Just an Illusion

Bundestag has passed a $20 billion energy bill to finance the construction of a massive hydrogen central grid across the country. Could it work? Current macro-financial-economic point of Germany

After many months of debate inside German politics and among national institutions, left-wing government led by Olaf Scholz has approved a reform of the national energy law that includes funding for a new hydrogen-fueled central grid. Two-decade project requires more than 20 billion to enable transition away from fossil fuels in hard-to-burn sectors. Germany was the country most affected in Europe by reduction in Russian gas supplies and has since doubled down on the prospects of accelerating the emissions reduction process with energy transition.

Berlin has one of the most ambitious energy strategies in the EU: it plans to be climate neutral by 2045, five years ahead of the European Green Deal target, and aims to cover at least 80% of electricity consumption with renewable energy by 2030. The new Hydrogen Core Grid, extended 9,700 km, will be needed to de-carbonize remaining parts of the economy. According to Vice Chancellor and Energy Minister Robert Habeck, construction of the hydrogen core grid could now begin, as government has secured funding for the grid plan.

Dopo molti mesi di discussioni all'interno della politica tedesca e tra le istituzioni nazionali, il governo di sinistra guidato da Olaf Scholz ha approvato una riforma della legge nazionale sull'energia, che prevede il finanziamento di una nuova rete centrale a idrogeno. Il progetto, della durata di due decenni, richiede oltre 20 miliardi di euro per consentire la transizione dai combustibili fossili di settori difficili da abbattere. La Germania è stato il Paese più colpito in Europa dalla riduzione delle forniture di gas russo e da allora ha raddoppiato le prospettive di accelerare il processo di riduzione delle emissioni con la transizione energetica.

Berlino ha una delle strategie energetiche più ambiziose dell'Unione Europea: prevede di essere neutrale dal punto di vista climatico entro il 2045, con cinque anni di anticipo rispetto all'obiettivo del Green Deal Europeo, e punta a coprire almeno l'80% del consumo di elettricità con energie rinnovabili entro il 2030. La nuova Hydrogen Core Grid, estesa per 9.700 km, sarà necessaria per de-carbonizzare le restanti parti dell'economia. Secondo il vice-cancelliere e ministro dell'Energia Robert Habeck, la costruzione della rete centrale a idrogeno potrebbe ora iniziare, dato che il governo ha assicurato il finanziamento del piano di rete.

Hydrogen's unknowns

Berlin intends to support the creation of a hydrogen network by covering network tariffs until 2055, which should be introduced by 2025 for all operators. Financing network is the milestone of all measures needed to achieve a true hydrogen economy within the next two decades. German government will intervene by limiting network tariffs to prevent prices from rising above market prices, allowing German industries to be competitive in the global economy and, at the same time, network to expand.

EU Parliament, which will oversee the construction and coordination of hydrogen networks, recently recognized importance of green electricity and green gas in a new set of laws governing the transition from gas to renewables. As locomotive of Europe, Germany has convinced the EU Parliament to allow municipal companies to own local networks, while European institutions have sought to clearly separate hydrogen and gas operators. However, there are many unknowns regarding hydrogen, and some of them Doomberg has debunked in one of his juicy articles, Natural Hydrogen: Something or Nothing?

Le incognite dell'idrogeno

Berlino intende sostenere la creazione di una rete a idrogeno coprendo le tariffe di rete fino al 2055, che dovrebbero essere introdotte entro il 2025 per tutti gli operatori. Il finanziamento della rete è la pietra miliare di tutte le misure necessarie per realizzare una vera e propria economia dell'idrogeno entro i prossimi due decenni. Il governo tedesco interverrà limitando le tariffe di rete per evitare che i prezzi aumentino oltre i prezzi di mercato, consentendo alle industrie tedesche di essere competitive nell'economia globale e, allo stesso tempo, alla rete di espandersi.

Il Parlamento Europeo, che si occuperà di supervisionare la costruzione e il coordinamento delle reti ad idrogeno, ha da poco riconosciuto l'importanza dell'elettricità verde e dei gas verdi in una nuova serie di leggi che regolano la transizione dal gas alle fonti rinnovabili. In qualità di locomotiva d’Europa, la Germania ha convinto il Parlamento Europeo a consentire alle aziende municipali di possedere reti locali, mentre le istituzioni europee hanno cercato di separare nettamente gli operatori ad idrogeno da quelli del gas. Tuttavia, ci sono molte incognite per quanto riguarda l'idrogeno, e alcune di esse le ha sfatate Doomberg in uno dei suoi succulenti articoli, Natural Hydrogen: Something or Nothing?.

