The Upside Down

While DAX (including dividends) as a stock market barometer for large German-originated global companies reached a new all-time high today, the Aktien of mid-size and small companies is still below

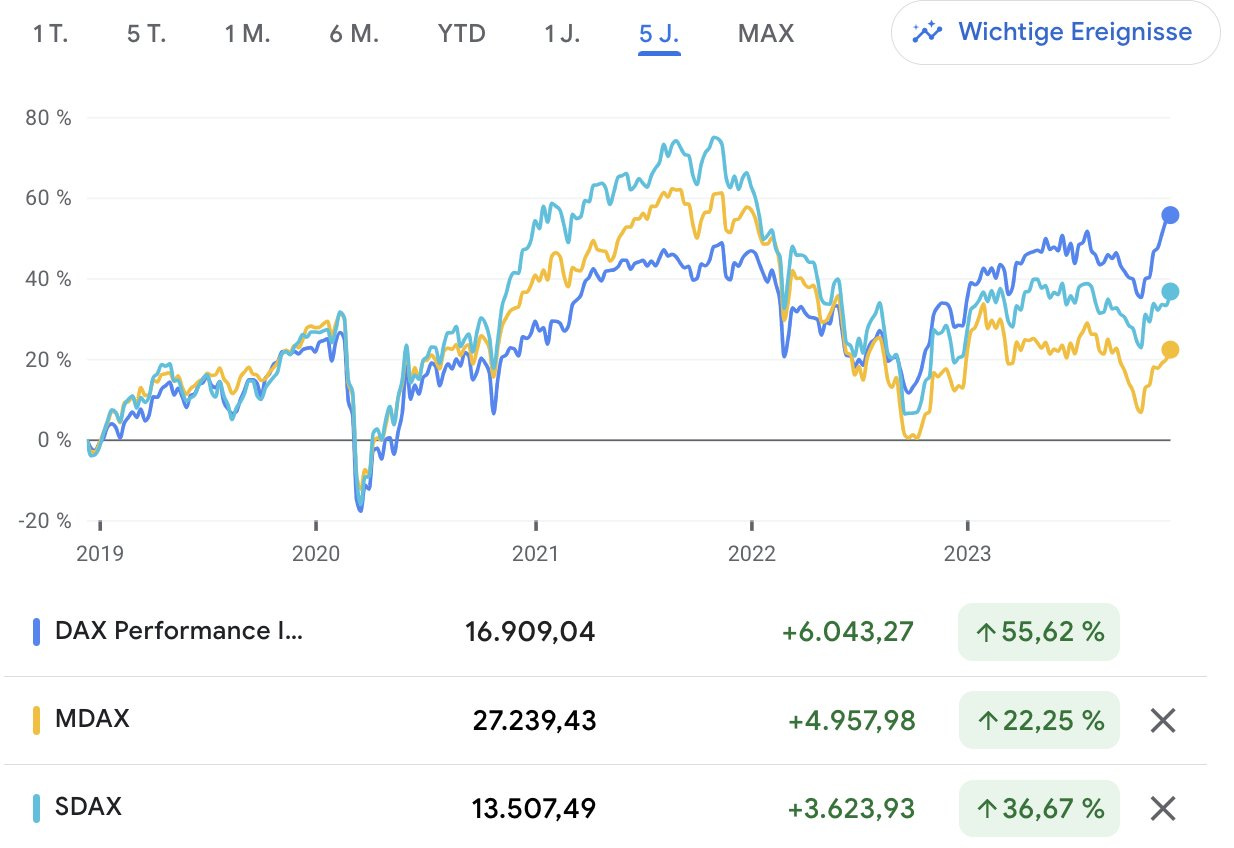

German industrial production fell 0.4% in the fourth quarter, marking the fifth consecutive monthly decline. Meanwhile, the DAX Index representing Germany's top 40 companies reached 17,000 points, breaking all previous records, updating all-time highs day after day. After the drop in exports and sharp decline in new orders, it is now the turn of industrial production to disappoint, signaling a very weak start to the fourth quarter. On a year-over-year basis, industrial production is down 3.5%. Suffice it to say that at current levels, we are about 7% below the pre-pandemic level, almost 4 years later.

For the avoidance of doubt: fact that DAX has risen above 17,000 for the first time has nothing to do with the ability of the coalition government to reach agreement on the budget. Nor is the stock market celebrating Germany as an economic center, but rather the prospects of the 40 companies included in the index, which generate only one-fifth of their sales in Germany and have about two-thirds of their workforce abroad.

Nel quarto trimestre la produzione industriale tedesca è scesa dello 0,4%, registrando il quinto calo mensile consecutivo. Nel frattempo l’Indice DAX rappresentativo delle 40 migliori aziende di Germania, ha raggiunto i 17,000 punti, rompendo tutti i record precedenti, aggiornando massimi storici giorno dopo giorno. Dopo il calo delle esportazioni e la forte diminuzione dei nuovi ordini, è ora la volta della produzione industriale a deludere, segnalando un inizio molto debole del quarto trimestre. Su base annua, la produzione industriale è scesa del 3,5%. Basti ricordare che ai livelli attuali, siamo circa il 7% al di sotto del livello pre-pandemia, quasi 4 anni dopo.

