The Art of Investing

A simple strategy that can change your life

When it comes to investing, there is often a tendency to overcomplicate matters. Charts are analyzed, economic models are studied, market forecasts are sought. Yet the real mantra capable of building wealth over time is remarkably simple: regularly buy a diversified range of income-producing assets without worrying about market fluctuations. We're not talking about choosing the right time to invest or calculating perfect quantities: the secret is simply to keep buying, consistently, as a habit of life.

This philosophy, which at first glance may seem almost too elementary, is based on a fundamental principle: market tends to rise in the long run, despite physiological ups and downs. Those who stop too often to calculate run the risk of becoming immobilized by fear or greed, missing the most important opportunities. Many investors fall into the trap of market timing: they wait for the perfect time to enter or exit the market, in an effort to maximize gains and minimize losses. This is an understandable temptation: no one would want to invest just before a crash.

For example, at the beginning of 2017, with the major stock indexes near all-time highs, many wondered whether to wait for a correction. Those who hesitated, however, missed out on a further period of growth. This is a universal lesson: market can remain overvalued for much longer than we imagine. A simple online search for overvalued stocks in any historical era, from 1920s to the present, returns hundreds of articles full of warnings, which have often turned out to be premature or unfounded. Those who always wait for the right moment often end up never investing or getting in too late.

In the process, they lose the most powerful effect of all: time.

