Too late to Buy, Too early to Short

Why the cost of waiting erodes returns as markets continue to hit new all-time highs

There is a feeling shared by every investor, regardless of experience, capital or level of technical expertise: the constant sense of arriving too late. It is a thought inevitably surfaces whenever markets are at all-time highs, when markets keep breaking records and general impression is that we are facing something «can’t last much longer». It is an extremely human, almost instinctive perception, because our brains are naturally inclined to view any prolonged movement as something destined, sooner or later, to revert to the mean. The problem is that financial markets, especially stocks, don’t operate according to the psychological concept of normality we use in everyday life.

A stock index is not a static entity; it is not a fixed asset over time, nor is it merely a snapshot of the economy at a specific historical moment. Instead, it is a dynamic, ever-changing entity, driven by nominal growth of the global economy, monetary expansion, rising productivity, technological innovation and above all, capitalism’s ability to continually adapt to the crises it faces. And this is exactly where one of the modern investor’s most costly mistakes arises.

Esiste una sensazione che accomuna praticamente ogni investitore, indipendentemente dall’esperienza, dal capitale o dal livello di preparazione tecnica: la sensazione costante di essere arrivati troppo tardi. È un pensiero che emerge puntualmente ogni volta che i mercati si trovano sui massimi storici, quando gli indici continuano a macinare record e l’impressione generale diventa quella di trovarsi davanti a qualcosa che «non può durare ancora a lungo». È una percezione estremamente umana, quasi istintiva, perché il nostro cervello è naturalmente portato a considerare ogni movimento eccessivamente esteso come qualcosa destinato prima o poi a ritornare verso la media. Il problema è che i mercati finanziari, soprattutto quelli azionari, non ragionano secondo il concetto psicologico di normalità che utilizziamo nella vita quotidiana.

Un indice azionario non è un oggetto statico, non è un bene immobile nel tempo e non è nemmeno una semplice fotografia dell’economia in un preciso momento storico: è invece un qualcosa di dinamico, in continua trasformazione, alimentato dalla crescita nominale dell’economia globale, dall’espansione monetaria, dall’incremento della produttività, dall’innovazione tecnologica e soprattutto dalla capacità del capitalismo di adattarsi continuamente alle crisi che esso stesso attraversa. Ed è proprio qui che nasce uno degli errori più costosi dell’investitore moderno.

The cost of waiting

When markets rise too high, average investor stops thinking in terms of probabilities and starts thinking in terms of emotions. They look at the S&P500 chart, see a line appears too steep, read about high multiples, hear constant talk of euphoria, speculative bubbles, Artificial Intelligence, concentration of returns and valuations spiraling out of control and slowly come to believe entering the market at that moment would inevitably mean exposing themselves to an imminent crash.

The result is that they stand still, wait, and put it off. They convince themselves it is wiser to wait for a 10% correction, perhaps 20%, maybe even 30%, because after all, «it will come sooner or later». Meanwhile, market continues to rise and as it does, psychological unease of those who stayed on the sidelines also grows, because at that point the problem is no longer just the fear of losing money by entering too late, but also the frustration of seeing market move in the expected direction without having taken part in it.

Il costo dell’attesa

Quando i mercati salgono troppo, l’investitore medio smette di ragionare in termini probabilistici e inizia a ragionare in termini emotivi. Guarda il grafico dell’S&P500, vede una linea apparentemente troppo verticale, legge multipli elevati, sente parlare continuamente di euforia, di bolle speculative, di Intelligenza Artificiale, di concentrazione dei rendimenti, di valutazioni fuori controllo e lentamente sviluppa la convinzione che entrare in quel momento significhi necessariamente esporsi a un crollo imminente.

Il risultato è che rimane fermo, aspetta, rimanda. Convince sé stesso che sia più prudente attendere una correzione del 10%, magari del 20%, forse addirittura del 30%, perché in fondo «prima o poi arriverà». Nel frattempo il mercato continua a salire, e mentre lo fa, cresce anche il disagio psicologico di chi è rimasto fuori, perché a quel punto il problema non è più soltanto la paura di perdere denaro entrando troppo tardi, ma diventa anche la frustrazione di vedere il mercato andare nella direzione prevista senza averne preso parte.

