DAX Index Outlook 2025

As financial community delights in the upcoming (and useless) 2025 forecast, let's analyze the data by taking a closer look at numbers, performance and trends in the market

Traders & Investors,

welcome to the new year! Stock markets have picked up where they left off. Stocks representing the German DAX Index have largely risen. But there are plenty of dark sides behind this rise. Over the course of this Outlook recap we will go through all details step by step. Economically, Germany, Europe's economic powerhouse and industrial locomotive, is on the verge of collapse: energy shortages (Germany's energy problems stem from a combination of geopolitical tensions, wretched political decisions, and the ambitious green energy transition, ed.), aging workers (the country is facing a demographic time bomb: by 2035, Germany's working-age population is projected to shrink by millions, threatening industries that rely on skilled labor, ed) and a stagnant economy (Germany's strength in sectors such as automotive and manufacturing is in decline: the global shift to electric vehicles has put automotive giants in crisis, ed).

What has happened to Europe's strongest economy and what does it mean for the future of European Union? Will have plenty of opportunities throughout the year to delve into various topics, so sign up: in this way you will support our research work, have access to a first-rate specialized information stream. In this Special Outlook will discuss:

DAX index annual performance analysis

Performance analysis of the basket of 40 stocks

Weights evaluation by sector and industry

2025 technical expectations

The practical aspects, i.e., the revaluation of Index made by Deutsche Böerse updated at the end of November, has further unknowingly aggravated the situation of DAX, in terms of the forces in the field and its future potential. Having chosen the path of «outcome at any cost» will impose serious assessments for traders who still intend to trade this market. Different discussion for investors who will be relatively affected by the recent changes. But without further ado, let us begin!

Traders & Investitori,

benvenuti nel nuovo anno! I mercati azionari hanno ripreso da dove avevano lasciato. I titoli che rappresentano l’Indice tedesco DAX sono in gran parte saliti. Ma ci sono tantissimi lati oscuri dietro questo rialzo. Nel corso di questo Outlook recap analizzeremo step by step tutti i dettagli. Dal punto di vista economico la Germania, potenza economica dell’Europa e locomotiva industriale, è sull'orlo del collasso: carenza di energia (i problemi energetici della Germania derivano da una combinazione di tensioni geopolitiche, sciagurate decisioni politiche e dall'ambiziosa transizione energetica verde, ndr), invecchiamento dei lavoratori (il paese si trova di fronte a una bomba demografica a orologeria: entro il 2035, si prevede che la popolazione tedesca in età lavorativa si ridurrà di milioni di unità, minacciando le industrie che fanno affidamento sulla manodopera qualificata, ndr) e un'economia stagnante (la forza della Germania in settori come quello automobilistico e manifatturiero è in declino: il passaggio globale ai veicoli elettrici ha messo in crisi i giganti tedeschi dell'automobile, ndr).

Cosa è successo all'economia più forte d'Europa e cosa significa per il futuro dell'Unione Europea? Avremo tantissime opportunità durante l’anno per approfondire i vari temi, pertanto iscrivetevi: in questo modo sosterrete il nostro lavoro di ricerca, avrete accesso ad un flusso informativo specializzato di prima qualità. In questo Outlook speciale parleremo di:

Analisi performance annuale indice DAX

Analisi performance del paniere dei 40 titoli

Valutazione dei pesi per settori ed industria

Aspettative tecniche del 2025

Gli aspetti pratici, ovvero la rivalutazione dell’Indice fatta da Deutsche Böerse aggiornata alla fine di Novembre, ha ulteriormente aggravato inconsapevolmente la situazione del DAX, in termini di forze in campo e di potenzialità future. Aver scelto la strada del «risultato ad ogni costo» imporrà serie valutazioni per i traders che intenderanno ancora operare su questo mercato. Discorso diverso per gli investitori che verranno intaccati relativamente dalle recenti modifiche. Ma senza ulteriori indugi, cominciamo!