Put things into right perspective

Truth is that wherever you try to find it, energy is life, and life doesn’t come out of nothing. The law that governs the universe, «nothing is lost, nothing is created, everything is transformed» (Antoine-Laurent Lavoisier, French chemist and physicist, ed.), has stood test of time, and we believe this is another bizarre stunt on the part of the dastardly German political class. We leave it to the experts to draw conclusions. From our side we can look at the data, markets and signals coming from the economy to see where we are heading. Recently Christine Lagarde, responding to a question from CNBC, said that «German manufacturing may have turned around». From a closer look at the data, it clearly appears that is totally skewed if we look in the right perspective on which we are relating the actual data. Let's dig in.

The baffling way of dealing with problems in Germany is something to be studied. Concept currently tested by German policy to combat climate change is essentially to:

shut down nuclear power plants: effectively shutting down Europe's only engine of self-generated energy subsistence;

keep coal mines active because it is better to pretend to go green in the public eye and capture a few more votes while the inevitable happens;

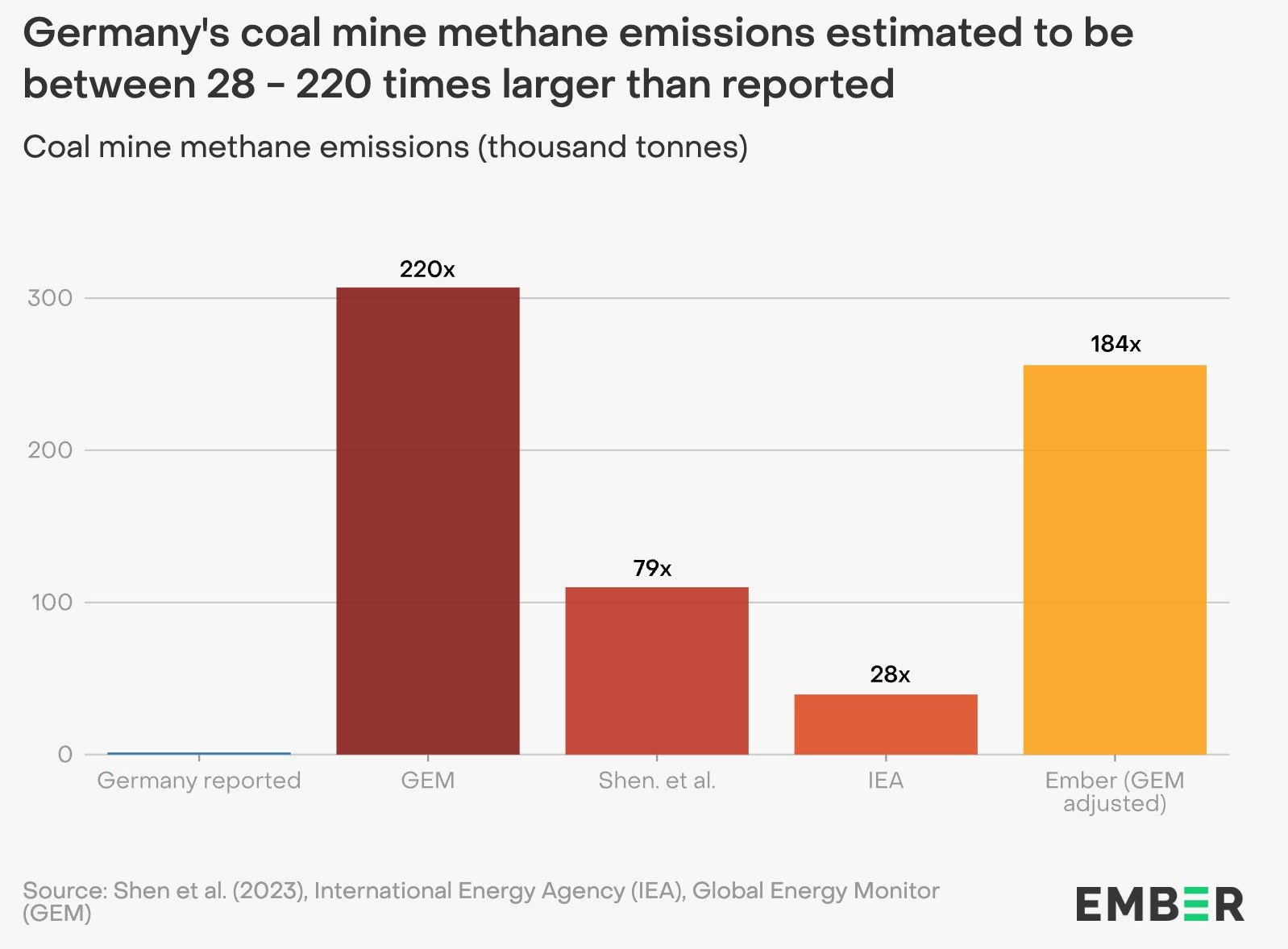

underestimate emissions just as some papers and studies have shown but without arbitrarily choosing the starting point, which is fundamental to any study not written by lobbyists. Brilliant isn't it?

Mettere le cose nella giusta prospettiva

La verità è che dovunque si cerchi di trovare, l’energia è vita e la vita non viene fuori dal nulla. La legge che regola l’universo, «nulla si crea, nulla si distrugge, tutto si trasforma» (Antoine-Laurent Lavoisier, chimico e fisico francese, ndr), ha superato la prova del tempo e crediamo che questa sia un’altra trovata bizzarra da parte della scellerata classe politica tedesca. Lasciamo agli esperti le conclusioni. Dal nostro lato possiamo guardare ai dati, ai mercati e ai segnali che vengono dall’economia per capire dove ci stiamo dirigendo. Recentemente Christine Lagarde, rispondendo ad una domanda della CNBC, ha affermato che «la produzione tedesca potrebbe aver svoltato». Da una più attenta osservazione dei dati, pare chiaramente che questa cosa si totalmente distorta se guardiamo la prospettiva corretta su cui stiamo rapportando i dati reali. Scaviamo a fondo.

Lo sconcertante modo di affrontare i problemi in Germania è un qualcosa da studiare. Il concetto attualmente collaudato dalla politica tedesca per combattere il cambiamento climatico è essenzialmente quello di:

chiudere le centrali nucleari: spegnendo di fatto l’unico motore di sussistenza energetica autoprodotta dall’Europa;

mantenere attive le miniere di carbone: perchè meglio far finta di diventare eco-sostenibili di fronte all’opinione pubblica e catturare qualche voto in più, mentre l’inevitabile accade;

sottostimare le emissioni: così come alcuni papers e studi hanno dimostrato senza però scegliere arbitrariamente il punto di partenza, fondamentale per qualsiasi studio non scritto dalle lobby. Geniale vero?

DAX crushed on itself

Into this climate of total detachment from reality comes the financial markets and DAX. Since October 2023 and more generally, since post-pandemic crisis, the German Index has doubled in value and increased by 30% in the last six-months. Crucial shift from 30 to 40 stocks has changed some of the valuation characteristics of companies within the index: criteria for DAX membership has become primarily market capitalization, which means total stock market value of the company. Trading volume will no longer take priority.

This reform was a direct response by Deutsche Börse to the Wirecard scandal. From then on, companies must remain profitable for two years without interruption before being admitted. Looking back over past ten years, we see an increase of more than 8,000 points resulting from only 11 companies. Bayer has been tail end and has put a strain on the index, weighing in with a negative performance of 600 points, just as appearance of HelloFresh and Delivery-Hero cost the index over 245 points.

If we take into analysis only the last six-months of trading of DAX Index, we note gain is more than 20%, or over 3,000 points. Two-thirds of this performance is from the activity of 6 stocks: SAP +637 points, which also leads index in terms of absolute weight (more than 10%, ed.), Siemens AG +435 points, Airbus +366 points, Allianz +240 points, Rheinmetall AG +189 points, with its galactic performance after outbreak of the war between Russia and Ukraine, and BASF +149 points, while Bayer has remained the tail end with -232 points of loss since October 2023.

DAX schiacciato su se stesso

In questo clima di totale distacco dalla realtà, si inseriscono i mercati finanziari e il DAX. Da Ottobre 2023 e più in generale, dalla crisi post-pandemica, l’Indice tedesco a raddoppiato il suo valore e aumentato del 30% negli ultimi sei mesi. Il cruciale passaggio da 30 a 40 titoli ha cambiato alcune caratteristiche di valutazione delle aziende all’interno dell’indice: il criterio per l'appartenenza al DAX è diventato principalmente la capitalizzazione di mercato, che significa il valore totale del mercato azionario della società. Il volume di scambio non avrà più la precedenza.