Just a little bit of market history

This pattern has repeated itself cyclically for over a century. In 1995, many investors were convinced that Wall Street was now overvalued. In 1996, Alan Greenspan spoke openly of «irrational exuberance», suggesting markets had reached levels were excessive relative to fundamentals. In 1998, after years of uninterrupted gains, consensus was already beginning to describe the U.S. market as a giant bubble ready to burst. Yet, from that point until its peak in 2000, Nasdaq would still multiply its value in an impressive manner.

The exact same pattern repeated itself in the period following the 2008 crisis. In 2013, many investors considered S&P500 too expensive because it had already doubled from the lows of the financial crisis. In 2015, there was constant talk of the end of the cycle. In 2017, market seemed to be rising without volatility and this was interpreted as a clear sign of an imminent collapse. In 2021, the dominant theme was post-pandemic speculative excess. In 2024 and 2025, debate shifted to the concentration of tech mega-caps and risk that the entire U.S. market had become dependent on a few companies tied to artificial intelligence. But central point remains the same: in most cases, market continues to rise for much longer than investors believe possible.

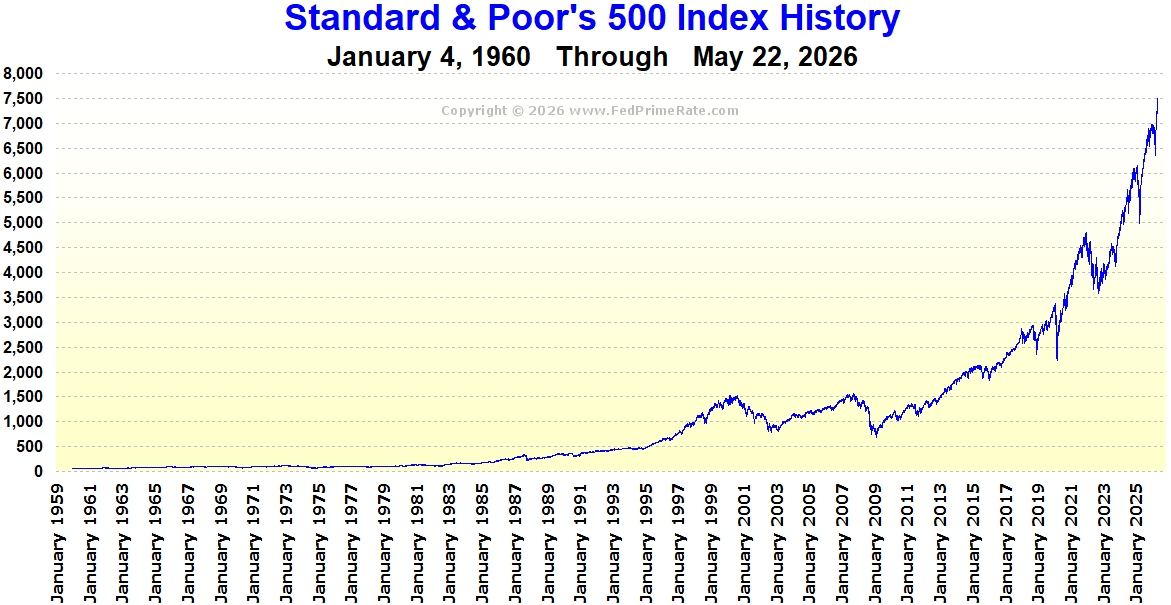

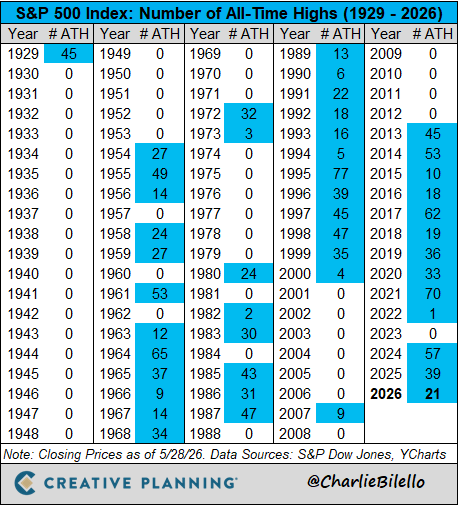

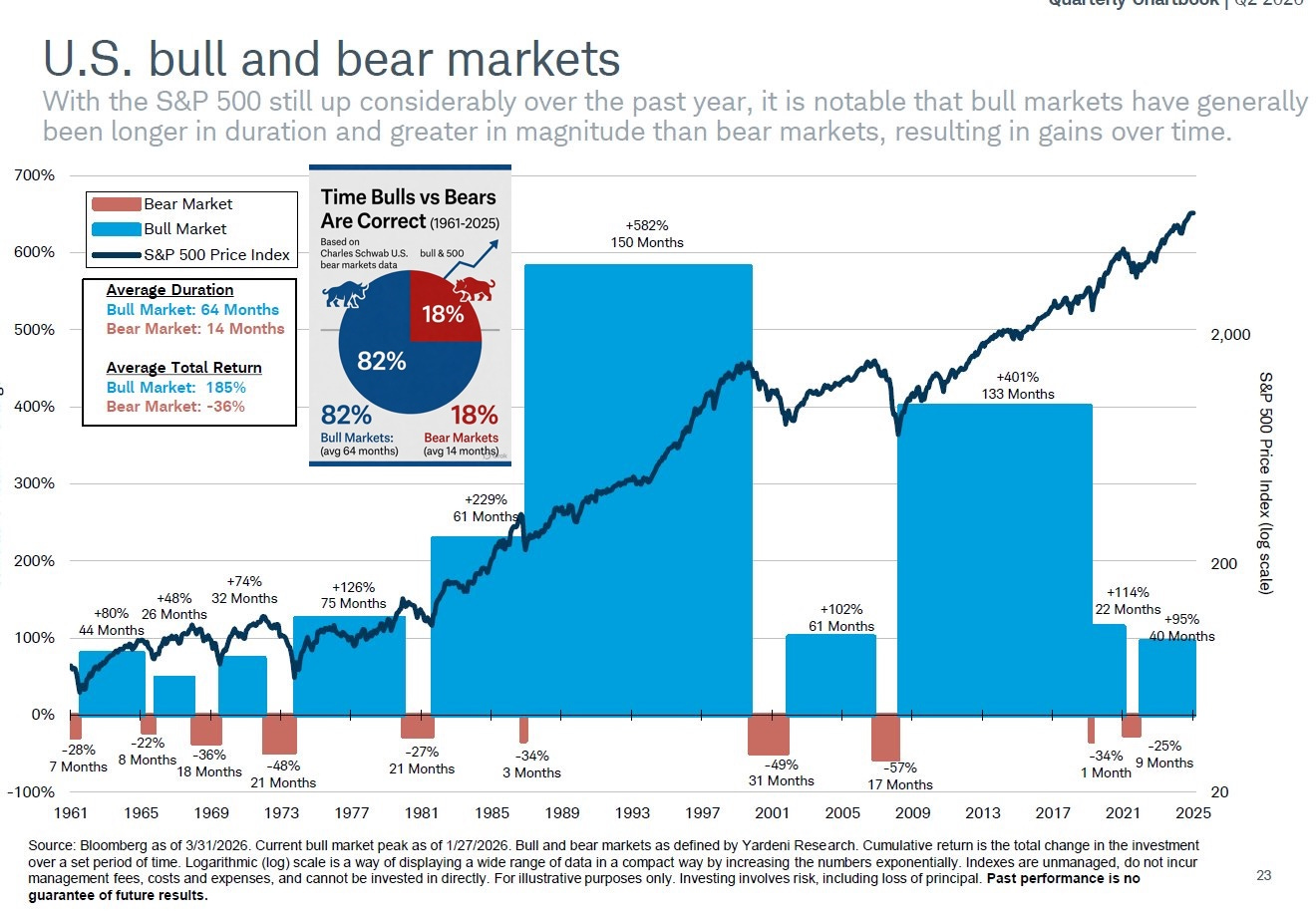

This happens for an extremely simple reason that is, however, often overlooked: stock markets spend most of their time near all-time highs. It is not an anomaly; it is their natural state. If an index grows on average over time, then it is inevitable it will continue to hit new highs with great frequency. And indeed, looking at the history of S&P500, it is clear a huge percentage of trading sessions fall within a few percentage points of previous all-time highs. This means that constantly waiting for «the right moment» very often amounts to building a strategy based on a lack of exposure. And absence of exposure, in the long run, is one of the most insidious forms of wealth destruction, because it doesn’t produce obvious losses but something even more dangerous: opportunity cost.

