Lump-Sum Investment or Dollar-Cost Averaging?

Which is really the best choice for knowledge-based investor? Let's clear things up

There is a question that every investor faces sooner or later. It is one of those questions never goes out of style, despite changes in markets, technologies, and investment platforms. It is the fundamental question about entering into an investment: is it better to invest everything at once, in a single transaction, or is it better to enter gradually, staggering purchases over time? This alternative is technically represented by two acronyms are as simple as they are meaningful: Dollar-Cost Averaging and Lump-Sum Investment. DCA is a capital accumulation plan, i.e., a path spread out over time, while Lump-Sum is a one-time investment.

At first glance, the difference may seem to be merely a matter of style. However, behind this decision lies a whole world of strategies, historical data, psychological considerations, and, above all, implications for returns. Understanding which of the two methods is most effective is not just about optimizing a financial transaction: it means understanding how the investor relates to time, risk, and their own money.

C’è una domanda che, prima o dopo, ogni investitore si trova ad affrontare. Una di quelle domande che non passano mai di moda, nonostante cambino i mercati, le tecnologie e le banche. È la questione di fondo sull'ingresso in un investimento: conviene investire tutto subito, in un’unica soluzione, oppure è meglio entrare poco alla volta, con calma, scaglionando gli acquisti nel tempo? Questa alternativa si presenta tecnicamente sotto due acronimi tanto semplici quanto carichi di significato: PAC (o Dollar-Cost Averaging) e PIC (o Lump-Sum Investment). Il PAC è un piano di accumulo del capitale, ossia un percorso diluito nel tempo mentre il PIC è l’investimento in un’unica soluzione.

A prima vista, la differenza può sembrare solo una questione di stile. E invece, dietro questa decisione, si nasconde un intero mondo di strategie, dati storici, considerazioni psicologiche, e soprattutto implicazioni sul rendimento. Capire quale dei due metodi sia il più efficace non significa solo ottimizzare un’operazione finanziaria: significa comprendere in che modo l’investitore si relaziona con il tempo, con il rischio e con il proprio denaro.

The direct approach: invest everything right away

Imagine you have $100,000 to invest. Lump-Sum Investment is the clear choice: you take all your capital and allocate it immediately to the market, in an ETF, a fund, a portfolio of securities, whatever. It's a decisive, courageous, and above all definitive move. From the next day onwards, you are completely exposed to market trends. If they rise, great: you earn immediately on the entire amount. If they fall, you are thrown directly into the storm. There is no safety net.

This method, often viewed with some apprehension by those who are more cautious, has a very solid logic behind it. In fact, statistics show that financial markets, at least global stock markets, tend to rise over time. This is not an opinion: it is a fact. Looking at decades of performance of indices such as S&P500 or MSCI World, we see, in the vast majority of periods, an investor who put all their capital in immediately performed better than those who split their investment.