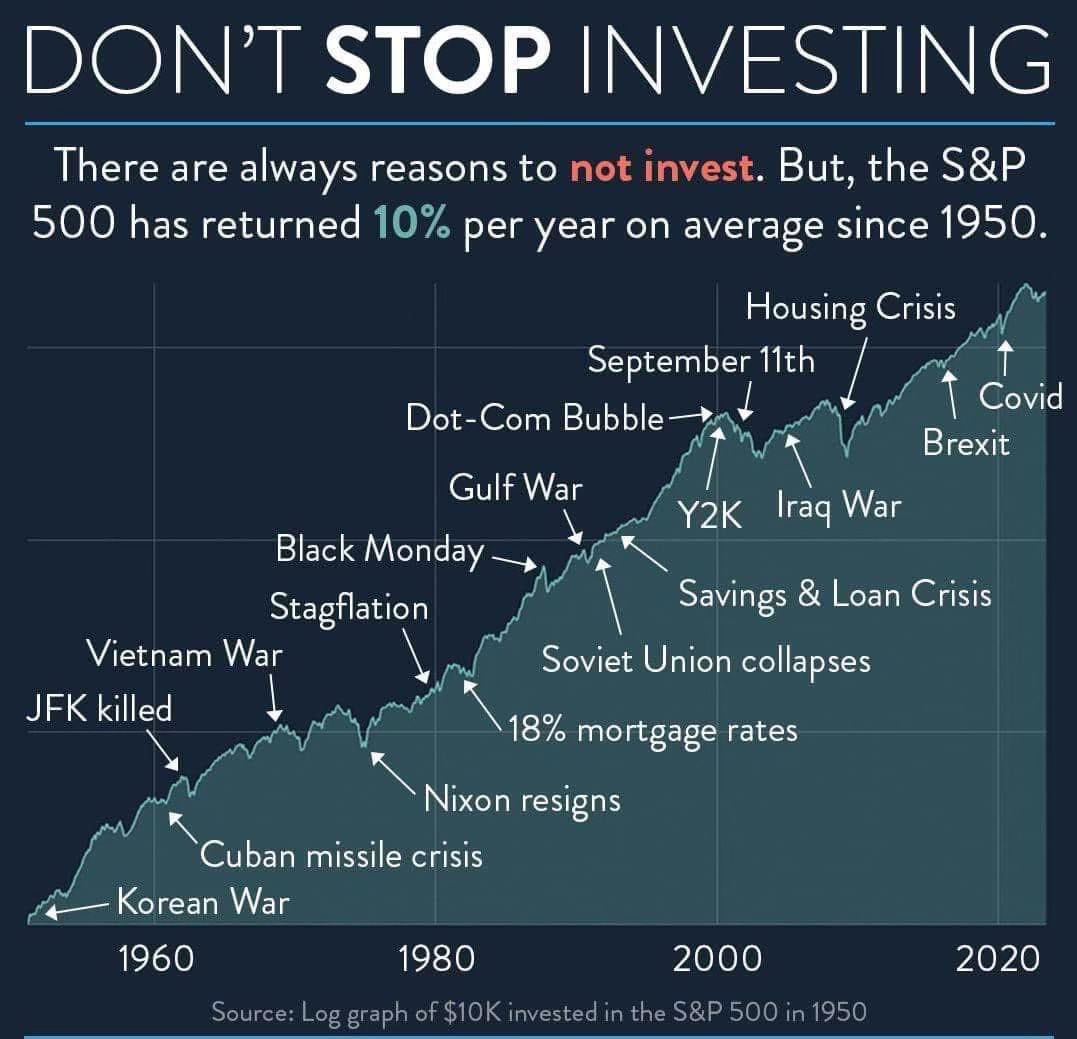

Truth is that market constantly offers good reasons to be pessimistic: economic crises, geopolitical tensions, recessions, disruptive technological innovations change rules of the game. But history shows that those who have continued to invest, ignoring the background noise, have been rewarded. Just as one pays rent every month or shops for groceries every week, investing should become an automatic habit, independent of the mood of the market. As long as transaction costs are low or zero, the best strategy is to buy regularly, without being paralyzed by emotions or news of the moment.

This technique is known as dollar cost averaging (DCA): investing fixed amounts at regular intervals, buying more shares when prices fall and fewer shares when prices rise. Over time, you reduce the risk of investing everything at a bad time and take advantage of volatility in your favor. Compared to traditional DCA, Just Keep Buying approach adds an even stronger psychological dimension: not just automating investments, but getting mentally used to the fact that market will go up and down, and this is part of the game.

Quando si parla di investimenti, si tende spesso a complicare eccessivamente il discorso. Si analizzano grafici, si studiano modelli economici, si cercano previsioni sui mercati. Eppure, il vero mantra capace di costruire ricchezza nel tempo è straordinariamente semplice: acquistare regolarmente una gamma diversificata di asset che producono reddito, senza preoccuparsi delle oscillazioni di mercato. Non parliamo di scegliere il momento giusto per investire né di calcolare quantità perfette: il segreto è semplicemente continuare a comprare, con costanza, come un’abitudine di vita.

Questa filosofia, che a prima vista può sembrare quasi troppo elementare, si basa su un principio fondamentale: il mercato tende a salire nel lungo periodo, nonostante i fisiologici alti e bassi. Chi si ferma troppo spesso a calcolare rischia di rimanere immobilizzato dalla paura o dall'avidità, perdendosi le opportunità più importanti. Molti investitori cadono nella trappola del market timing: aspettano il momento perfetto per entrare o uscire dal mercato, nel tentativo di massimizzare i guadagni e minimizzare le perdite. È una tentazione comprensibile: nessuno vorrebbe investire appena prima di un crollo.

Ad esempio, all’inizio del 2017, con i principali indici azionari vicini ai massimi storici, molti si chiedevano se fosse il caso di aspettare una correzione. Chi ha esitato, però, si è perso un ulteriore periodo di crescita. Questa è una lezione universale: il mercato può rimanere sopravvalutato per molto più tempo di quanto si immagini. Una semplice ricerca online sulle azioni sopravvalutate in qualsiasi epoca storica, dagli anni ’20 a oggi, restituisce centinaia di articoli pieni di allarmi, che si sono spesso rivelati prematuri o infondati. Chi aspetta sempre il momento giusto spesso finisce per non investire mai o per entrare troppo tardi.

E nel frattempo, perde l'effetto più potente di tutti: il tempo.

La verità è che il mercato offre continuamente buone ragioni per essere pessimisti: crisi economiche, tensioni geopolitiche, recessioni, innovazioni tecnologiche dirompenti che cambiano le regole del gioco. Ma la storia insegna che chi ha continuato a investire, ignorando il rumore di fondo, è stato premiato. Proprio come si paga l'affitto ogni mese o si fa la spesa ogni settimana, investire deve diventare un'abitudine automatica, indipendente dall'umore del mercato.

Finché i costi di transazione sono bassi o nulli, la strategia migliore è quella di acquistare regolarmente, senza farsi paralizzare dalle emozioni o dalle notizie del momento.

Questa tecnica è nota come dollar cost averaging (DCA): investire somme fisse a intervalli regolari, comprando più quote quando i prezzi scendono e meno quote quando i prezzi salgono. Nel tempo, si riduce il rischio di investire tutto in un brutto momento e si approfitta della volatilità a proprio favore. Rispetto al DCA tradizionale, l'approccio del Just Keep Buying aggiunge una dimensione psicologica ancora più forte: non solo automatizzare gli investimenti, ma abituarsi mentalmente al fatto che il mercato salirà e scenderà, e che questo fa parte del gioco.