Un breve excursus sulla storia dei mercati

Questa dinamica si ripete ciclicamente da oltre un secolo. Nel 1995 moltissimi investitori erano convinti che Wall Street fosse ormai sopravvalutata. Nel 1996 Alan Greenspan parlò apertamente di «irrational exuberance», lasciando intendere che i mercati avessero raggiunto livelli eccessivi rispetto ai fondamentali. Nel 1998, dopo anni di rialzi praticamente ininterrotti, il consenso iniziava già a descrivere il mercato americano come una gigantesca bolla pronta a esplodere. Eppure, da quel momento fino al picco del 2000, il Nasdaq avrebbe ancora moltiplicato il proprio valore in maniera impressionante.

Lo stesso identico schema si è ripetuto nel periodo successivo alla crisi del 2008. Nel 2013 moltissimi investitori consideravano l’S&P500 troppo caro perché era già raddoppiato dai minimi della crisi finanziaria. Nel 2015 si parlava continuamente di fine ciclo. Nel 2017 il mercato sembrava salire senza volatilità e questo veniva interpretato come un chiaro segnale di imminente collasso. Nel 2021 il tema dominante era l’eccesso speculativo post-pandemia. Nel 2024 e nel 2025 il dibattito si è spostato sulla concentrazione delle mega cap tecnologiche e sul rischio che l’intero mercato americano fosse diventato dipendente da poche aziende legate all’intelligenza artificiale. Ma il punto centrale rimane sempre lo stesso: nella maggior parte dei casi il mercato continua a salire molto più a lungo di quanto gli investitori ritengano possibile.

Questo accade per una ragione estremamente semplice che però viene spesso ignorata: i mercati azionari passano gran parte della loro vita vicino ai massimi storici. Non è un’anomalia, è la loro condizione naturale. Se un indice cresce mediamente nel tempo, allora è inevitabile che continui a registrare nuovi massimi