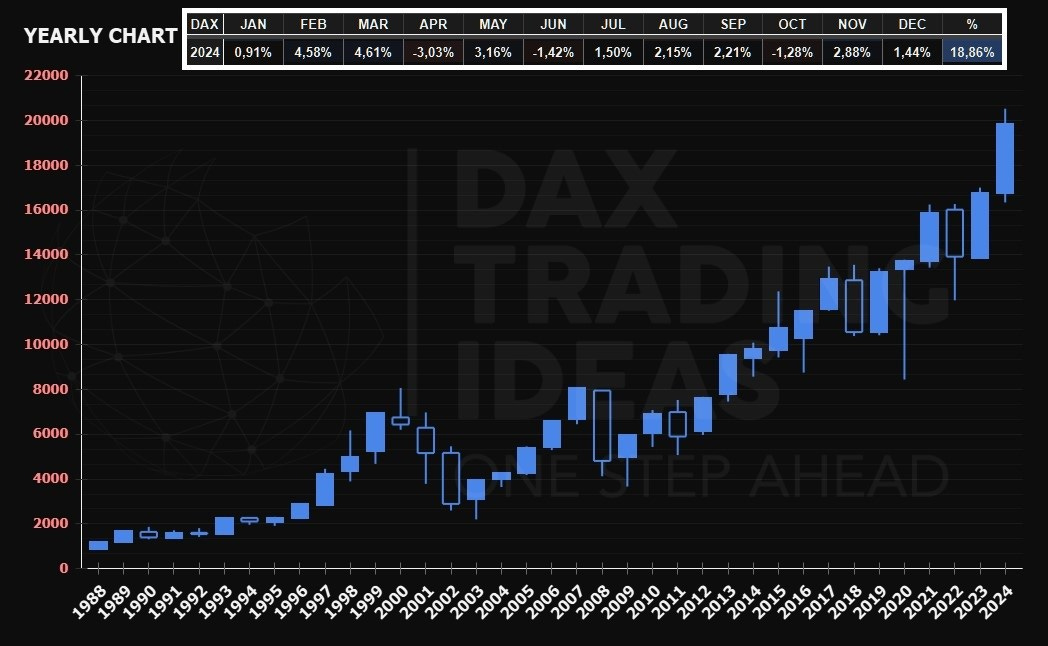

DAX Index annual performance analysis

No two without three! All analysts agree 2025 will still be a year with a green sign. While Wall Street is reveling in the forecasts of well-known hedge fund managers on the S&P500, in Europe don’t know exactly what to expect. Or rather, sentiment on the streets is strongly negative, but financial markets don't seem to want to hear it. Asset managers are hoarding money among investors' savings: race for the stock to buy, crypto-currency to own, active fund recommended by financial advisor or the latest ETF with «to the moon» performance. The honeymoon has lasted continuously for 24 months seems to be continuing, and nothing is on the horizon. But analyzing the data, something doesn't add up.

The DAX Index ended 2024 with a performance of +18.86%. This double-digit performance follows 2023, which was an even more bullish year with a +20.33% result. Seasonality was only partly respected, such was the FOMO (Fear Of Missing Out, ed.) flowing through the streets. Three negative and nine positive months enabled such results. Although much of the performance was done in the first six months of the year, January tends to be very significant in understanding what might happen in the near future.

March, June, September, and December are usually «window dressing» months: that is, industry players prepare their accounts to feed to clients. These results must contain lavish commissions and prospectuses will be used to prepare for the next quarters' collections. January, on the other hand, tends to be a period where waits for the best time to enter. Only one small detail is missing: no one can know what this best time will be. Therefore, Q1 and particularly the first part of the year is for profit taking. Should we experience a positive performance right away, it is very likely that expectation and «rush to buy» may continue throughout the year. The reason is quickly stated: big players are still out of the market, volumes are lower on average, and daily volatility (trading range, ed.) is very high. The only thing breaching investors' heads are round numbers: 20,000 for example on the DAX Index is a very important benchmark and will be throughout 2025. Check the volumes and a tick chart on Monday, January 6, 2025, and everything will be clearer to you.

