Paper Silver

Between leverage, silver and systemic risk: what price fluctuations really tell us

Silver is one of the markets very quickly cease to behave like simple investment instruments. The more you observe it, the more it becomes clear the price is not just about the metal, but something else, a deeper tension running through the entire financial system.

Every sudden jump, every acceleration followed by a brutal compression, every seemingly irrational movement is not a hiccup, but a signal, almost a nervous reflex, of a balance that rests on fragile assumptions. Seen in this light, the recent price rollercoaster is neither an exceptional event nor a temporary distortion: it is the consistent manifestation of a market structure has been suspended for years, sustained more by confidence in paper, promises and derivatives than by the actual availability of physical underlying asset.

L’argento è uno di quei mercati che smettono molto presto di comportarsi come semplici strumenti di investimento. Più lo si osserva, più diventa evidente che il prezzo non sta parlando solo del metallo, ma di qualcos’altro, di una tensione più profonda che attraversa l’intero sistema finanziario.

Ogni scatto improvviso, ogni accelerazione seguita da una compressione brutale, ogni movimento apparentemente irrazionale non è un incidente di percorso, ma un segnale, quasi un riflesso nervoso, di un equilibrio che si regge su presupposti fragili. Le recenti montagne russe del prezzo, lette in questa chiave, non sono né un evento eccezionale né una distorsione temporanea: sono la manifestazione coerente di una struttura di mercato che da anni vive sospesa, sostenuta più dalla fiducia nella carta, nelle promesse e nei derivati che dalla disponibilità effettiva del sottostante fisico.

Margin calls coming for silver?

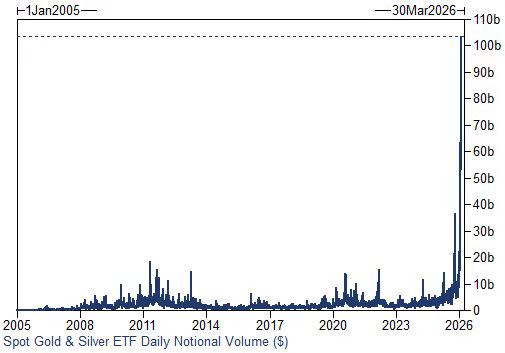

Unlike gold, silver is a small, relatively shallow market that is extremely sensitive to financial flows and therefore ideal for amplification by leverage, because even a relatively small amount of capital, if appropriately multiplied through derivatives, is enough to produce price movements appear disproportionate to the dynamics of real economy. This is where speculation finds its natural terrain, not as a pathological deviation from the system, but as its structural component. In fact, silver is now traded mainly as a financial exposure and only marginally as a physical commodity, with an ever-widening gap between what exists in warehouses and what is promised on the markets.

When price begins to rise sharply, narrative quickly changes and is enriched with justifications that, taken individually, are well-founded, from industrial demand linked to the energy transition to growing use in high-tech sectors, but which together end up masking the real driver of short- and mid-term movements, which remains financial and linked to the very structure of the derivatives market. Futures, options, funds and securitized instruments build up exposure to silver almost never requires ownership of the metal, creating a mass of «paper silver» that grows much faster than available physical supply, making the system efficient only as long as no one asks to convert paper into actual delivery.

It is in this context that cyclical lowering of leverage should be understood, which invariably occurs at times of greatest tension, when price approaches levels put the entire market architecture under stress. The increase in margins, the tightening of requirements and forced reduction of exposure are not neutral events or simple technical risk management measures, but actual mechanisms for controlling systemic volatility, because in a market such as silver, leverage is not an accessory, it is the supporting structure and allowing it to grow unchecked while price accelerates means accepting a level of instability the system is not willing to tolerate.

Chiamate a margine in arrivo sull’argento?