con una frequenza molto elevata. E infatti, osservando la storia dell’S&P500, emerge chiaramente come una percentuale enorme delle sedute si collochi entro pochi punti percentuali dai massimi assoluti precedenti. Questo significa che attendere continuamente «il momento giusto», equivale molto spesso a costruire una strategia basata sull’assenza di esposizione. E l’assenza di esposizione, nel lungo periodo, è una delle forme più subdole di distruzione patrimoniale, perché non produce perdite evidenti ma produce qualcosa di ancora più pericoloso: il costo opportunità.

Waiting doesn’t pay off

Opportunity cost is probably the concept least understood by retail investors. Those who remain in cash for years while market rises tend to focus exclusively on the risk they’ve avoided, without realizing the return they’ve sacrificed. Psychologically, it’s much easier to accept a missed gain than an actual loss, because human brain processes losses much more intensely than unrealized potential gains. But from a financial standpoint, difference is irrelevant: missing out on a 100% gain has just as massive an impact on your net worth as suffering a significant loss. Yet, while losses are felt immediately, the cost of staying out of the market manifests slowly, almost invisibly, over the years.

The most interesting paradox is that investors who fear buying at the top the most often end up entering at exactly the worst possible moment. Why? Because human beings constantly seek emotional confirmation. When market rises for years, those who stayed out feel uneasy but still maintain a certain caution. However, when rally continues long enough to become a collective consensus, perception of risk changes completely. At that point, market is no longer perceived as dangerous but as inevitable. And that’s exactly when many investors enter heavily, often after years of waiting. The problem is that major cycle highs occur when fear disappears almost completely and is replaced by the conviction that «this time is different».