Analisi performance annuale indice DAX

Non c’è due senza tre! Tutti gli analisti sono concordi nel ritenere che il 2025 sarà ancora un anno con il segno verde. Mentre Wall Street si diletta a raccogliere le previsioni dei noti hedge fund manager sull’S&P500, in Europa non si sa esattamente cosa aspettarsi. O meglio, il sentiment per le strade è fortemente negativo ma i mercati finanziari pare non vogliano sentirlo. Gli asset manager stanno facendo incetta di denaro tra i risparmi degli investitori: la corsa al titolo da comprare, la crypto-valuta da possedere, il fondo attivo consigliato dal consulente finanziario di famiglia o l’ultimo ETF con performance «to the moon». La luna di miele che dura ininterrottamente da 24 mesi sembra continuare e nulla si vede all’orizzonte. Ma analizzando i dati qualcosa non torna.

L’Indice DAX ha chiuso il 2024 con una performance del +18,86%. Tale performance a doppia cifra segue il 2023, ovvero un anno ancora più rialzista con un risultato del +20,33%. La stagionalità è stata solo in parte rispettata, tanta era la FOMO (Fear Of Missing Out, ndr) che scorreva per le strade. Tre mesi negativi e nove positivi hanno permesso tali risultati. Sebbene gran parte della performance è stata fatta nei primi sei mesi dell’anno, Gennaio è tendenzialmente molto significativo per capire cosa potrebbe accadere nel futuro prossimo.

Marzo, Giugno, Settembre e Dicembre sono solitamente mesi di «Window Dressing»: ovvero gli operatori del settore preparano i loro conti da dare in pasto ai clienti. Tali risultati devono contenere laute provvigioni e prospetti che serviranno a preparare le raccolte dei trimestri successivi. Gennaio invece, è un periodo dove si aspetta il miglior momento per entrare. Manca soltanto un piccolo dettaglio: nessuno può sapere quale sarà questo momento migliore. Pertanto il primo trimestre e in particolare la prima parte dell’anno è destinata alle prese di profitto. Qualora dovessimo registrare una performance positiva fin da subito, è molto probabile che questa aspettativa e «corsa all’acquisto» possa continuare per tutto l’anno. Il motivo è presto detto: i big players sono ancora fuori dal mercato, i volumi sono mediamente più bassi e la volatilità giornaliera (trading range, ndr) è molto alta. L’unica cosa che fa breccia nella testa degli investitori sono i numeri tondi: 20,000 ad esempio sull’Indice DAX è un riferimento molto importante e lo sarà per tutto il 2025. Controllate i volumi e un grafico a tick nella giornata di Lunedì 6 Gennaio 2025 e tutto vi sarà più chiaro.