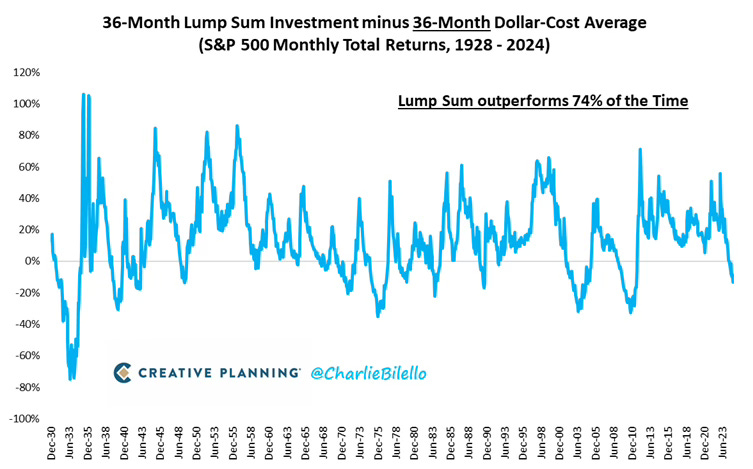

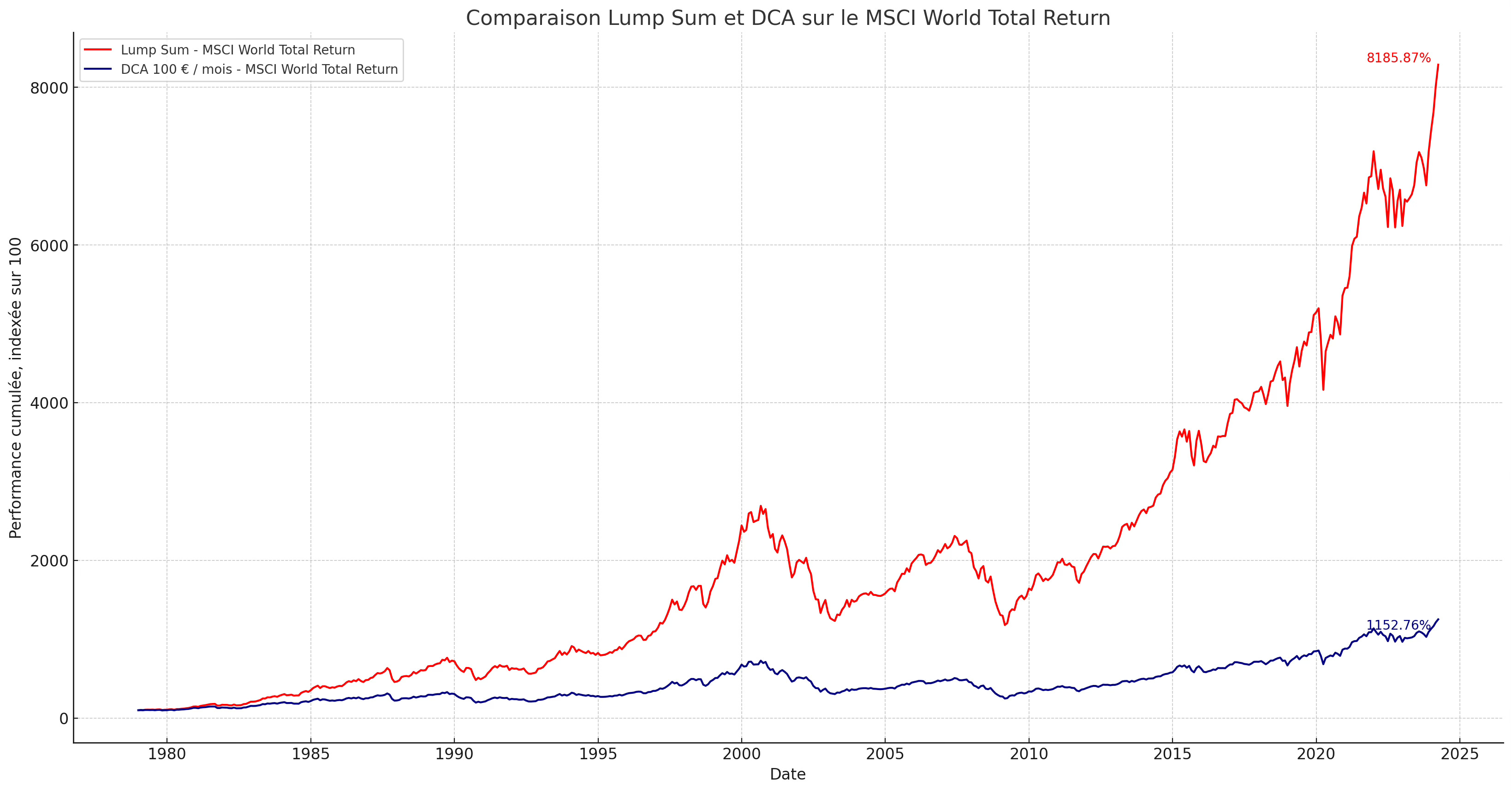

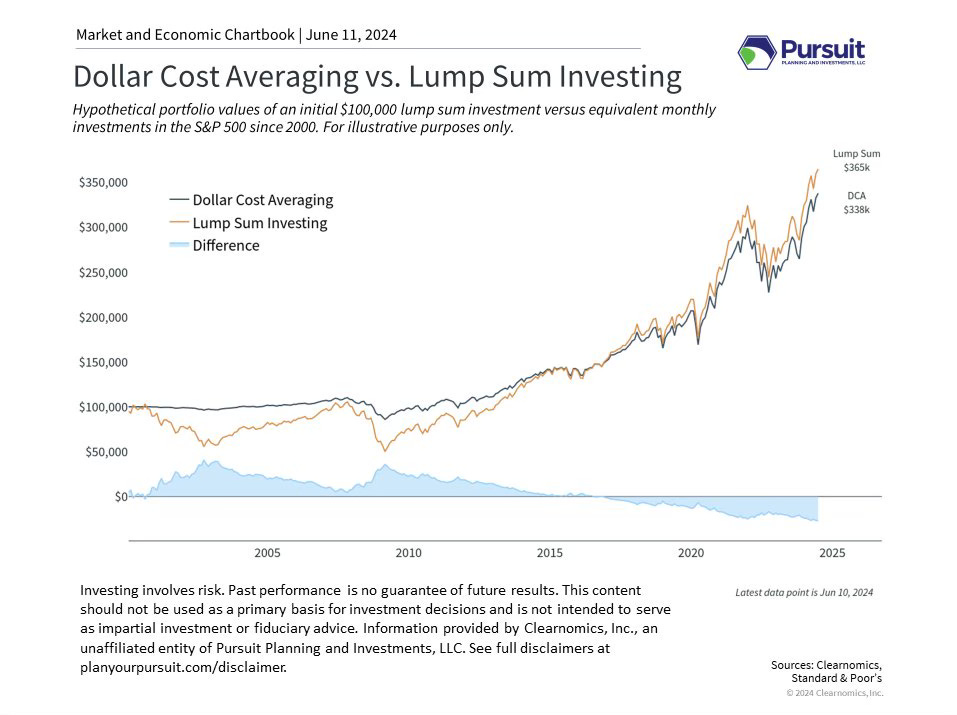

A widely cited study conducted by Vanguard analyzed hundreds of scenarios from 1926 to the present, finding that Lump-Sum Investment outperformed Dollar-Cost Averaging in about two-thirds of cases, especially over time horizons of 10 years or more. Simply put, those who had the courage (or coolness) to invest everything at once were more likely to earn more. And not just a little more: the difference can be significant, especially thanks to the advantage of compound interest, which acts immediately on the entire sum. Anyone who invested $100,000 in an ETF on the MSCI World in 2000 and left it there for twenty years would have seen their capital double today. Those who spread their investment over two years with a DCA, on the other hand, would have achieved a more modest result, without losing anything. But over time, this caution has cost them in terms of returns.

In-depth analysis Lump-Sum Investment (PIC) — It is an approach consists of investing the entire available capital in a single transaction, immediately, without dividing it into tranches over time. If, for example, an investor has $50,000 and chooses to adopt a lump sum strategy, they will invest all of it in a single transaction without waiting, staggering, diluting time risk.

The logic behind this approach is based on a historically proven fact: in the long term, financial markets tend to rise. By investing everything at once, the investor is exposed from the outset to the power of compound interest and returns of the market as a whole. The longer you remain invested with all your capital, the greater the likelihood of obtaining a good return. Several studies, including those mentioned above by Vanguard, Morningstar, and universities such as Berkeley, show that Lump-Sum have historically outperformed DCA in most of the periods analyzed (generally in 60-70% of cases over ten-year horizons, ed.). This is because the capital starts working all together and right away.

The main limitation of Lump-Sum investing is immediate exposure to market risk. If you invest all your capital just before a correction or crash, you will suffer the entire decline with your entire portfolio. From a psychological point of view, this can be devastating for an unprepared investor: initial losses can prompt the disposal of the investment, often at the worst possible moment. For this reason, even though it is statistically more effective, Lump-Sum investing requires a high tolerance for volatility, a long time horizon of at least 5-10 years, and a well-structured strategy (with good asset allocation and a long-term vision, ed.).

Lump-Sum investment is a strategy suitable for those who want to optimize long-term capital growth and have emotional and technical capacity to withstand short-term market fluctuations. It is more effective in bullish markets, but more risky from a psychological point of view. For this reason, in financial consulting, it is often recommended to experienced clients with a long-term vision and greater confidence in volatility. But as always in finance, the best strategy is the one that investor can actually follow with discipline.