Questa riforma fu una risposta diretta di Deutsche Börse allo scandalo Wirecard. Da quel momento in poi, le aziende devono rimanere redditizie per due anni senza interruzione prima di essere ammesse. Guardando indietro agli ultimi dieci anni, vediamo un aumento di oltre 8,000 punti derivante soltanto da 11 aziende. Bayer è stato il fanalino di coda ed ha messo a dura prova l’indice, pesando con una performance negativa di 600 punti, così come l’apparizione di HelloFresh e Delivery-Hero è costata all’indice oltre 245 punti.

Se prendiamo in analisi soltanto gli ultimi sei mesi di contrattazione dell’Indice DAX, notiamo che il guadagno è superiore al 20%, ovvero oltre 3,000 punti. Due terzi di questa performance è derivante dall’attività di 6 titoli: SAP +637 punti, che guida l’indice anche in termini di peso assoluto (oltre il 10%, ndr), Siemens AG +435 punti, Airbus +366 punti, Allianz +240 punti, Rheinmetall AG +189 punti, con la sua performance galattica dopo lo scoppio della guerra tra Russia e Ucraina e BASF +149 punti, mentre Bayer è rimasta fanalino di coda con 232 punti di perdita da Ottobre 2023.

Zero-sum game

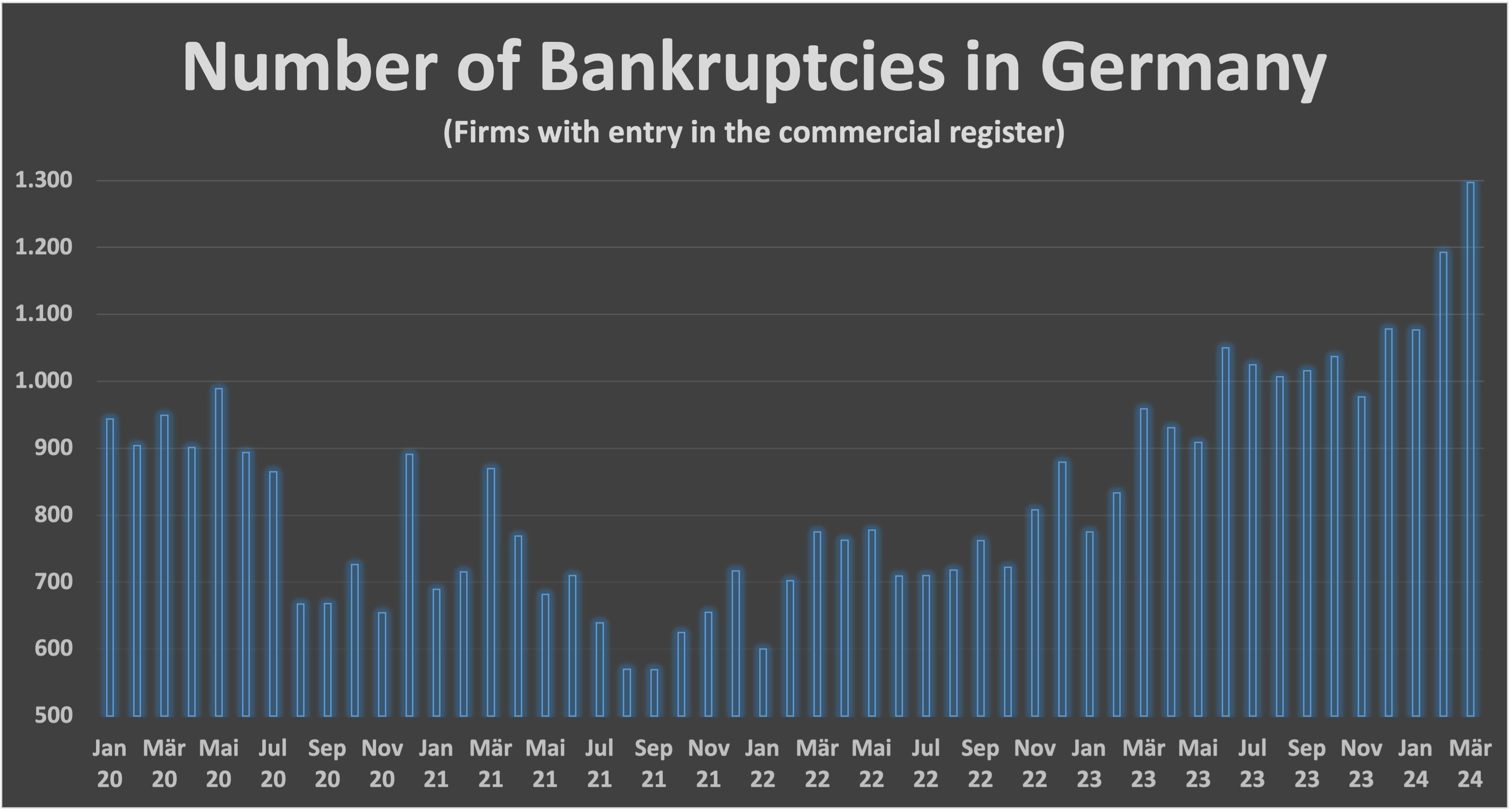

It seems clear things have gotten even worse since the end of September 2021, when DAX was raised to 40 companies: entire increase of about 3,000 points came from the usual 6 stocks. This shows that net of earnings and a few magnificent stocks (DAX includes dividends, ed.) German Index has turned out to be a mostly zero-sum game. If we broaden the spectrum of analysis by moving outside the box of markets and look deep into the real economy, we see that number of corporate bankruptcies reached a new record high in March 2024. According to the IWH Institute, the number of insolvencies of partnerships and companies more generally in Germany increased by 9% on a monthly basis. Current number is also 35% higher than in March 2023 and 30% higher than March average for the years from 2015-2020, just before pandemic.

In short, if we avoid trees and extend our gaze to the forest, outlook for the Q2 of 2024 may be less exciting than what markets have been telling us so far. With inflation expectations recently increased significantly, an imminent rate cut by ECB, but still less than the pace expected at this point in the year, we can assume the best is behind us. Iran's entry into the Middle East conflict may cause further delays in European trade to and from Germany: import/export volumes have come to a complete standstill in recent months.

