Holistic Financial Advice

Putting the customer back at the center: the new paradigm of financial advice

We live in times when polarization is creeping into every area of society. It is no longer just politics that is divided into opposing factions, but also science, culture, sports, and even finance. In our industry, this trend has taken shape in a silent but constant conflict: the opposition between advisors and active managers. It is a cold war that is not fought with weapons, but articles, social media posts, presentation slides, and vitriolic remarks at industry conferences.

Anyone on LinkedIn, Reddit, or investment discussion forums is well aware of this. On the first side, we find advisors who denigrate active management, accusing it of being expensive, inefficient, and lacking transparency. On the other, we have managers who proudly defend their profession, convinced that without them markets would be flat, devoid of opportunities and dynamics. In the middle are clients, who rarely have tools to decipher the debate and too often find themselves confused, with a question that no one seems willing to really address: who should I believe?

The reality, as is often the case, is much more nuanced than it is portrayed. Yet simplification suits everyone: the advisor who wants to stand out, manager who wants to defend their model, the marketing department thrives on slogans. But this binary logic is dangerous because it shifts the focus away from the real goal: client's financial peace of mind. Let's take a closer look.

Viviamo in tempi in cui la polarizzazione si insinua in ogni ambito della società. Non è più solo la politica a dividersi in fazioni contrapposte, ma anche la scienza, la cultura, lo sport e persino la finanza. Nel nostro settore, questa tendenza ha preso forma in un conflitto silenzioso ma costante: la contrapposizione tra consulenti e gestori attivi. Una guerra fredda che non si combatte con le armi, ma con articoli, post sui social, slide di presentazione e battute al vetriolo nei convegni di settore.

Chiunque frequenti LinkedIn, Reddit o i forum di discussione dedicati agli investimenti lo sa bene. Da una parte troviamo consulenti che denigrano la gestione attiva, accusandola di essere costosa, inefficiente e priva di trasparenza. Dall’altra, gestori che difendono con orgoglio il proprio mestiere, convinti che senza di loro i mercati sarebbero un mare piatto, privo di opportunità e dinamiche. Nel mezzo, i clienti, che raramente hanno strumenti per decifrare il dibattito e che troppo spesso si ritrovano disorientati, con una domanda che nessuno sembra voler affrontare davvero: a chi devo credere?

La realtà, come spesso accade, è molto più sfumata di come viene raccontata. Eppure la semplificazione fa comodo a tutti: al consulente che vuole differenziarsi, al gestore che vuole difendere il proprio modello, al marketing che vive di slogan. Ma questa logica binaria è pericolosa, perché sposta l’attenzione dal vero obiettivo: la serenità finanziaria del cliente. Approfondiamo.

The myth of methodological purity

In recent years, especially in the world of independent consulting, a certain cult of «methodological purity» has emerged. Passive is good, active is bad. ETFs equal transparency, active funds equal traps. It's a narrative that works well on social media, where simplicity of the message always wins out over the complexity of reality. Many consultants have ridden this wave, building their professional identity on fierce criticism of active managers. The narrative is simple: «I’m on the client's side, I don't charge you unnecessary costs, I don't delude you with promises of outperformance will never materialize». It is a position has its commercial strength, especially in a context where cost sensitivity has grown and where data seem to confirm the difficulty of active managers in beating benchmarks.

Yet behind this façade often lies a paradox. The same advisors who condemn active management end up adopting manager-like behavior in their clients' portfolios. Improvised stock picking, market timing based on macroeconomic feelings, tactical shifts in asset classes depending on the cycle, frequent and often unjustified rebalancing (just for the sake of movement?). In other words, exactly what active managers are criticized for. The real difference lies not in formal transparency, but in the nature of the approach. Active managers operate with a specific mandate: to select securities, move in the market and try to generate extra returns relative to a benchmark. It is a technical job, limited in scope and judged on performance results. Advisors, on the other hand, have a broader mandate: they don’t have to «beat the market» but rather help clients structure a path consistent with their objectives, constraints, and risk tolerance. It is therefore not a question of superimposing the two figures, but of recognizing they play different and complementary roles.