Market timing or time the market?

Market timing is the art, or perhaps it would be better to say the bet, of predicting market movements to decide the best time to buy or sell an investment. Those who practice market timing try to anticipate price rises or falls to maximize gains or limit losses, relying on technical analysis, economic indicators, mathematical models, or sometimes simple intuition. The idea of beating the market by entering and exiting at the right time is fascinating, but also very risky. Numerous studies show that systematically guessing market trends is extremely difficult, even for professionals. Errors in forecasting not only cancel out potential gains, but can also generate greater losses than those who adopt more passive strategies, such as simple buy and hold. Despite the difficulties, market timing continues to attract investors and traders around the world, driven by the hope, or illusion, of anticipating the future.

It is precisely on this instinct the other theory of «timing the market» is based. According to this idea, it is possible to improve one's earnings by anticipating market movements, that is, by carefully choosing when to enter and when to exit investments, thus avoiding downturns and riding on upturns. In words it sounds simple: just sell before crashes and buy before upturns. But in practice? Things get complicated. Consistently getting the right moments right has proven, over the years, to be an extremely difficult task even for professional managers. Prediction errors can turn the search for extra-gain into a trap erodes returns and increases costs.

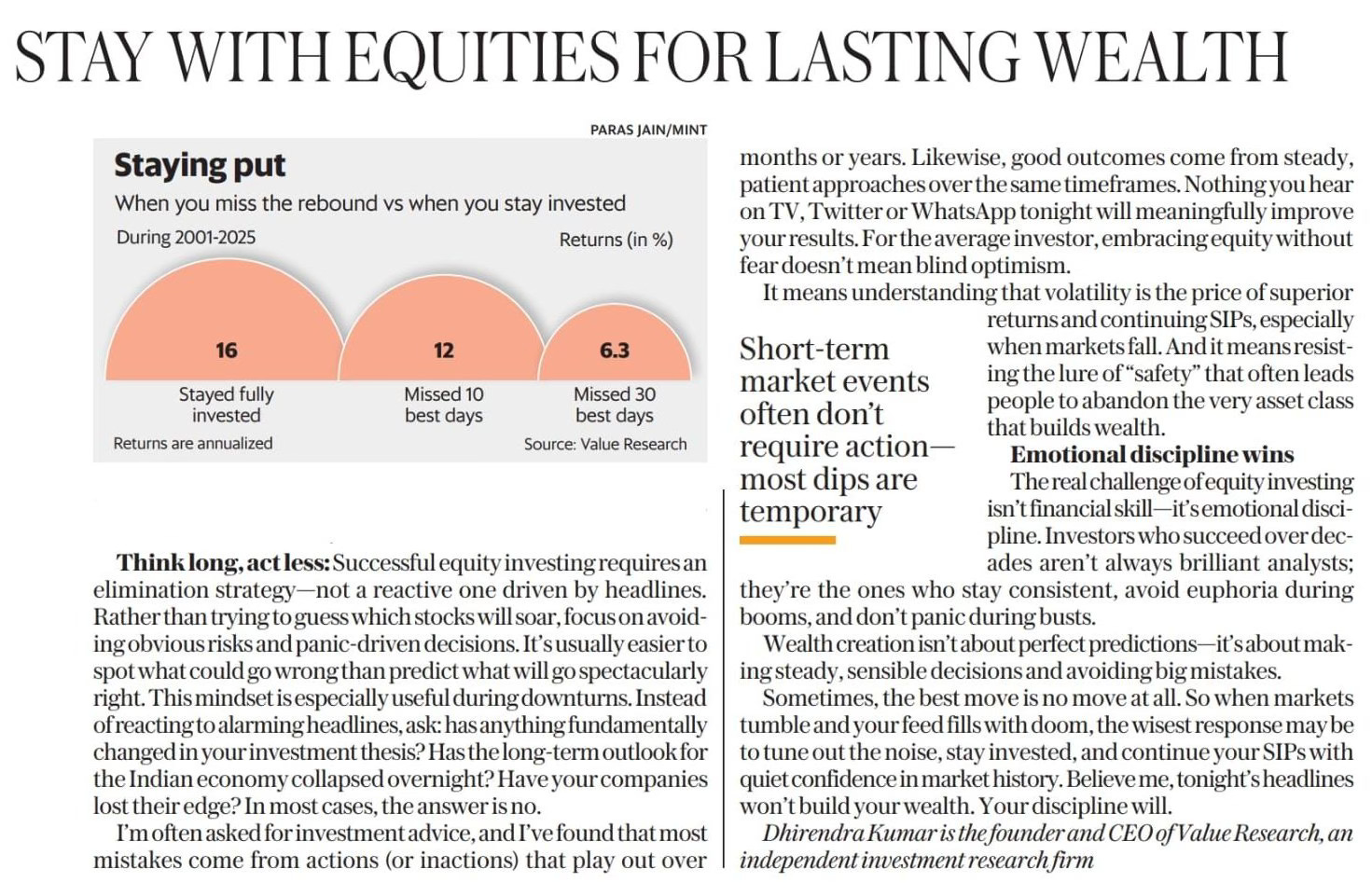

Those who believe in timing the market are opposed to the philosophy of time in the market, staying invested over the long term without trying to guess the ups and downs of the market, an approach that, data in hand, has often proven more effective precisely because it avoids missing out on the best days, the ones make the difference in annual returns. In short: timing theory is fascinating and promises great opportunities, but it hides even greater risks. And in the investment world, prudence often trumps presumption.

Market timing o time the market?

Il market timing è l'arte, o forse sarebbe meglio dire la scommessa, di prevedere i movimenti del mercato per decidere il momento migliore per comprare o vendere un investimento. Chi pratica il market timing cerca di anticipare i rialzi o i ribassi dei prezzi per massimizzare i guadagni o limitare le perdite, affidandosi ad analisi tecniche, indicatori economici, modelli matematici o, talvolta, al semplice intuito. L'idea di battere il mercato entrando e uscendo al momento giusto è affascinante, ma anche molto rischiosa. Numerosi studi dimostrano che indovinare sistematicamente l'andamento dei mercati è estremamente difficile, persino per i professionisti. Errori di previsione non solo annullano i potenziali guadagni, ma possono anche generare perdite maggiori rispetto a chi adotta strategie più passive, come il semplice compra e tieni. Nonostante le difficoltà, il market timing continua ad attrarre investitori e trader di tutto il mondo, spinti dalla speranza, o dall'illusione, di anticipare il futuro.

