beni si è indebolita (come abbiamo visto prima), contribuendo a riequilibrare l'offerta e la domanda nei mercati dei beni. È quindi troppo presto per dichiarare vittoria sull'andamento dei prezzi. Anche la crescita dei salari continua a salire con cautela. Anche se non abbastanza da destare preoccupazioni per una spirale salari-prezzi, il mercato del lavoro rimane caldo e la crescita salariale anche: l'offerta e la domanda nei mercati del lavoro devono quindi ancora adattarsi.

In conclusione, molte cose si stanno muovendo nella direzione giusta per la BCE per riportare l'inflazione all'obiettivo, ma l'incertezza rimane. Nessuno sa quanto sarà persistente l'inflazione. C'è anche incertezza su quanto tempo ci vorrà perché il PIL e l'inflazione subiscano l'impatto degli aggressivi rialzi dei tassi effettuati finora dalla BCE. Essendo passata di recente ad un livello più restrittivo e avendo in programma altri rialzi, ritengo che sarà molto difficile per l’economia riprendersi. Anche se al momento tutti gli occhi sono puntati sull’aumento dei tassi e sul ritiro della liquidità, qualsiasi ripresa significativa e questo rally di mercato vedrà la sua fine o quantomeno una pausa.