Il mito della purezza metodologica

Negli ultimi anni, soprattutto nel mondo della consulenza indipendente, si è affermato un certo culto della «purezza metodologica». Passiva è bello, attiva è male. ETF uguale trasparenza, fondi attivi uguale trappola. È un racconto che funziona bene sui social, dove la semplicità del messaggio ha sempre la meglio sulla complessità della realtà. Molti consulenti hanno cavalcato questa onda, costruendo la propria identità professionale sulla critica serrata ai gestori attivi. La narrazione è semplice: «io sono dalla parte del cliente, non ti faccio pagare costi inutili, non ti illudo con promesse di sovra-performance che non arriveranno mai». È un posizionamento che ha una sua forza commerciale, soprattutto in un contesto in cui la sensibilità ai costi è cresciuta e in cui i dati sembrano confermare la difficoltà dei gestori attivi nel battere i benchmark.

Eppure, dietro questa facciata si nasconde spesso un paradosso. Gli stessi consulenti che condannano la gestione attiva finiscono per adottare, nei portafogli dei loro clienti, comportamenti da gestori. Stock picking improvvisati, market timing basati su sensazioni macroeconomiche, spostamenti tattici di asset class a seconda del ciclo, ribilanciamenti frequenti e spesso poco giustificati (solo per movimentare?). In altre parole, esattamente ciò che viene rimproverato ai gestori attivi. La vera differenza non sta nella trasparenza formale, ma nella natura stessa dell’approccio. I gestori attivi operano con un mandato preciso: selezionare titoli, muoversi sul mercato e cercare di generare extra-rendimento rispetto a un benchmark. È un lavoro tecnico, circoscritto e giudicato sul risultato di performance. I consulenti, invece, hanno un mandato più ampio: non devono «battere il mercato», ma aiutare il cliente a strutturare un percorso coerente con i suoi obiettivi, i suoi vincoli e la sua tolleranza al rischio. Non si tratta quindi di sovrapporre le due figure, ma di riconoscere che svolgono ruoli diversi e complementari.