L’approccio immediato: investire tutto subito

Immagina di avere 100.000€ da investire. Il PIC è la scelta netta: si prende tutto il capitale e lo si alloca immediatamente sul mercato, in un ETF, un fondo, un portafoglio di titoli, quello che sia. È una mossa decisa, coraggiosa, e soprattutto definitiva. Dal giorno dopo, si è esposti completamente all’andamento dei mercati. Se salgono, bene: si guadagna fin da subito sull’intera cifra. Se scendono, si entra direttamente nella burrasca. Non c’è rete di sicurezza.

Questo metodo, spesso visto con un certo timore da chi è più cauto, ha però una logica molto solida dietro di sé. Infatti, le statistiche dimostrano che i mercati finanziari, almeno quelli azionari globali, tendono a salire nel tempo. Non è un’opinione: è un dato di fatto. Prendendo in esame decenni di andamento di indici come l’S&P500 o l’MSCI World, si osserva che, nella stragrande maggioranza dei periodi, un investitore che ha messo tutto il capitale subito ha avuto risultati migliori rispetto a chi ha frazionato l’investimento.

Uno studio molto citato, condotto da Vanguard, ha analizzato centinaia di scenari dal 1926 ad oggi, scoprendo che il PIC ha ottenuto performance superiori al PAC in circa due terzi dei casi, soprattutto su orizzonti temporali di 10 anni o più. In parole semplici: chi ha avuto il coraggio (o la freddezza) di investire tutto subito, ha avuto più probabilità di guadagnare di più. E non solo un po’ di più: la differenza può essere significativa, soprattutto grazie al vantaggio dell’interesse composto che agisce fin da subito su tutta la somma. Chi avesse investito 100.000€ in un ETF sul MSCI World nel 2000 e avesse lasciato tutto lì per vent’anni, oggi avrebbe visto raddoppiare il proprio capitale. Chi, invece, avesse diluito l’ingresso con un PAC su due anni, avrebbe ottenuto un risultato più modesto, pur senza perdere nulla. Ma nel tempo, questa prudenza è costata rendimento.

Approfondimento PIC (Lump-Sum Investment) — E’ l’approccio che consiste nell’investire l’intero capitale disponibile in un’unica soluzione, immediatamente, senza suddividerlo in tranche nel tempo. Se, ad esempio, un investitore dispone di 50.000€ e sceglie di adottare una strategia PIC, li investirà tutti in una sola operazione senza attendere, senza scaglionare, senza diluire il rischio temporale.

La logica di questo approccio si basa su una realtà storicamente verificata: nel lungo periodo, i mercati finanziari tendono a salire. Investendo tutto subito, l’investitore si espone fin dall’inizio al potere dell’interesse composto e ai rendimenti del mercato nel suo complesso. Più tempo si resta investiti con tutto il capitale, maggiore è la probabilità di ottenere un buon ritorno. Diversi studi, tra cui quelli sopra citati di Vanguard, o Morningstar e università come Berkeley, dimostrano che il PIC ha storicamente sovra-performato il PAC nella maggioranza dei periodi analizzati (in genere nel 60-70% dei casi su orizzonti decennali, ndr). Questo perché il capitale inizia a lavorare tutto insieme e fin da subito.

Il limite principale del PIC è l’esposizione immediata al rischio di mercato. Se si investe tutto il capitale poco prima di una correzione o di un crollo, si subisce l’intera discesa con tutto il portafoglio. Dal punto di vista psicologico, questo può essere devastante per un investitore non preparato: le perdite iniziali possono spingere alla dismissione dell’investimento, spesso nel momento peggiore. Per questo motivo, anche se statisticamente più efficace, il PIC richiede una forte tolleranza alla volatilità, un orizzonte temporale lungo, di almeno 5-10 anni, e una strategia ben strutturata (con una buona asset allocation e una visione di lungo termine, ndr).

Il PIC è una strategia adatta a chi vuole ottimizzare la crescita del capitale nel lungo periodo e ha la capacità emotiva e tecnica per sopportare le oscillazioni dei mercati nel breve. È più efficace in mercati tendenzialmente rialzisti, ma più rischiosa dal punto di vista psicologico. Per questo, in consulenza finanziaria, è spesso raccomandata a clienti esperti, con visione di lungo periodo e maggiore confidenza con la volatilità. Ma come sempre in finanza, la miglior strategia è quella che l’investitore riesce davvero a seguire con disciplina.

