The Swiss Currency Shock Explained

Depeg risk in Forex: the incredible day when Swiss franc shocked the markets

In late 2014 and early 2015 I was taking my first steps in the study of financial markets, macroeconomics and everything revolving around global finance. As is often the case when you approaches a new field, whether for work or passion, the first thing encounters is the allure of «sirens» or those seductive narratives that promise certainty, shortcuts, and absolute truths. In my case, those sirens with their seductive and bewitching song spoke of Forex, binary options and seemingly unbreakable systems. From there I understood how paved the road was within this world, but at the same time I was totally unaware that experiencing one of the most incredible moments in currency history and all of finance.

Indeed, January 15, 2015, was the day when the Swiss National Bank (SNB) surprisingly announced the abandonment of the low exchange rate between the euro and Swiss franc, which until then had been fixed at 1.20. This seemingly technical decision set off a chain reaction in global markets: within minutes, billions were lost, several brokers went into default, and confidence in one of the pillars of European currency stability was shaken from the ground up. This article traces in detail the roots of the SNB's decision, its immediate impact, parallels with other historical currency crises (including those related to cryptocurrencies, ed.), and finally offers some thoughts on the risks that could reoccur in similar forms today. Let's dig in.

Tra la fine del 2014 e l’inizio del 2015 muovevo i primi passi nello studio dei mercati finanziari, della macroeconomia e di tutto ciò che ruota attorno alla finanza globale. Come spesso accade quando ci si avvicina a un campo nuovo, che sia per lavoro o per passione, la prima cosa che si incontra è il fascino delle «sirene», ovvero quelle narrazioni seducenti che promettono certezze, scorciatoie e verità assolute. Nel mio caso, quelle sirene dal canto seducente e ammaliatore parlavano di Forex, opzioni binarie e sistemi apparentemente infrangibili. Da lì capì quanto fosse lastricata la strada all’interno di questo mondo, ma allo stesso tempo ero totalmente inconsapevole di star vivendo uno dei momenti più incredibili della storia valutaria e della finanza tutta.

Il 15 Gennaio 2015 infatti, fu il giorno in cui la Banca Nazionale Svizzera (BNS) annunciò a sorpresa l'abbandono del tasso minimo di cambio tra euro e franco svizzero, fino ad allora fissato a 1,20. Questa decisione, apparentemente tecnica, scatenò una reazione a catena sui mercati globali: in pochi minuti, si persero miliardi, diversi broker andarono in default e la fiducia in uno dei pilastri della stabilità valutaria europea venne scossa dalle fondamenta. Questo articolo ripercorre in dettaglio le radici della decisione della BNS, il suo impatto immediato, i paralleli con altre crisi valutarie storiche (comprese quelle legate alle cripto-valute, ndr), e infine propone alcune riflessioni sui rischi che oggi potrebbero ripresentarsi in forme simili. Approfondiamo.

The context and time X

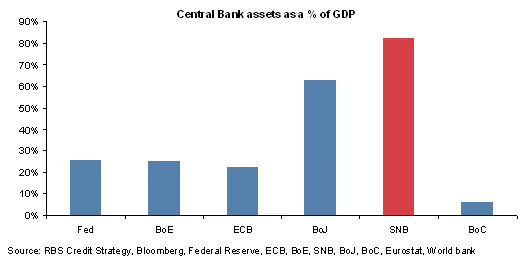

In 2011, Europe was in the midst of a sovereign debt crisis. Capital was seeking refuge in safe assets, and Swiss franc, which had always been considered a safe haven asset, began to strengthen significantly. This phenomenon was undermining the competitiveness of the Swiss economy, which was heavily based on exports. Swiss companies were seeing declining profits, tourism was slowing down, and deflationary risk was becoming increasingly real. To protect its economic system, SNB introduced a low exchange rate on September 6, 2011: it would prevent the euro from falling below 1.20 against the franc. The message was clear: SNB was ready to intervene in the market buying foreign currency in unlimited quantities if necessary. Over the next three years, Switzerland accumulated huge foreign exchange reserves to maintain that level, while meanwhile the European Central Bank moved toward increasingly expansionary monetary policies.