The weight of numbers: active versus passive

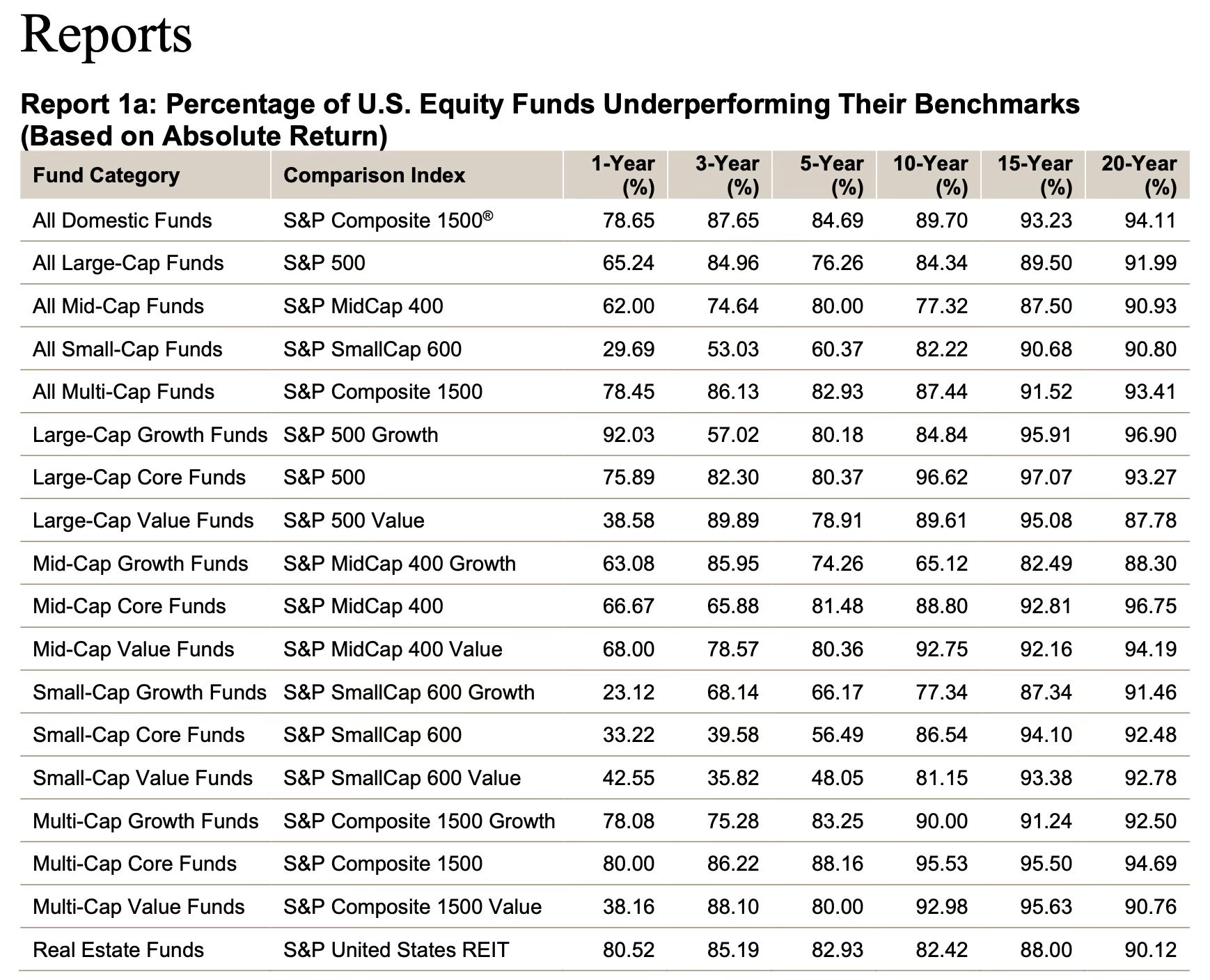

To dismantle ideologies, we need to return to the data. The debate between active and passive management is not new and has been the subject of studies, comparisons, and statistics for years. The SPIVA Report, published by S&P Dow Jones Indices, is perhaps the most authoritative source in this field. According to the latest update for Europe, 92% of active large-cap managers failed to beat their benchmark over ten years. In the United States, the percentage is not very different: approximately 88% of active large-cap blend funds were outperformed by their benchmark over the same period. These figures seem to put an end to the debate: in the long term, especially in developed and liquid markets, passive management has prevailed. Yet it would be wrong to interpret these data as a definitive condemnation, because there are exceptions.

In emerging markets, during some periods of volatility, active managers have proven they can add value, both in terms of performance and risk control. Some management companies have historically built convincing track records based on highly concentrated buy-and-hold strategies. Funds specializing in small-cap, thematic, or ESG stocks can still benefit from more pronounced inefficiencies, where active selection makes a difference. Not to mention the legendary Medallion Funds of the late but never forgotten Jim Simons. The point, therefore, is not to declare the victory of one model over another, but to recognize that active management can work, provided it is truly active and not just in terms of costs.

A simple numerical example clarifies the issue. Let's imagine two portfolios: the first invested in an S&P 500 ETF with annual costs of 0.07%, the second in an active US large-cap blend fund with an average TER of 1.5%. Over a 20-year horizon, with the index yielding an average of 8.7% per annum, the passive portfolio accumulates about 30% more capital than the active one. The difference is all in the costs. But if active fund manages to consistently outperform by 2% per annum net, then final result would be reversed. The truth, therefore, lies neither in condemnation nor in exaltation. It lies in recognizing the conditions under which a model works and limits beyond which it becomes inefficient.

Il peso dei numeri: attivo contro passivo

Per smontare le ideologie serve tornare ai dati. Il dibattito tra gestione attiva e gestione passiva non è nuovo e da anni produce studi, confronti e statistiche. SPIVA Report, pubblicato da S&P Dow Jones Indices, è forse la fonte più autorevole in questo campo. Secondo l’ultimo aggiornamento relativo all’Europa, il 92% dei gestori attivi large-cap non è riuscito a battere il proprio benchmark a dieci anni. Negli Stati Uniti la percentuale non è molto diversa: circa l’88% dei fondi attivi large-cap blend è stato battuto dall’indice di riferimento nello stesso arco temporale. Questi numeri sembrano mettere la parola fine al dibattito: nel lungo periodo, soprattutto nei mercati sviluppati e liquidi, la gestione passiva ha avuto la meglio. Eppure sarebbe sbagliato leggere questi dati come una condanna definitiva, perché ci sono eccezioni.

Nei mercati emergenti, in particolari fasi di volatilità, alcuni gestori attivi hanno dimostrato di poter aggiungere valore, sia in termini di performance che di controllo del rischio. Alcune case di gestione hanno storicamente costruito track record convincenti, basati su strategie buy & hold ad alta concentrazione. Fondi specializzati in small-cap, tematici o ESG possono ancora beneficiare di inefficienze più marcate, dove la selezione attiva fa la differenza. Per non parlare del mitico Medallion Funds dello scomparso ma mai dimenticato Jim Simons. Il punto quindi non è decretare la vittoria dell’uno o dell’altro modello, ma riconoscere che la gestione attiva può funzionare, a patto che sia davvero attiva e non solo nei costi.