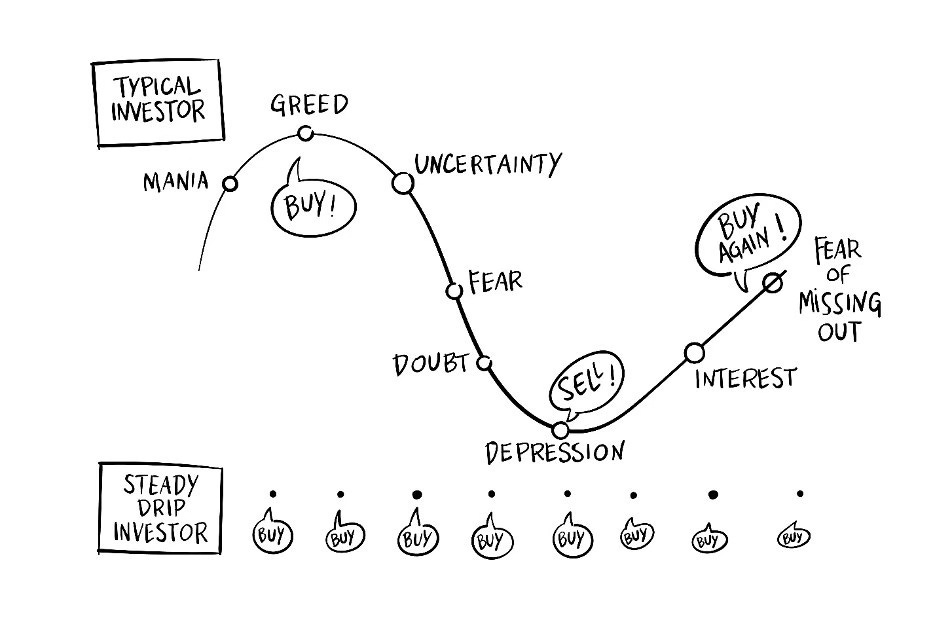

The appeal of Dollar-Cost Averaging: entering gradually

The idea of not risking everything at once is deeply rooted in the minds of those who fear investing at the wrong time. Who doesn't have this fear? Getting the timing wrong, investing today and finding yourself tomorrow in a market has fallen by 20% or 30%, can be a destabilizing experience. The DCA was created precisely to address this concern: to spread out investments so as to avoid concentrating all the risk in a single moment. With DCA, those $100,000 are transformed into a series of monthly payments, perhaps over two or three years. Each month, you enter the market a little, buying shares at different prices. When markets fall, you buy at a discount. When they rise, you get on board little by little. This price averaging effect is at the heart of DCA philosophy, which focuses more on risk protection than on maximizing gains.

But there is an interesting paradox. DCA works very well when markets fall. In those rare sideways or bearish market phases, DCA manages to protect the investor from immediate losses and, at the end of accumulation period, allows them to end up with a lower average price. However, when markets rise, as they do in most decades, DCA proves less efficient. It's like getting on a train that's accelerating: those who get on right away enjoy the whole trip; those who get on one car at a time miss part of the view.

In-depth analysis of Dollar-Cost Averaging (PAC) — It is an investment strategy consists of investing a fixed amount of money at regular intervals, regardless of the market price of the financial instrument purchased. The underlying idea is simple but powerful: by buying periodically, regardless of price, you end up buying more shares when prices are low and fewer when prices are high. This mechanism reduces the risk of entering the market at an unfavorable time (such as a short-term peak) and allows you to average the purchase price over time.

Although DCA helps manage timing risk, statistically it is not the most profitable strategy in the long run. When markets are trending upward (as historically happens with stock investments ed.), investing everything at once produces better results on average. DCA sacrifices some potential return in exchange for greater emotional control and lower initial exposure. In summary, Dollar-Cost Averaging is a method of gradually entering the market, which is particularly useful for protecting against psychological risk and short-term volatility. It is not designed to maximize profits, but to minimize the perceived risk of making the wrong choice at the outset.