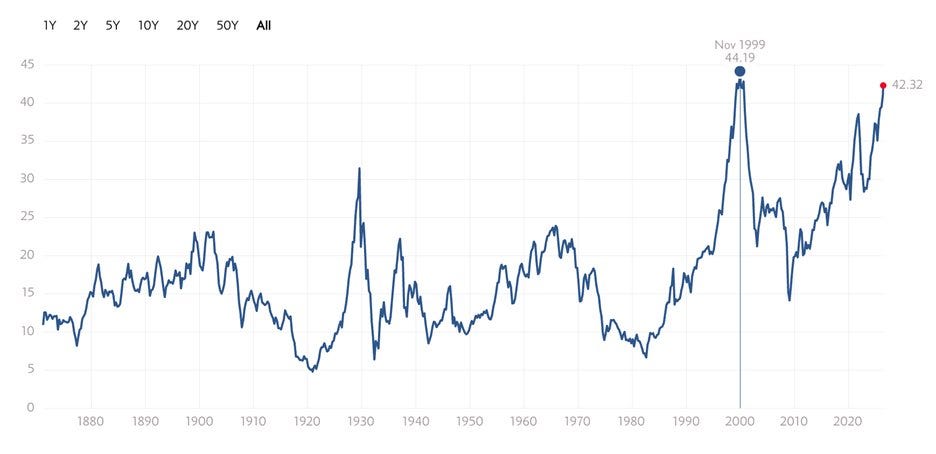

And this is where the most difficult concept to accept comes into play: market can simultaneously be too expensive to generate extraordinary returns over the next decade and yet continue to rise far more than expected in the short and mid-term. This is a fundamental distinction that many investors fail to grasp. An overvalued market doesn’t necessarily imply an imminent crash. High valuations reduce expected future returns, but they almost never provide reliable guidance on timing. And this is exactly why strategies based on the idea that «it’s too late to buy now» tend to fail historically.

Aspettare non paga

Il costo opportunità è probabilmente la variabile meno compresa dagli investitori retail. Chi rimane liquido per anni mentre il mercato sale, tende a concentrarsi esclusivamente sul rischio evitato, senza rendersi conto del rendimento sacrificato. Psicologicamente è molto più facile accettare un mancato guadagno rispetto a una perdita reale, perché il cervello umano contabilizza le perdite in maniera molto più intensa rispetto ai benefici potenziali non realizzati. Ma dal punto di vista finanziario la differenza è irrilevante: perdere un rialzo del 100% ha un impatto patrimoniale enorme quanto subire una perdita significativa. Eppure, mentre le perdite vengono percepite immediatamente, il costo di essere rimasti fuori dal mercato si manifesta lentamente, quasi invisibilmente, nel corso degli anni.

Il paradosso più interessante è che spesso gli investitori che temono maggiormente di comprare sui massimi finiscono poi per entrare esattamente nel momento peggiore possibile. Perché? Perché l’essere umano cerca continuamente conferme emotive. Quando il mercato sale per anni, chi è rimasto fuori prova disagio ma mantiene ancora una certa prudenza. Quando però il rialzo continua abbastanza a lungo da trasformarsi in consenso collettivo, allora cambia completamente la percezione del rischio. A quel punto il mercato non viene più percepito come pericoloso ma come inevitabile. Ed è esattamente lì che molti investitori entrano pesantemente, spesso dopo anni di attesa. Il problema è che i grandi massimi di ciclo nascono proprio quando la paura scompare quasi completamente e viene sostituita dalla convinzione che «questa volta sia diverso».