L’argento, a differenza dell’oro, è un mercato piccolo, relativamente poco profondo, estremamente sensibile ai flussi finanziari e proprio per questo ideale per essere amplificato dalla leva, perché basta una quantità di capitale non particolarmente elevata, se opportunamente moltiplicata tramite derivati, per produrre movimenti di prezzo che appaiono sproporzionati rispetto alle dinamiche dell’economia reale. È qui che la speculazione trova il suo terreno naturale, non come deviazione patologica del sistema, ma come sua componente strutturale. L’argento infatti, oggi viene scambiato prevalentemente come esposizione finanziaria e solo marginalmente come bene fisico, con una distanza sempre più ampia tra ciò che esiste nei magazzini e ciò che viene promesso sui mercati.

Quando il prezzo inizia a salire con decisione, la narrativa cambia rapidamente e si arricchisce di giustificazioni che, prese singolarmente, sono anche fondate, dalla domanda industriale legata alla transizione energetica fino all’utilizzo crescente in settori ad alta tecnologia, ma che nel loro insieme finiscono per mascherare il vero motore dei movimenti di breve e medio periodo, che rimane finanziario e legato alla struttura stessa del mercato dei derivati. Futures, opzioni, fondi e strumenti cartolarizzati, costruiscono un’esposizione all’argento che non richiede quasi mai il possesso del metallo, creando una massa di «argento di carta» che cresce molto più rapidamente dell’offerta fisica disponibile, rendendo il sistema efficiente solo finché nessuno chiede di trasformare quella carta in consegna reale.

È in questo contesto che va letto l’abbassamento ciclico della leva finanziaria, che puntualmente arriva nei momenti di maggiore tensione, quando il prezzo si avvicina a livelli che mettono sotto stress l’intera architettura del mercato. L’aumento dei margini, l’inasprimento dei requisiti, la riduzione forzata dell’esposizione, non sono eventi neutrali né semplici misure tecniche di gestione del rischio, ma veri e propri meccanismi di controllo della volatilità sistemica, perché in un mercato come quello dell’argento la leva non è un accessorio, è la struttura portante, e lasciarla crescere indisturbata mentre il prezzo accelera significa accettare un livello di instabilità che il sistema non è disposto a tollerare.

The compression and release cycle

Many people see these moves as a deliberate attempt to cap the price, but this interpretation, while intuitive, is incomplete, because the problem is not the price level itself, but rather the sustainability of chain of promises that price supports. If leverage remains high and prices continue to rise, risk is not only for the most exposed speculators, but for the entire clearing system, because margin calls don’t occur in isolation; they spread, triggering cascading liquidations and quickly transforming an already volatile market into a source of systemic instability. Reducing leverage therefore means buying time, cooling the dynamics and bringing the market back within manageable limits, without, however, addressing the central issue.