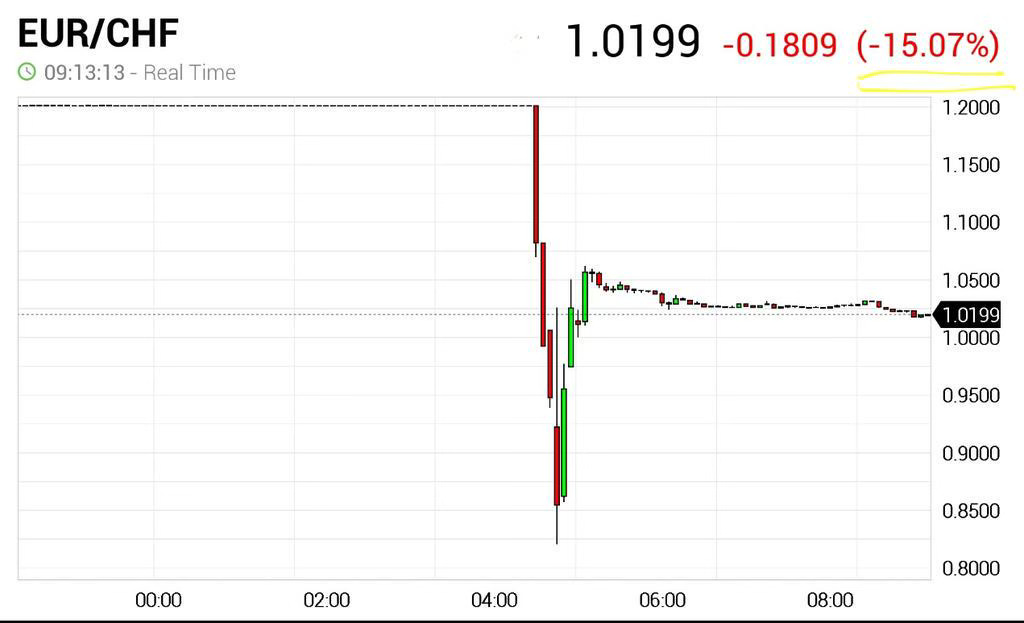

At 10:30 a.m. on January 15, 2015, SNB announced the end of the low rate, in a dry statement and without any warning. The decision was justified by intensifying divergence between monetary policies of the Eurozone and Switzerland: in particular, SNB no longer considered it sustainable to continue defending the peg in a context in which the ECB was preparing to launch its quantitative easing program, which would further weaken the euro. The reaction was fast: within minutes, the franc appreciated by up to 30%, rising from 1.20 to 0.85 against the euro. Liquidity in the currency market evaporated, some orders were executed at out-of-control prices, others were not executed at all. Swiss and European stock exchanges collapsed as investors tried to understand magnitude of the change. Confidence in the Swiss monetary system faltered, but even more so did confidence in the central banks' defensive tools.

The repercussions were enormous. FXCM, a leading retail forex broker, reported losses of $225 million and was forced to obtain an emergency bailout from Leucadia. Other brokers, such as Alpari UK, declared bankruptcy within hours. The Swiss stock exchange lost more than 10% on the same day, and large companies such as Swatch, UBS and Credit Suisse were among the hardest hit. On the real economy, the effects were felt immediately: export sector had to drastically revise turnover forecasts, while tourism saw its competitiveness shrink. The Swiss media spoke of a currency earthquake that would forever change the relationship between Switzerland and Europe.

The case of the Swiss franc was not unique in financial history. Similar crises have occurred in the past. In 1997, Thailand was forced to abandon the baht's fixed exchange rate with the dollar due to massive speculation and depleted reserves, triggering Asian financial crisis. In 1998, it was Russia's turn, where the ruble collapsed after peg defense drained national reserves. In both cases, the currency anchor system proved fragile in the face of market pressure. More recently, in 2022, the cryptocurrency world also experienced its own «dramatic depeg». The Terra case, an algorithmic stablecoin theoretically pegged to the dollar, is emblematic. When stabilization mechanism collapsed, Terra lost parity and its value virtually went to zero within days, generating a wave of distrust throughout stablecoin industry. Common thread linking all of these cases is the loss of credibility of the promise of stability: when markets perceive that a peg is no longer defensible or economically viable, detachment becomes inevitable.

Il contesto e l’ora X

Nel 2011, l’Europa era nel pieno della crisi del debito sovrano. I capitali cercavano rifugio in asset sicuri e il franco svizzero, considerato da sempre un bene rifugio, iniziò a rafforzarsi in modo significativo. Questo fenomeno stava minando la competitività dell'economia svizzera, fortemente basata sull’export. Le aziende elvetiche vedevano calare i profitti, il turismo rallentava e il rischio deflattivo diventava sempre più concreto. Per proteggere il proprio sistema economico, la BNS introdusse il 6 Settembre 2011 un tasso minimo di cambio: avrebbe impedito che l’euro scendesse sotto 1,20 rispetto al franco. Il messaggio era chiaro: la Banca Nazionale era pronta a intervenire sul mercato acquistando valuta estera in quantità illimitata, se necessario. Nei tre anni successivi, la Svizzera accumulò enormi riserve valutarie per mantenere quel livello, mentre nel frattempo la Banca Centrale Europea si muoveva verso politiche monetarie sempre più espansive.