A scanso di equivoci: il fatto che il DAX sia salito per la prima volta sopra quota 17.000 non ha nulla a che vedere con la capacità del governo di coalizione di trovare un accordo sul bilancio. La Borsa non sta nemmeno celebrando la Germania come piazza economica, ma piuttosto le prospettive delle 40 aziende incluse nell'indice, che generano solo un quinto del loro fatturato in Germania e hanno circa due terzi della loro forza lavoro all'estero.

Return of austerity

Also weighing on the recession risk was the fiscal issue: monetary tightening put in place by the European Central Bank and new austerity measures announced recently will play a key role in the coming months. December is the month of sealing of fiscal maneuvers in the major eurozone countries: time is running out and a solution to a 17 billion hole had to be found. The agreement includes spending cuts, tax increases and other pains for citizens. This will probably keep the economy in a mild recession next year. The new budget follows the Constitutional Court ruling a month ago that the reallocation of 60 billion euros of unused pandemic-era debt to the Climate and Transformation Fund was not in line with the Constitution. As a result, the government was forced to suspend ex-post, the constitutional debt brake for 2023 budget and resolve a funding gap of about 17 billion euros for the 2024 budget.

In short, government plans to reduce climate-damaging subsidies, discontinue subsidies for electric vehicles and solar panel industry earlier than planned, reduce some spending by individual ministries, and try to make social spending «more efficient». There will also be an increase in the price of CO2 emissions and introduction of a new tax on plastic packaging. The government wants to avoid the fifth consecutive year of official deviation from the constitutional debt brake, but still wants to test the possibility of a nearly 3 billion euro deviation to continue funding the 2021 flood damage. Finally, Climate and Transition Fund will be reduced by a total of 45 billion euros for the period 2024-2027.

Overall, the measures announced seem to be manageable for the economy. However, the ongoing dispute over how to combine large-scale investment and balanced budgets will not end quickly. Austerity measures would clearly push the economy into further recession, not to mention that they would lead to unprecedented fiscal policy across the Eurozone: austerity in a low-debt country and rather loose fiscal policies in high-debt countries. In any case, recent fiscal problems have clearly damaged credibility and reliability of policy announcements and, at least in the short term, will lead to a greater slowdown in investment and consumption. It is likely, therefore, to expect the current state of stagnation and recession to continue. The risk that 2024 will prolong situation is high, and it would not be the first time that Germany has entered negative territory, as happened some 20 years ago in the early 2000s.

Il ritorno dell'austerità

Ad aumentare il rischio recessione ha pesato anche la problematica fiscale: la stretta monetaria messa in piedi dalla Banca Centrale Europea e le nuove misure di austerità annunciate recentemente giocheranno un ruolo fondamentale nei prossimi mesi. Dicembre è il mese della sigla delle manovre finanziarie nei principali paesi dell’Eurozona: il tempo sta per scadere ed è stato necessario trovare una soluzione ad un buco di 17 miliardi. L’accordo prevede tagli alla spesa, aumenti per le tasse e altri dolori per i cittadini. Questo probabilmente manterrà l'economia in una lieve recessione l'anno prossimo. Il nuovo bilancio fa seguito alla sentenza della Corte Costituzionale di un mese fa, secondo la quale la riallocazione di 60 miliardi di euro di debito inutilizzato dell'era pandemica al fondo per il clima e la trasformazione non era in linea con la Costituzione. Di conseguenza, il governo è stato costretto a sospendere ex-post, il freno costituzionale al debito per il bilancio 2023 e a risolvere un deficit di finanziamento di circa 17 miliardi di euro per il bilancio 2024.

In breve, il governo prevede di ridurre i sussidi che danneggiano il clima, di interrompere prima del previsto i sussidi per i veicoli elettrici e l'industria dei pannelli solari, di ridurre alcune spese dei singoli ministeri e di cercare di rendere «più efficiente» la spesa sociale. Ci sarà anche un aumento del prezzo delle emissioni di CO2 e l'introduzione di una nuova tassa sugli imballaggi di plastica. Il governo vuole evitare il quinto anno consecutivo di deviazione ufficiale dal freno al debito costituzionale, ma vuole comunque verificare la possibilità di una deviazione di quasi 3 miliardi di euro per continuare a finanziare i danni delle alluvioni del 2021. Infine, il Fondo per il clima e la transizione sarà ridotto di un totale di 45 miliardi di euro per il periodo 2024-2027.

Nel complesso, le misure annunciate sembrano essere gestibili per l'economia. Tuttavia, la controversia in corso su come combinare investimenti su larga scala e bilanci in equilibrio non si esaurirà velocemente. Le misure di austerità spingerebbero chiaramente l'economia verso un'ulteriore recessione, senza contare che porterebbero a una politica fiscale senza precedenti in tutta l'Eurozona: austerità in un Paese a basso debito e politiche fiscali piuttosto allentate nei Paesi ad alto debito. In ogni caso, i recenti problemi fiscali hanno chiaramente danneggiato la credibilità e l'affidabilità degli annunci politici e, almeno nel breve termine, porteranno a un maggiore rallentamento degli investimenti e dei consumi. E probabile quindi aspettarsi che l’attuale stato di stagnazione e recessione continui. Il rischio che nel 2024 la situazione si prolunghi è alto e non sarebbe la prima volta che la Germania entra in territorio negativo, come capitò circa 20 anni fa nei primi anni 2000.