Un semplice esempio numerico chiarisce la questione. Immaginiamo due portafogli: il primo investito in un ETF sull’S&P500 con costi dello 0,07% annuo, il secondo in un fondo attivo USA large-cap blend con un TER medio dell’1,5%. Su un orizzonte di vent’anni, con l’indice che rende in media l’8,7% annuo, il portafoglio passivo accumula circa il 30% in più di capitale rispetto a quello attivo. La differenza è tutta nei costi. Ma se il fondo attivo riuscisse a sovra-performare stabilmente del 2% annuo netto, allora il risultato finale si ribalterebbe. La verità, dunque, non sta né nella condanna né nell’esaltazione. Sta nel riconoscere le condizioni in cui un modello funziona e i limiti oltre i quali diventa inefficiente.

Advisor and manager: two different professions

This is where central issue comes into play: the role of advisor compared to the manager. The active manager is a professional who lives under the spotlight of relative performance, has clear constraints, return objectives and a defined investable universe. Their job is to seek alpha, i.e., additional return relative to the benchmark. Advisor, on the other hand, should not be an alpha hunter. Their task is broader and more complex: to act as a director. They coordinate all components of the client's assets, investments, liquidity, pensions, taxation, insurance protection, estate planning and integrate them into a plan consistent with the person's life goals.

The value of an advisor is not measured by their ability to guess the right stock or the right moment, but by their strategic consistency, risk management and ability to stay the course even when markets are in turmoil. When an advisor masquerades as a manager, chasing the market with improvised tactical strategies, they betray their mission. Similarly, when a manager ignores the real needs of the end client, entrenching themselves in the logic of pure performance, they lose sight of the ultimate meaning of their activity. These are two distinct roles that should work together, not two opposing factions.

The problem is the dominant narrative pushes towards opposition. Advisors versus managers, active versus passive, costs versus value. It is a binary logic that benefits no one, least of all the end customer. And effects are clear. Customers find themselves confused, unable to understand who is right. Distrust of the system grows. Professionals waste precious energy defending their position instead of building value. On social media, the discussion often descends into sterile controversy: endless threads on Reddit, poisonous comments on LinkedIn, mutual irony, sometimes even personal grudges. Yet none of these grounds are conducive to building customer trust. Trust comes from consistency, clarity, and transparency. Not from a crusade against the opposing faction.

Consulente e gestore: due mestieri diversi

Qui entra in gioco il tema centrale: il ruolo del consulente rispetto a quello del gestore. Il gestore attivo è un professionista che vive sotto il faro della performance relativa, ha vincoli chiari, obiettivi di rendimento, un universo investibile definito. Il suo mestiere è cercare alpha, ossia rendimento aggiuntivo rispetto al benchmark. Il consulente, invece, non dovrebbe essere un cacciatore di alpha. Il suo compito è più ampio e più complesso: fare da regista. Coordinare tutte le componenti del patrimonio del cliente, investimenti, liquidità, previdenza, fiscalità, protezione assicurativa, pianificazione successoria e integrarle in un disegno coerente con gli obiettivi di vita della persona.

Il valore del consulente non si misura nella capacità di indovinare il titolo giusto o il momento giusto, ma nella coerenza strategica, nella gestione del rischio, nella capacità di mantenere la rotta anche quando i mercati sono turbolenti. Quando un consulente si traveste da gestore, rincorrendo il mercato con strategie tattiche improvvisate, tradisce la propria missione. Allo stesso modo, quando un gestore ignora le esigenze reali del cliente finale, arroccandosi nella logica della performance pura, perde il senso ultimo della sua attività. Sono due ruoli distinti, che dovrebbero collaborare. Non due fazioni contrapposte.

Il problema è che la narrativa dominante spinge verso la contrapposizione. Consulenti contro gestori, attivo contro passivo, costi contro valore. È una logica binaria che non porta benefici a nessuno, men che meno al cliente finale. E gli effetti sono evidenti. I clienti si ritrovano disorientati, incapaci di capire chi abbia ragione. La sfiducia verso il sistema cresce. I professionisti sprecano energie preziose per difendere la propria posizione invece di costruire valore. Sui social, la discussione scade spesso nella polemica sterile: thread interminabili su Reddit, commenti velenosi su LinkedIn, ironie reciproche, a volte persino rancori personali. Eppure, nessuno di questi terreni è quello su cui si costruisce la fiducia del cliente. La fiducia nasce dalla coerenza, dalla chiarezza e dalla trasparenza. Non da una crociata contro la fazione opposta.