Geopolitical scenario leaves so many doubts for investors, who are divided between the mad desire to join the bullish party and caution to try entries at better prices. The quarterly reports in the US will do the rest: in the coming weeks, results of Meta (April 24) Microsoft and Google (April 25) Amazon (April 30) Apple (May 5) and Nvidia (May 22) will be released. Will we resume the bullish march or honeymoon will be just an illusion?

Gioco a somma zero

Pare evidente che le cose sono peggiorate ulteriormente da fine Settembre 2021, quando il DAX è stato portato a 40 aziende: l'intero incremento di circa 3,000 punti è derivato dai soliti 6 titoli. Ciò mostra che al netto degli utili e di pochi magnifici titoli (il DAX include i dividendi, ndr) l’indice tedesco è risultato un gioco per lo più a somma zero. Se allarghiamo lo spettro di analisi spostandoci fuori dagli schemi dei mercati e guardiamo in profondità verso l’economia reale, vediamo che il numero di fallimenti aziendali ha raggiunto un nuovo record a Marzo del 2024. Secondo l’Istituto IWH, il numero di insolvenze di società di persone e società più in generale in Germania è aumentato del 9% su base mensile. Anche il numero attuale è superiore del 35% rispetto a Marzo 2023 e del 30% superiore alla media di Marzo degli anni dal 2015-2020, ovvero poco prima della pandemia.

Insomma se evitiamo di vedere gli alberi e allunghiamo lo sguardo verso la foresta, le prospettive del secondo trimestre del 2024 potrebbero essere meno entusiasmanti di quelle che i mercati ci hanno raccontato fino ad oggi. Con le aspettative di inflazione recentemente aumentate in modo significativo, una diminuzione dei tassi imminente da parte della BCE, ma comunque inferiore al ritmo che ci si aspettava a questo punto dell’anno, possiamo dedurre che il meglio è alle spalle. L’entrata dell’Iran nel conflitto in Medio Oriente potrebbe causare ulteriori ritardi nel commercio Europeo da e verso la Germania: negli ultimi mesi il volume di import/export si è completamente fermato.

Lo scenario geopolitico lascia tanti dubbi agli investitori, divisi tra la voglia matta di partecipare alla festa del rialzo e la prudenza nel provare ingressi a prezzi migliori. Le trimestrali negli Stati Uniti faranno il resto: nelle prossime settimane verranno diffusi i risultati di Meta (24 Aprile) Microsoft e Google (25 Aprile) Amazon (30 Aprile) Apple (5 Maggio) e Nvidia (22 Maggio). Riprenderemo la marcia rialzista oppure la luna di miele sarà solo un illusione?

It's one of my favorite songs 😂

I really don't understand how they think of implementing the plan by replacing coal, oil and nuclear with sun and wind. The ecological fairy tale is adrift.