The Chinese Reversal

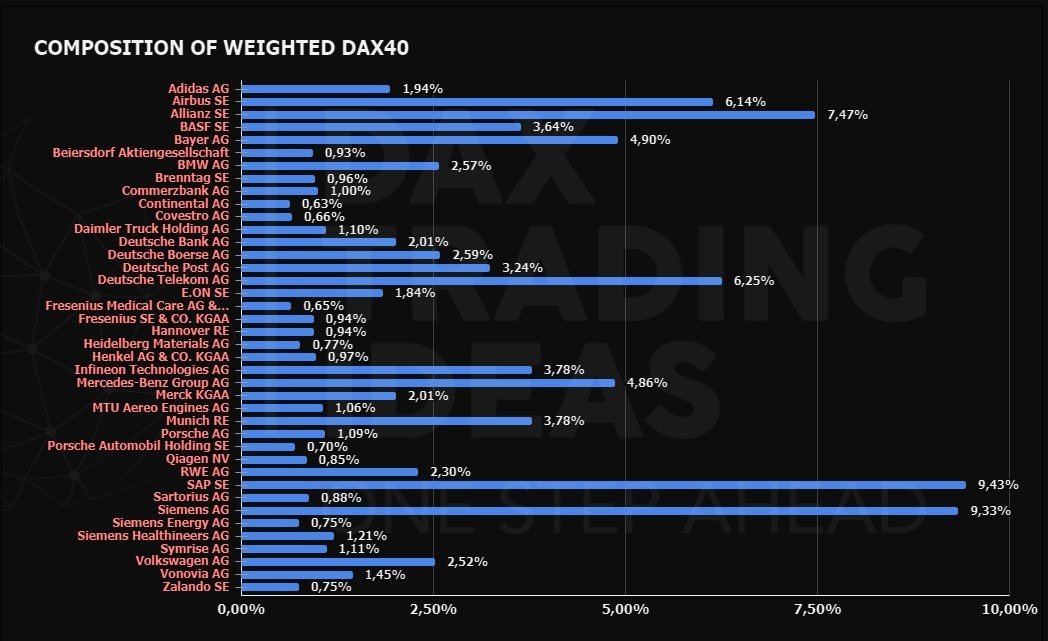

Then, what is the reason for this very powerful boost of German listed companies? We may find the answer in the numbers, and in tech. The composition of DAX index in fact follows very closely that of US tech, the Nasdaq for short. Although at first glance it might seem easy to place Germany toward the classic old-fashioned industry, today the situation has changed. The weight is distributed equally in the tech sector between services and software. A very curious thing that hints at how much this market is getting carried away by expectations narrative, just take a look at what is happening in China. The underperformance of emerging equities is justified by structural problems Asian giant is struggling with. Moreover, German equities have always maintained a high correlation, motivated by direct agreements and robust ties between the two economies. Recently this correlation has softened to an inverse correlation. The world upside down.

Even assuming that the importance of Chinese demand for German companies has recently diminished, a stably negative correlation between the 2 countries' stock markets seems an unlikely development. On this basis, a temporary convergence seems a desirable outcome in the coming weeks: German stock down and Chinese recovery by Q1 2024.

L'inversione Cinese

A cosa è dovuto allora questo boost potentissimo delle aziende tedesche quotate a mercato? La risposta potremo trovarla nei numeri, e nella tecnologia. La composizione dell’indice DAX infatti segue molto da vicino quello delle tech USA, il Nasdaq per intenderci. Sebbene ad un primo approccio potrebbe sembrar facile collocare la Germania verso la classica industria vecchio stampo, oggi la situazione è cambiata. Il peso è distribuito equamente nel comparto tecnologico tra servizi e software. Una cosa molto curiosa che fa intendere quanto questo mercato si stia facendo portare via dalla narrativa delle aspettative, basta dare un occhiata a quello che sta succedendo in Cina. La sotto-performance dell’azionario emergente è giustificata dai problemi strutturali in cui si dibatte il colosso asiatico. Inoltre l’azionario tedesco ha sempre conservato una correlazione elevata, motivata da accordi diretti e robusti legami tra le due economie. Recentemente questa correlazione si è attenuata fino a diventare inversa. Il mondo alla rovescia.

Pur ammettendo che l’importanza della domanda cinese per le aziende tedesche si sia recentemente ridotta, una correlazione stabilmente negativa tra le borse dei 2 paesi sembra uno sviluppo improbabile. Su queste basi, una temporanea convergenza sembra un esito auspicabile nelle prossime settimane: azionario tedesco giù e ripresa cinese entro il Q1 2024.