Il fascino del PAC: entrare gradualmente

L’idea di non giocarsi tutto in una volta è profondamente radicata nella mente di chi teme di investire nel momento sbagliato. Chi non ha questa paura? Sbagliare il timing, investire oggi e trovarsi domani in un mercato in calo del 20% o del 30%, può essere un’esperienza destabilizzante. Il PAC nasce proprio per rispondere a questo disagio: diluire gli ingressi in modo da evitare di concentrare tutto il rischio in un singolo momento. Con il PAC, quei 100.000€ si trasformano in una serie di versamenti mensili, magari per due o tre anni o più. Ogni mese, si entra un po’ nel mercato, acquistando quote a prezzi diversi. Quando i mercati scendono, si compra a sconto, quando salgono, si sale a bordo poco alla volta. Questo effetto di media dei prezzi è il cuore della filosofia del PAC, che punta più sulla protezione dal rischio che sulla massimizzazione del guadagno.

Ma c’è un paradosso interessante. Il PAC funziona molto bene quando i mercati scendono. In quelle rare fasi di mercato laterale o ribassista, esso riesce a proteggere l’investitore da perdite immediate e consente, alla fine del periodo di accumulo, di ritrovarsi con un prezzo medio più basso. Tuttavia, se i mercati salgono, come fanno nella maggior parte dei decenni, il PAC si dimostra meno efficiente. È come salire su un treno che accelera: chi è salito subito gode di tutto il viaggio; chi sale un vagone alla volta, perde parte del panorama.

Approfondimento PAC (Dollar-Cost Averaging) — E’ una strategia di investimento che consiste nell’investire una somma fissa di denaro a intervalli regolari, indipendentemente dal prezzo di mercato dello strumento finanziario acquistato. L’idea alla base è semplice ma potente: acquistando periodicamente, a prescindere dal prezzo, si finisce per comprare più quote quando i prezzi sono bassi e meno quando i prezzi sono alti. Questo meccanismo riduce il rischio di entrare nel mercato in un momento sfavorevole (come un picco di breve termine) e consente di mediare il prezzo di acquisto nel tempo.

Anche se il PAC aiuta a gestire il rischio di timing, statisticamente non è la strategia più redditizia nel lungo periodo. Quando i mercati sono in trend crescente (come storicamente accade negli investimenti azionari, ndr), investire tutto subito produce in media risultati migliori. Il PAC rinuncia a parte del rendimento potenziale in cambio di maggiore controllo emotivo e minor esposizione iniziale. In sintesi, il PAC è un metodo per entrare progressivamente nel mercato, utile soprattutto per proteggersi dal rischio psicologico e dalla volatilità a breve termine. Non è pensato per massimizzare i profitti, ma per minimizzare il rischio percepito di fare una scelta sbagliata all’inizio.

The real factor: the investor

So far, we could conclude that Lump-Sum Investment is better than Dollar-Cost Averaging. But there is one key element cannot be overlooked: the investor. Because in reality, investing is not just a matter of using your head, but also, and often above all, your gut. Investing in Lump-Sum requires a high degree of self-control. You need the ability to withstand even significant losses in the first months or years of investment without panicking. For those who are inexperienced in the markets, or for those who are emotionally involved, seeing $100,000 reduced to $70,000 in a few weeks can be unbearable. It is precisely at times like these the average investor risks making the worst choice: exiting the market, selling at a loss, and never returning. And then damage becomes irreversible.

The DCA, on the other hand, acts as a kind of financial sedative. It makes entry smoother, reduces investment anxiety, and allows you to test the market without immediately feeling too exposed. For many, it is also a way to build a habit, a discipline. Especially for those who have not yet accumulated capital but are saving month after month, DCA is the natural solution. It is not just a method of entry: it is an educational journey.

So, which is better? The answer, as is often the case in finance, is not absolute. It depends on your personal situation, risk tolerance, knowledge of the markets, capital availability, and time horizon. But one thing is certain: the longer the time available, the more Lump-Sum tends to be statistically the winning choice. Not so much because it is smarter, but because it allows you to remain exposed to the market right from the start, and therefore to benefit from the power of compounding for longer. DCA makes sense, on the other hand, when the goal is to protect from yourself. When the real risk is not the market, but your emotions. When you fear you will not be able to withstand an initial drawdown and prefer to sacrifice a little return to give back peace of mind.