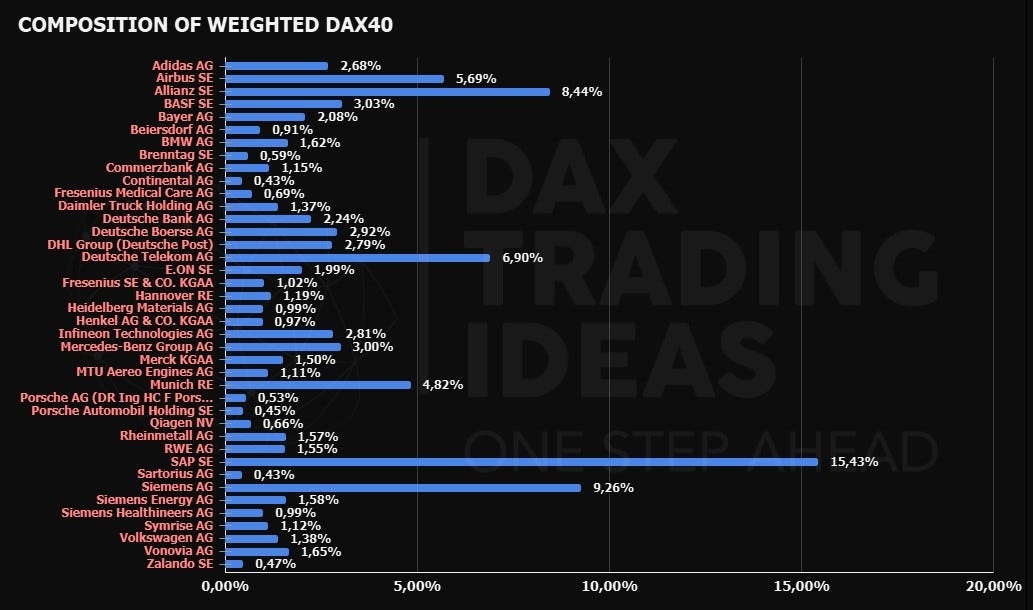

Performance analysis of the basket of 40 stocks

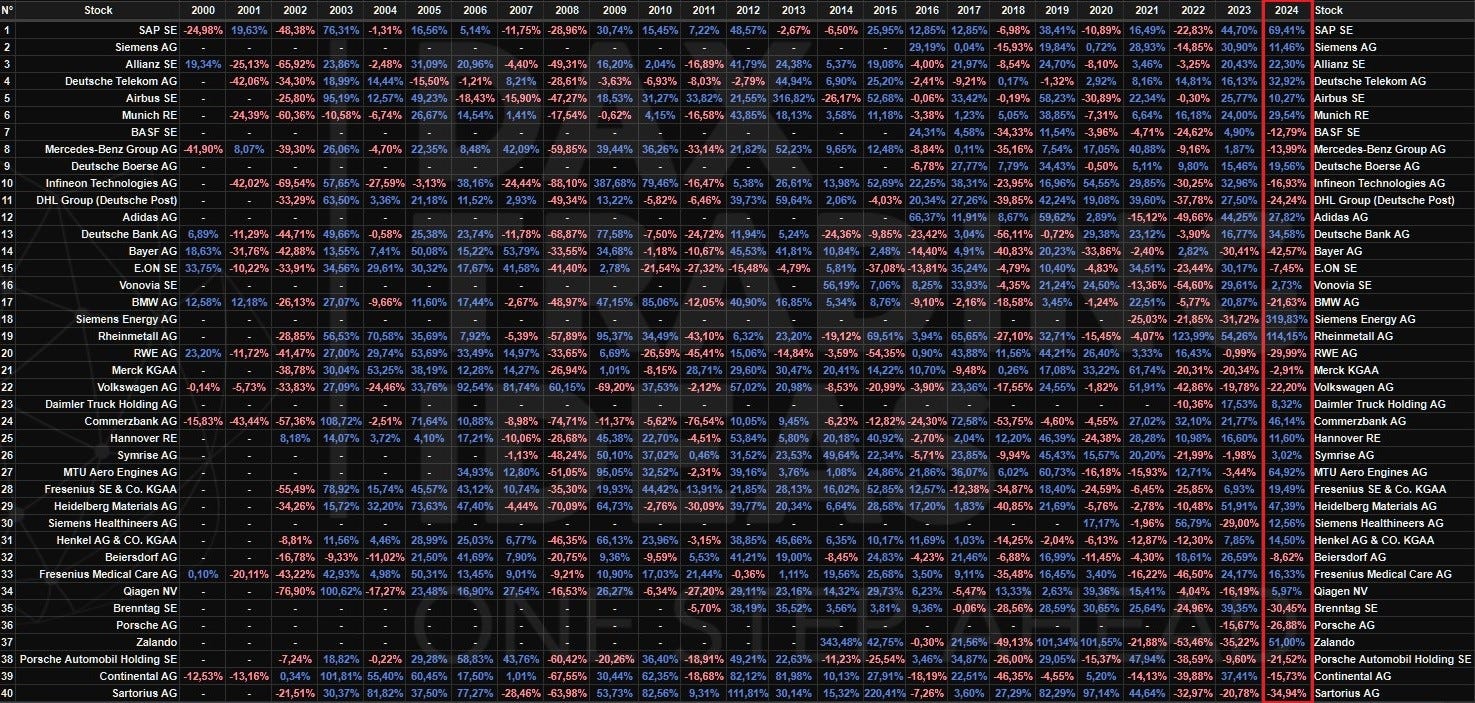

Looking at the performance of 40 stocks, that is, companies make up DAX Index, the Dow Jonesification of the German market is very evident: out with the bad apples, in with only the stocks remain with high EBITDA. Looking at the last few years, rapid exit of stocks had recently entered the basket is evident. Also evident is positive performance of the top 6 stocks (chart below is sorted by weight, ed.): SAP put up +69.41%, Siemens +11.46%, Allianz +22.30%, Deutsche Telekom +32.92%, Airbus +10.27%, and Munich +29.54%. These six stocks make up 50.54% of the entire DAX Index basket. On Wall Street they would call them «the big six» or «FAANG» made in Germany.