Alle 10:30 del mattino del 15 Gennaio del 2015 la BNS annunciò la fine del tasso minimo, con un comunicato secco e senza alcun preavviso. La decisione fu giustificata con l’intensificarsi delle divergenze tra le politiche monetarie dell’Eurozona e della Svizzera: in particolare, la BNS non riteneva più sostenibile continuare a difendere il peg in un contesto in cui la BCE si preparava a lanciare il suo programma di quantitative easing, che avrebbe indebolito ulteriormente l’euro. La reazione fu istantanea: in pochi minuti, il franco si apprezzò fino al 30%, passando da 1,20 a 0,85 contro l’euro. La liquidità sul mercato valutario evaporò, alcuni ordini furono eseguiti a prezzi fuori controllo, altri non vennero eseguiti affatto. Le borse svizzere e europee crollarono, mentre gli investitori cercavano di comprendere le dimensioni del cambiamento. La fiducia nel sistema monetario elvetico vacillava, ma ancor più tremava quella negli strumenti di difesa delle banche centrali.

Le ripercussioni furono enormi. FXCM, uno dei principali broker forex retail, riportò perdite per 225 milioni di dollari e fu costretto a ottenere un salvataggio d’urgenza da Leucadia. Altri broker, come Alpari UK, dichiararono fallimento nel giro di poche ore. La Borsa svizzera perse oltre il 10% nella stessa giornata, e grandi aziende come Swatch, UBS e Credit Suisse furono tra le più colpite. Sull’economia reale, gli effetti si fecero sentire da subito: il settore dell’export dovette rivedere drasticamente le previsioni di fatturato, mentre il turismo vide ridursi la competitività. I media svizzeri parlarono di un terremoto valutario che avrebbe cambiato per sempre il rapporto tra la Svizzera e l’Europa.

Il caso del franco svizzero non fu un unicum nella storia finanziaria. Crisi simili si sono verificate in passato. Nel 1997, la Thailandia fu costretta ad abbandonare il cambio fisso del baht con il dollaro a causa di speculazioni massive e riserve esaurite, innescando la crisi finanziaria asiatica. Nel 1998 fu la volta della Russia, dove il rublo crollò dopo che la difesa del peg prosciugò le riserve nazionali. In entrambi i casi, il sistema di ancoraggio valutario si rivelò fragile davanti alla pressione dei mercati. Più recentemente, nel 2022, anche il mondo delle cripto-valute ha vissuto il proprio «depeg drammatico». Il caso di Terra, una stablecoin algoritmica teoricamente ancorata al dollaro, è emblematico. Quando il meccanismo di stabilizzazione è collassato, Terra ha perso la parità e il suo valore si è praticamente azzerato nel giro di giorni, generando un'ondata di sfiducia in tutto il comparto delle stablecoin. Il filo conduttore che unisce tutti questi casi è la perdita di credibilità della promessa di stabilità: quando i mercati percepiscono che un peg non è più difendibile o economicamente sostenibile, il distacco diventa inevitabile.

The lesson for investors (and me): it can happen again!

The depeg of Swiss franc highlighted even assets considered most stable can be subject to violent swings. Those who were leveraged positions based on the assumption that franc could never cross certain limits suffered catastrophic losses. This is what financial markets do: when something works for too long and short-term investors exploit an advantage, they try to shake fleas off. And so they did. So many retail clients have ended up with negative accounts, and mind you, it is often written in the clauses of Forex brokers that «losses in excess of the balance must be covered». That's why there are margin calls, that's why there are regulators (like Esma, ed.) that's why in Europe we can consider ourselves lucky, no matter how much we may say or speak ill of it. The main lesson is that no currency regime is eternal, and even central bank interventions, however credible, have political, economic and technical limits. Those who operate in the markets must take these dynamics into account. Relying on a peg as if it were an absolute guarantee can be dangerous: balancing risk and return requires careful management, in-depth knowledge of current monetary policies, and, above all, the humility to consider even the most unlikely scenarios.

Currency crises, by their nature, recur in contexts where promises of stability collide with changing realities, and there are several potentially explosive scenarios today. Some pegged currencies, such as the Saudi rial to the dollar, could come under pressure if capital flows or U.S. policies change dramatically (as has been happening recently, ed.). Stablecoins, especially uncollateralized ones, are also constantly at risk of losing their peg in the absence of transparency or credible backing (basically trust is placed in the company, not the project or technology, ed.). Global monetary policies, after a decade of easing, are diverging again, creating tensions among the world's major currencies. Any imbalance, any loss of confidence, any sign of reserve depletion can trigger a domino effect. Along comes Trump, who historically aims for dollar devaluation, and suddenly all economic theories that wanted the euro below parity vanish in a matter of weeks. History teaches so much in this respect.