È proprio su questo istinto che si basa l’altra teoria del «timing the market». Secondo questa idea, è possibile migliorare i propri guadagni anticipando i movimenti del mercato, ovvero scegliendo con attenzione quando entrare e quando uscire dagli investimenti, evitando così i periodi di ribasso e cavalcando quelli di crescita. A parole sembra semplice: basta vendere prima dei crolli e comprare prima delle riprese. Ma nella pratica? Le cose si complicano.

Azzeccare costantemente i momenti giusti si è rivelato, negli anni, un compito estremamente difficile anche per i gestori professionisti. Errori di previsione possono trasformare la ricerca di un extra-guadagno in una trappola che erode rendimenti e aumenta i costi.

Chi crede nel timing the market si contrappone alla filosofia del time in the market, rimanere investiti nel lungo periodo senza cercare di indovinare i saliscendi del mercato, un approccio che, dati alla mano, si è dimostrato spesso più efficace proprio perché evita di perdersi i giorni migliori, quelli che fanno la differenza nei rendimenti annuali. In breve: la teoria del timing è affascinante e promette grandi opportunità, ma nasconde rischi ancora più grandi. E nel mondo degli investimenti, la prudenza spesso batte la presunzione.

Just keep buying

To understand how powerful long-term investment theory is, just think of an exemplary story. Between 1973 and 2007, one investor made four major purchases at disastrous times:

in 1973, before a 48% crash

in 1987, just before «Black Monday»

in 2000, on the threshold of the collapse of the Internet bubble

in 2007, just before the Great Recession

In short, the worst possible timing. Yet by investing just under $200,000 in total and never selling, this investor saw his capital grow to about $980,000, with an average annual return of 9%. The lesson is clear: it doesn't matter when you buy, it matters that you don't sell. Selling during a crisis often means freezing losses and losing the chance to participate in the recovery. To build wealth, you need to accumulate capital and let it work for itself, resisting the temptations to panic.

Another useful concept to know is the price-to-earnings ratio, which measures the price of a stock relative to its annual earnings. Historically, a high P/E is associated with lower future returns, and vice versa. When stocks are expensive, returns tend to decline in the short to medium term (5 years). However, as you lengthen the time horizon, 20 or 30 years, correlation between P/E and returns weakens. In the long term, maintaining the investment matters much more than any initial valuation. For example, in the United States, over 20-year periods there have been no negative real returns when including dividends, and over 30 years returns tend to converge, even starting from high valuations. In other words: time in the market beats trying to beat the market.