Although important and historical stocks such as Sartorius, Volkswagen, RWE, BMW, Bayer and others, have put up strongly negative performances ranging from -20% to -40%, in a year of expansion, of general economic growth with high interest rates, you will well understand this trend is absolutely dystopian. DAX Index is no longer meaningful to either Germany's domestic economy, Europe, or investors. Moreover, this dystopia is strongly negative for active traders, as bullish market trend has virtually cut off the entire short end of the market (short sellers, ed.), decreasing trading volume on the underlying futures. Leveraged positioning of traders means that market has become completely addicted to buying and few re-coverings of short positions: this attitude is the first cause of flash-crash, such as on August 5, 2024 (-10% in a few hours, quickly reabsorbed but wiping out most retail traders, ed.). Not a good sign in the mid-term.

Analisi performance del paniere dei 40 titoli

Osservando la performance dei 40 titoli, ovvero delle aziende che compongono l’Indice DAX, è molto evidente la Dow Jonesificazione del mercato tedesco: fuori le mele marce, dentro solo i titoli che rimangono con un EBITDA alto. Guardando gli ultimi anni è evidente la rapida uscita di titoli che recentemente erano entrati nel paniere. Altra cosa evidente è la performance positiva dei primi 6 titoli (il grafico qui sopra è ordinato per peso, ndr): SAP ha messo a segno il +69,41%, Siemens +11,46%, Allianz +22,30%, Deutsche Telekom +32,92%, Airbus +10,27% e Munich +29,54%. Questi sei titoli compongono il 50,54% dell’intero paniere dell’Indice DAX. A Wall Street le chiamerebbero «le big six» o «le FAANG» made in Germany.

Sebbene titoli importanti e storici come Sartorius, Volkswagen, RWE, BMW, Bayer e altre, abbiano messo a segno performance fortemente negative che oscillano tra il -20% e il -40%, in un anno di espansione, di crescita economica generale con tassi d’interesse alti, capirete bene che questo andamento è assolutamente distopico. L’Indice DAX non è più significativo né per l’economia interna della Germania, né per l’Europa, né per gli investitori. Inoltre, tale distopia è fortemente negativa per gli active traders, in quanto la tendenza rialzista del mercato ha praticamente tagliato fuori tutta la parte corta del mercato (venditori allo scoperto, ndr), diminuendo il volume di scambio sui sottostanti futures. Il posizionamento a leva degli operatori fa si che il mercato è diventato completamente assuefatto dagli acquisti e dalle poche ricoperture delle posizioni corte: questo atteggiamento è la prima causa dei flash-crash, come quello del 5 Agosto 2024 (-10% in poche ore, rapidamente riassorbito ma che ha spazzato via gran parte degli operatori retail, ndr). Non un bel segno nel medio periodo.