The depeg of Swiss franc was a warning to financial markets: even the imponderable can happen. Imagine waking up one day and Swiss franc has appreciated in value by 30%, destroying the net worth of your portfolio. The irony at time was that many people moved their mortgages into Swiss francs because of their security and stability after 2008 financial crisis and lower interest rates, which could be as low as 1.5%. When confidence is broken, the reactions can be immediate and devastating. Investors, institutions and regulators must always remember that currency stability is, after all, a convention: strong while credible, but fragile when put to the test. In the age of global crises, cryptocurrencies and central banks under pressure, that lesson remains as relevant as ever.

La lezione per gli investitori (e per me): può accadere di nuovo!

Il depeg del franco svizzero ha evidenziato che anche gli asset considerati più stabili possono essere soggetti a oscillazioni violente. Chi era posizionato a leva sulla base dell’ipotesi che il franco non potesse mai superare certi limiti ha subito perdite catastrofiche. Questo è quello che fanno i mercati finanziari: quando qualcosa funziona per troppo tempo e gli investitori di breve periodo sfruttano un vantaggio, cercano di scrollarsi le pulci di dosso. E così è stato. Tantissimi clienti al dettaglio si sono ritrovati con conti negativi e, badate bene, nelle clausole degli intermediari Forex è spesso scritto che «le perdite superiori al saldo devono essere ricoperte». Ecco perchè esistono i margini di garanzia, ecco perchè esistono gli enti regolatori (come Esma, ndr) ecco perchè in Europa possiamo considerarci fortunati, per quanto si possa dire o parlarne male. La lezione principale è che nessun regime valutario è eterno e anche gli interventi delle banche centrali, per quanto credibili, hanno limiti politici, economici e tecnici. Chi opera nei mercati deve tenere conto di queste dinamiche. Affidarsi a un peg come se fosse una garanzia assoluta può essere pericoloso: l’equilibrio tra rischio e rendimento richiede un’attenta gestione, una conoscenza profonda delle politiche monetarie in atto e, soprattutto, l’umiltà di considerare anche gli scenari più improbabili.

Le crisi valutarie, per loro natura, si ripresentano in contesti in cui le promesse di stabilità si scontrano con realtà mutevoli e oggi esistono diversi scenari potenzialmente esplosivi. Alcune valute ancorate, come il rial saudita al dollaro, potrebbero essere messe sotto pressione se i flussi di capitale o le politiche USA cambiassero in modo drastico (come sta accadendo recentemente, ndr). Anche le stablecoin, soprattutto quelle non collateralizzate, sono costantemente a rischio di perdere il peg in assenza di trasparenza o sostegno credibile (fondamentalmente la fiducia è riposta nell’azienda, non nel progetto o nella tecnologia, ndr). Le politiche monetarie globali, dopo un decennio di allentamento, stanno nuovamente divergendo, creando tensioni tra le principali valute mondiali. Ogni squilibrio, ogni perdita di fiducia, ogni segnale di esaurimento delle riserve può innescare un effetto domino. Arriva Trump che storicamente punta alla svalutazione del dollaro e improvvisamente tutte le teorie economiche che volevano l’Euro sotto la parità svaniscono in poche settimane. La storia insegna tanto sotto questo punto di vista.

Il depeg del franco svizzero è stato un monito per i mercati finanziari: anche l’imponderabile può accadere. Immaginate di svegliarvi un giorno e che il franco svizzero si sia rivalutato del 30%, distruggendo il patrimonio netto del vostro portafoglio. L'ironia dell’epoca fu che molte persone spostarono i loro mutui in franchi svizzeri grazie alla loro sicurezza e stabilità dopo la crisi finanziaria del 2008 e ai tassi di interesse più bassi, che potevano arrivare fino all'1,5%. Quando la fiducia viene meno, le reazioni possono essere immediate e devastanti. Investitori, istituzioni e regolatori devono sempre ricordare che la stabilità valutaria è, in fondo, una convenzione: forte finché credibile, ma fragile quando messa alla prova. Nell’epoca delle crisi globali, delle cripto-valute e delle banche centrali sotto pressione, quella lezione rimane attuale come non mai.

Remember that moment so well. Had just been invited by a PE group to bid in an auction for a block of stock in a HK listed financial. Pricing risk when you did not know how many hedge funds had been blown up by carry trades was a challenge!!