The real challenge is psychological: staying invested requires nontrivial mental strength. It is easy to buy when everything is going well, prices are going up, and the news is optimistic. It is much harder to keep buying when the market crashes, confidence evaporates and pessimism is everywhere. Yet it is precisely in times of crisis the best bargains are created. History confirms this: markets tend to rebound after periods of panic, rewarding those who have stuck to their strategy. Despite the natural desire to protect oneself by selling in difficult times, it is essential to hold on. Because, as trading volumes also show, most investors tend to sell on lows and buy on highs, exactly the opposite of what should be done.

Building wealth through investing is not a matter of financial brilliance, impeccable forecasting or perfect timing. Rather, it is the result of simple, repeated habits over time: saving, investing regularly, staying the course in hard times. Buy, hold and forget is not just practical advice, but a real mindset toward the market and toward one's financial future. We are not the first to talk about it and we will not be the last to think about it. Act now, because tomorrow is another day lost without investing.

Continua a comprare

Per capire quanto sia potente la teoria dell’investimento nel lungo periodo, basti pensare a una storia esemplare. Tra il 1973 e il 2007, un investitore compì quattro acquisti importanti in momenti disastrosi:

nel 1973, prima di un crollo del 48%

nel 1987, subito prima del «lunedì nero»

nel 2000, alle soglie del crollo della bolla internet

nel 2007, poco prima della Grande Recessione

Insomma, il peggior tempismo possibile. Eppure, investendo poco meno di 200.000 dollari in totale e non vendendo mai, questo investitore ha visto il suo capitale crescere fino a circa 980.000 dollari, con un rendimento medio annuo del 9%. La lezione è chiara: non importa quando compri, importa che tu non venda. Vendere durante una crisi significa spesso congelare le perdite e perdere la possibilità di partecipare alla ripresa. Per costruire ricchezza, bisogna accumulare capitale e lasciarlo lavorare per sé, resistendo alle tentazioni di panico.

Un altro concetto utile da conoscere è il rapporto prezzo/utili, che misura il prezzo di un'azione rispetto ai suoi utili annuali. Storicamente, un P/E elevato è associato a rendimenti futuri più bassi, e viceversa. Quando le azioni sono care, i rendimenti tendono a ridursi nel breve-medio periodo (5 anni). Tuttavia, man mano che si allunga l'orizzonte temporale, 20 o 30 anni, la correlazione tra P/E e rendimenti si indebolisce. Nel lungo termine, mantenere l'investimento conta molto di più di qualsiasi valutazione iniziale. Ad esempio, negli Stati Uniti, su periodi di 20 anni non ci sono stati rendimenti reali negativi quando si includono i dividendi, e su 30 anni i ritorni tendono a convergere, anche partendo da valutazioni elevate. In altre parole: il tempo sul mercato batte il tentativo di battere il mercato.

La vera sfida è psicologica: restare investiti richiede una forza mentale non banale. È facile acquistare quando tutto va bene, i prezzi salgono e le notizie sono ottimistiche. È molto più difficile continuare a comprare quando il mercato crolla, la fiducia evapora e ovunque si respira pessimismo. Eppure, è proprio nei momenti di crisi che si creano le occasioni migliori. La storia lo conferma: i mercati tendono a rimbalzare dopo i periodi di panico, premiando chi è rimasto fedele alla propria strategia. Nonostante il naturale desiderio di proteggersi vendendo nei momenti difficili, è essenziale resistere. Perché, come dimostrano anche i volumi di scambio, la maggior parte degli investitori tende a vendere sui minimi e comprare sui massimi, esattamente il contrario di ciò che bisognerebbe fare.

Costruire ricchezza attraverso gli investimenti non è questione di genialità finanziaria, di previsioni impeccabili o di tempismo perfetto. È piuttosto il risultato di abitudini semplici e ripetute nel tempo: risparmiare, investire con regolarità, mantenere la rotta nei momenti difficili. Comprare, mantenere e dimenticarsi non è solo un consiglio pratico, ma un vero e proprio atteggiamento mentale verso il mercato e verso il proprio futuro finanziario. Non siamo i primi a parlarne e non saremo gli ultimi a pensarlo. Agisci adesso, perché domani è un altro giorno perso, senza investire.