Ed è qui che entra in gioco il concetto più difficile da accettare: il mercato può essere contemporaneamente troppo caro per produrre rendimenti straordinari nel decennio successivo e comunque continuare a salire ancora molto più del previsto nel breve e medio periodo. Questa è una distinzione fondamentale che moltissimi investitori non riescono a comprendere. Un mercato sopravvalutato non implica necessariamente un imminente crollo. Le valutazioni elevate riducono i rendimenti attesi futuri, ma non forniscono quasi mai indicazioni affidabili sul timing. Ed è esattamente questo il motivo per cui strategie basate esclusivamente sull’idea che «ormai sia troppo tardi per comprare» tendono storicamente a fallire.

It’s never too late to…

Financial history is full of examples of those who have systematically tried to predict the end of bull markets. In the article, I cited some of the most emblematic cases, but the beginning and end of the «cycle of losers» is very long. In addition to retail investors, many asset managers remain underweight in equities for years because they believe valuations are unsustainable and, from a theoretical standpoint, they wouldn’t even be entirely wrong. The problem is that market can remain irrational for much longer than one can remain solvent or competitive. And this is the great contradiction of financial markets: being right too early very often amounts to being wrong.

Of course, none of this means the market always goes up or there aren’t extremely long and frustrating periods. Because while it’s true staying out of the market for too long has historically been a losing strategy, it’s equally true entering emotionally and aggressively right near major structural highs can condemn an investor to years, sometimes decades, of zero real returns. Just look at the Japanese market after 1989 or Nasdaq after 2000: those who bought at the height of the dot-com bubble euphoria would have taken over a decade just to break even in nominal terms, not to mention the number of companies that went bankrupt trying to ride the wave and the golden years of internet.

The conclusion seems obvious: there is no point at which the market becomes easy to read, but only phases in which the narrative seems convincing. Any attempt to reduce the market to a «right time» to enter tends to oversimplify a dynamic remains structurally continuous yet simultaneously random and unpredictable. Rather than identifying the perfect entry point, the real issue is accepting that market rarely offers conditions of clarity between price and perception. By accepting this logic, we will stop living in a market where tomorrow is always too late to buy and too early to short.

Non è mai troppo tardi per…

La storia finanziaria è piena di esempi devastanti per chi ha provato sistematicamente ad anticipare la fine dei rialzi. Nell’articolo, ho citato alcuni dei casi più emblematici, ma l’inizio e la fine del «ciclo dei perdenti» è lunghissimo. Oltre agli investitori al dettaglio, moltissimi gestori professionali rimangono sotto-pesati sull’azionario per anni perché ritengono che le valutazioni siano insostenibili e, dal punto di vista teorico, non avrebbero nemmeno completamente torto. Il problema è che il mercato può rimanere irrazionale molto più a lungo di quanto si riesca a rimanere solvibili o competitivi. Ed è questa la grande contraddizione dei mercati finanziari: avere ragione troppo presto equivale molto spesso ad avere torto.

Naturalmente tutto questo non significa che il mercato salga sempre o che non esistano periodi estremamente lunghi e frustranti. Perché se è vero che rimanere fuori dal mercato troppo a lungo rappresenta storicamente una strategia perdente, è altrettanto vero che entrare in maniera emotiva e aggressiva proprio in prossimità di grandi massimi strutturali può condannare un investitore a vivere anni, talvolta decenni, di rendimenti reali praticamente nulli. Basta osservare il mercato giapponese dopo il 1989 oppure il Nasdaq dopo il 2000: chi acquistò nel pieno dell’euforia della bolla dot-com avrebbe impiegato oltre un decennio semplicemente per tornare in pari nominalmente, oltre alla quantità di aziende fallite che provarono a calvare l’onda e gli anni d’oro dell’internet.

La conclusione pare ovvia e scontata: non esiste un punto in cui il mercato diventa facile da leggere, ma solo fasi in cui la narrazione sembra convincente. Ogni tentativo di ridurre il mercato a un momento giusto per entrare, tende a semplificare eccessivamente una dinamica che resta strutturalmente continua ma allo stesso tempo randomica e imprevedibile. Più che individuare il punto di ingresso perfetto, la questione reale è accettare che il mercato raramente offre condizioni di chiarezza tra prezzo e percezione. Accettando questa logica, smetteremo di vivere in un mercato in cui il domani è sempre troppo tardi per comprare e troppo presto per vendere.