Many investors ultimately choose a middle ground: they invest a portion immediately, perhaps 50% of their capital, and spread the rest over 6 or 12 months. This hybrid strategy is often a good compromise: it allows you to be present in the market right away, but leaves room for a gradual entry, which is psychologically more manageable. However, there is one point on which there is no doubt, and it is perhaps the most important. The real mistake is not choosing between Lump-Sum or DCA. The real mistake is not choosing at all. Stay still, keeping money idle for months or years, waiting for the right moment never comes, is what really damages wealth.

In a world where inflation erodes the value of money and real interest rates are often negative, remaining liquid means losing purchasing power with each passing day. For this reason, beyond strategies and simulations, the most important advice remains the same: start investing. Whether all at once or little by little, it doesn't matter. The market rewards those who get started. And time, in the long run, beats timing.

La vera variabile: l’investitore

Fin qui, potremmo concludere che il PIC sia meglio del PAC. Ma c’è un elemento chiave che non può essere trascurato: la persona che investe. Perché nella realtà, non si investe solo con la testa, ma anche e spesso soprattutto con la pancia. L’investimento in PIC richiede un’elevata dose di autocontrollo. Serve la capacità di sopportare una perdita anche importante nei primi mesi, o anni, di investimento, senza farsi prendere dal panico. Per chi non ha esperienza sui mercati, o per chi è emotivamente coinvolto, vedere 100.000 ridursi a 70.000€ in poche settimane può essere insostenibile. È proprio in questi momenti che l’investitore medio rischia di fare la scelta peggiore: uscire dal mercato, vendere in perdita e non rientrare più. E allora sì che il danno diventa irreversibile.

Il PAC, invece, agisce come una sorta di tranquillante finanziario. Rende l’ingresso più morbido, riduce l’ansia da investimento, permette di testare il mercato senza sentirsi subito troppo esposti. Per molti è anche un modo per costruire un’abitudine, una disciplina. Soprattutto per chi non ha ancora accumulato un capitale, ma sta risparmiando mese dopo mese, il PAC rappresenta la soluzione naturale. Non è solo un metodo di ingresso: è un percorso educativo.

Quindi, cosa è meglio? La risposta, come spesso accade in finanza, non è assoluta. Dipende dalla situazione personale, dalla tolleranza al rischio, dalla conoscenza dei mercati, dalla disponibilità del capitale e dall’orizzonte temporale. Ma una cosa è certa: più lungo è il tempo a disposizione, più il PIC tende a essere statisticamente la scelta vincente. Non tanto perché sia più furbo, ma perché consente di restare esposti al mercato fin da subito, e quindi di beneficiare più a lungo del potere del compounding. Il PAC ha senso, invece, quando l’obiettivo è proteggersi da sé stessi. Quando il vero rischio non è il mercato, ma l’emotività. Quando si teme di non reggere un drawdown iniziale e si preferisce sacrificare un po’ di rendimento in cambio di maggiore serenità.

Molti investitori, alla fine, scelgono una via di mezzo: investono una parte subito, magari il 50% del capitale, e il resto lo diluiscono in 6 o 12 mesi. Questa strategia ibrida è spesso un buon compromesso: consente di essere presenti sul mercato fin da subito, ma lascia spazio a un ingresso graduale, psicologicamente più gestibile. C’è però un punto su cui non ci sono dubbi, ed è forse il più importante. Il vero errore non è scegliere PIC o PAC. Il vero errore è non scegliere affatto. Restare immobili, tenere i soldi fermi per mesi o anni, aspettando il momento giusto che non arriva mai, è ciò che danneggia davvero il patrimonio.

In un mondo in cui l’inflazione erode il valore del denaro e i tassi reali sono spesso negativi, restare liquidi equivale a perdere potere d’acquisto ogni giorno che passa. Per questo, al di là delle strategie e delle simulazioni, il consiglio più importante resta sempre lo stesso: comincia a investire. Che sia tutto in una volta o poco alla volta, non importa. Il mercato premia chi parte. E il tempo, alla lunga, batte il timing.