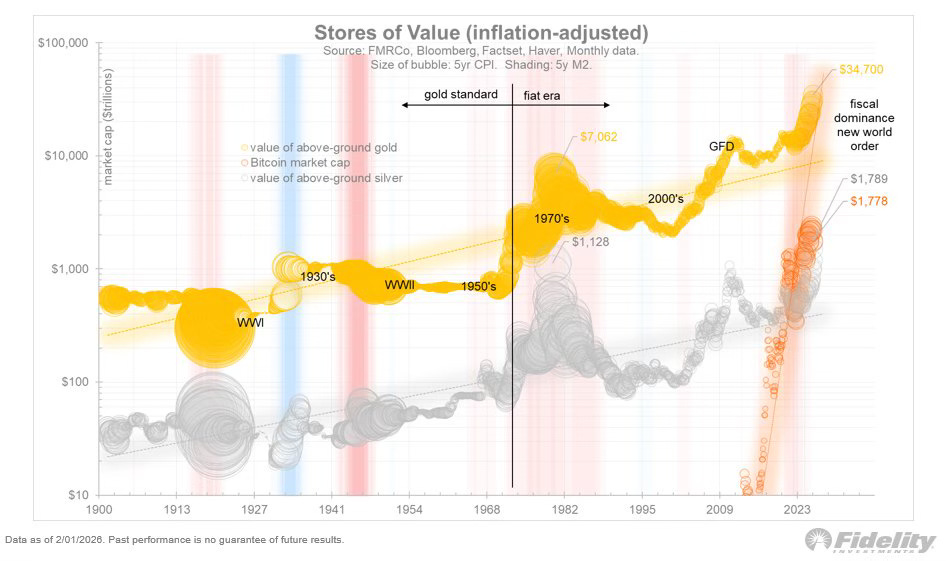

That issue is the extreme securitization of silver, which appears increasingly out of control when viewed in relation to the physical availability of the metal, as is clearly evident from various macro-financial aggregators compare the volume of financial promises with actual reserves. The point is not tomorrow everyone will demand delivery of silver, because this scenario is unlikely, but the system only works as long as majority of operators implicitly accept traded silver is an accounting concept rather than a physical asset, a financial representation thrives on monetary regulations rather than physical transfers.

This growing distance between physical reality and financial representation creates a tension that cannot be resolved in a linear fashion, but manifests itself through cycles of compression and release, phases in which the price attempts to express something about the state of the system and is quickly brought back within a range compatible with the current financial structure. Every time this happens, narrative changes, volatility explodes, confidence falters, but the underlying problem remains intact, because it doesn’t concern silver as such, but rather the way in which the financial system manages real scarcity through instruments that presuppose infinite abundance.

Il ciclo di «compressione e rilascio»

Molti interpretano questi interventi come una volontà deliberata di reprimere il prezzo, ma questa lettura, pur intuitiva, è incompleta, perché il problema non è il livello del prezzo in sé, bensì la sostenibilità della catena di promesse che quel prezzo sostiene. Se la leva rimane elevata e il prezzo continua a salire, il rischio non è solo per gli speculatori più esposti, ma per l’intero sistema di compensazione, perché le margin call non avvengono in isolamento, si propagano, innescano liquidazioni a cascata e trasformano rapidamente un mercato già volatile in una fonte di instabilità sistemica. Ridurre la leva significa quindi guadagnare tempo, raffreddare la dinamica, riportare il mercato entro limiti gestibili, senza affrontare però il nodo centrale.

Quel nodo è la cartolarizzazione estrema dell’argento, che appare sempre più fuori controllo se osservata in rapporto alla disponibilità fisica del metallo, come emerge chiaramente da diversi aggregatori macro-finanziari che mettono a confronto il volume delle promesse finanziarie con le riserve reali. Il punto non è che domani tutti chiederanno la consegna dell’argento, perché questo scenario è improbabile, ma che il sistema funziona solo finché la maggioranza degli operatori accetta implicitamente che l’argento scambiato sia un concetto contabile più che un bene fisico, una rappresentazione finanziaria che vive di regolamenti monetari e non di trasferimenti materiali.

Questa distanza crescente tra realtà fisica e rappresentazione finanziaria crea una tensione che non può essere risolta in modo lineare, ma che si manifesta attraverso cicli di compressione e rilascio, fasi in cui il prezzo tenta di esprimere qualcosa sullo stato del sistema e viene rapidamente riportato all’interno di un range compatibile con l’attuale struttura finanziaria. Ogni volta che ciò accade, la narrativa cambia, la volatilità esplode, la fiducia vacilla, ma il problema di fondo rimane intatto, perché non riguarda l’argento in quanto tale, bensì il modo in cui il sistema finanziario gestisce la scarsità reale attraverso strumenti che presuppongono abbondanza infinita.