The way out: holistic advice

The term holistic derives from the Greek holos, which means «whole, entire». Applied to financial advice, it doesn’t refer to yet another technique to add to the range of tools available, but rather a change of perspective: looking at the client as a whole, not only as an investor, but as a person with plans, fears, resources, and constraints. Holistic advice is therefore an approach that integrates finance, wealth planning, risk management, even emotional and relational dimensions, avoiding reducing the client to a portfolio to be optimized or a benchmark to be beaten.

So how can we get out of this cold war? The answer lies in holistic advice. An approach recognizes the complementary nature of roles: manager works to create efficient tools capable of intercepting market opportunities; advisor works to incorporate those tools into a broader project that meets the client's life goals. One without the other is incomplete. Without the advisor, the manager risks speaking a technical language that is incomprehensible to the client. Without the manager, the advisor risks limiting themselves to theoretical choices, without concrete tools.

Holistic advice means overcoming the obsession with pure performance and embracing an integrated vision: return, yes, but together with protection, planning, asset balance and fiscal sustainability. A good advisor doesn’t need to discredit anyone else to prove their own worth. All they need to do is demonstrate method, transparency, and intellectual honesty. This is the real cultural revolution that our industry needs: putting the client back at the center and recognizing that every player in the supply chain has a specific and valuable role to play.

The cold war between advisors and managers is fruitless. It produces no winners, only permanent tensions and a climate of mistrust. The losers, always and in any case, are clients. The real future of consulting doesn’t lie in taking sides, but in knowing how to integrate different skills into a coherent project. In a complex, fragmented and uncertain world, value doesn’t come from ideology, but from the ability to build long-term peace of mind. Because the greatest luxury we can offer a client today is not to promise stellar returns, but to give them the certainty that, whatever happens in the markets, they will always have a clear, stable, and consistent path in life.

La via d’uscita: la consulenza olistica

Il termine olistico deriva dal greco holos, che significa «tutto, intero». Applicato alla consulenza finanziaria, non indica una tecnica in più da aggiungere al ventaglio degli strumenti, ma un cambio di prospettiva: guardare al cliente nella sua interezza, non solo come investitore, ma come persona con progetti, paure, risorse e vincoli. La consulenza olistica è quindi un approccio che integra finanza, pianificazione patrimoniale, gestione del rischio e persino dimensioni emotive e relazionali, evitando di ridurre il cliente a un portafoglio da ottimizzare o a un benchmark da battere.

Quindi, come uscire allora da questa guerra fredda? La risposta appunto, sta nella consulenza olistica. Un approccio che riconosce la complementarità dei ruoli: il gestore lavora per creare strumenti efficienti, in grado di intercettare opportunità di mercato; il consulente lavora per inserire quegli strumenti in un progetto più ampio, che risponda agli obiettivi di vita del cliente. L’uno senza l’altro è monco. Il gestore senza il consulente rischia di parlare un linguaggio tecnico incomprensibile al cliente. Il consulente senza il gestore rischia di limitarsi a scelte teoriche, prive di strumenti concreti.

La consulenza olistica significa superare l’ossessione per la performance pura e abbracciare una visione integrata: rendimento, sì, ma insieme a protezione, pianificazione, equilibrio patrimoniale, sostenibilità fiscale. Un bravo consulente non ha bisogno di screditare nessuno per far emergere il proprio valore. Gli basta dimostrare metodo, trasparenza e onestà intellettuale. È questa la vera rivoluzione culturale che serve al nostro settore: riportare il cliente al centro e riconoscere che ogni attore della filiera ha un ruolo specifico e prezioso.

La guerra fredda tra consulenti e gestori è sterile. Non produce vincitori, solo tensioni permanenti e un clima di sfiducia. A perderci, sempre e comunque, sono i clienti. Il vero futuro della consulenza non sta nello schierarsi da una parte o dall’altra, ma nel saper integrare competenze diverse in un progetto coerente. In un mondo complesso, frammentato e incerto, il valore non nasce dall’ideologia, ma dalla capacità di costruire serenità nel lungo periodo. Perché il lusso più grande che possiamo offrire oggi a un cliente non è promettere rendimenti stellari, ma dargli la certezza che, qualunque cosa accada nei mercati, avrà sempre una rotta chiara, stabile e coerente con la sua vita.