Stores of value

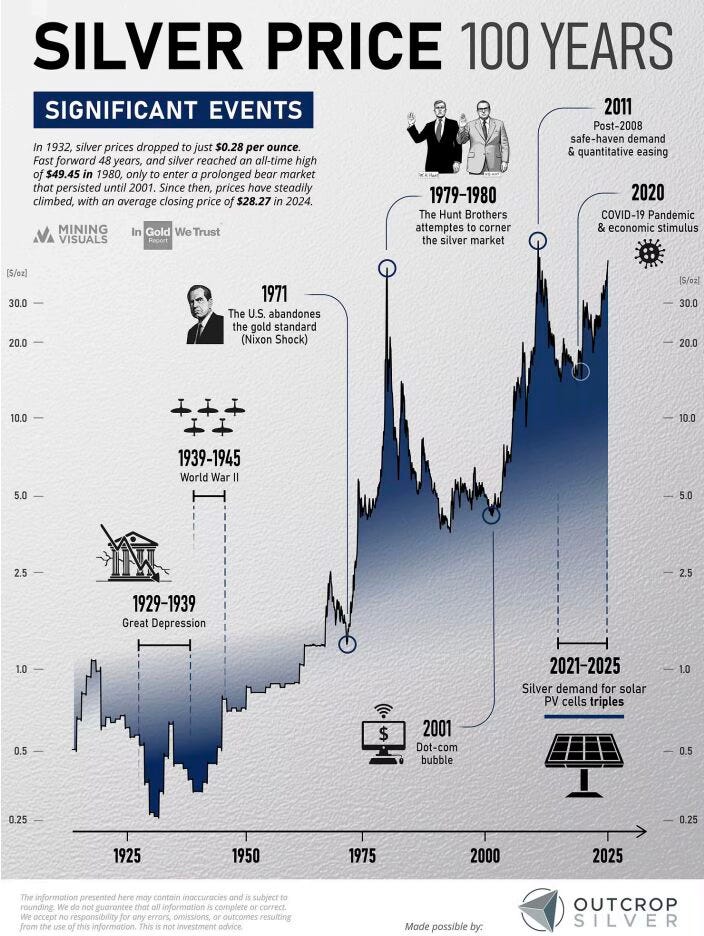

A common mistake is to view silver as an immediate hedge against inflation or systemic risk, without taking into account that, just because of its small size and high financialization, in the short term it tends to suffer more than other assets when financial conditions tighten or liquidity is withdrawn. This is not a paradox, but a direct consequence of the market structure, because what makes silver attractive as a real asset in the long term makes it vulnerable to leverage and speculation in the short term.

Observing silver therefore means observing a market that offers no certainties, doesn’t follow clear trajectories and punishes those who seek simple confirmation of preconceived ideas, but which, precisely for this reason, provides valuable information on the state of the financial system as a whole. Each of its rollercoaster rides is not a noise to be ignored, but a sign of stress shows how the thin line has become between finance and physical reality, paper promises and real assets, apparent stability and structural fragility.

Magazzini di valore

Un errore frequente è considerare l’argento come una copertura immediata contro l’inflazione o contro il rischio sistemico, senza tenere conto che, proprio a causa della sua dimensione ridotta e della sua elevata finanziarizzazione, nel breve periodo tende a soffrire più di altri asset quando le condizioni finanziarie si irrigidiscono o la liquidità viene ritirata. Questo non è un paradosso, ma una conseguenza diretta della struttura del mercato, perché ciò che nel lungo periodo rende l’argento interessante come asset reale, nel breve lo rende vulnerabile alle dinamiche della leva e della speculazione.

Osservare l’argento significa quindi osservare un mercato che non offre certezze, che non segue traiettorie pulite e che punisce chi cerca conferme semplici a tesi già decise, ma che proprio per questo fornisce informazioni preziose sullo stato del sistema finanziario nel suo complesso. Ogni sua montagna russa non è un rumore da ignorare, ma un segnale di stress che racconta quanto sia diventato sottile il confine tra finanza e realtà fisica, tra promesse cartacee e beni reali, tra stabilità apparente e fragilità strutturale.