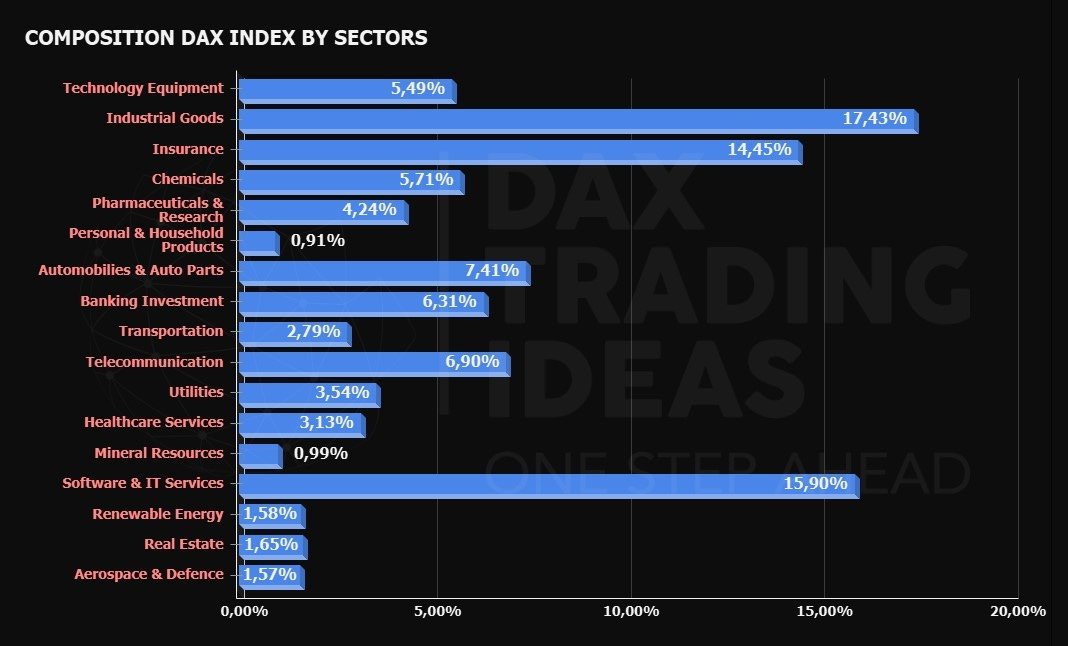

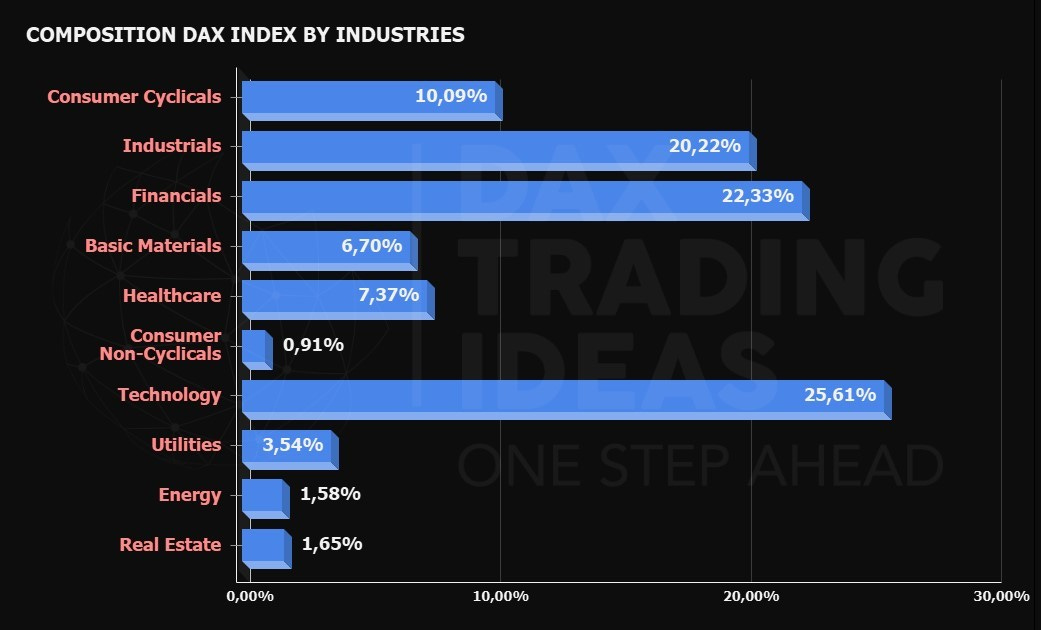

Evaluation of weights by sectors and industry

An important change was made to the industry sectors of DAX Index. By reevaluating the weights of some stocks on the upside (such as SAP going from 9% in 2023 to almost 16% in 2024, ed.) and shifting other stocks from one specific sector to another, the German Index seems to have found some balance. Shifted ever toward the technology industry will most likely dominate ‘20s, the rise from «industrial products» and «insurance» is evident. As consumption recovers and people again have a need for essential goods and products after the crisis of 2020, the insurance industry seemed to have lost its luster and interest from investors. Instead, a new frontier has emerged in the service sector: after the pandemic, interest has returned to products limit misfortunes (missed bookings, cancellations, travel flexibility, health insurance, ed.) and basket has also benefited.

2024 was also the year of consecration of the «space and defense» sector: newcomer Rheinmetall, Germany's historical war industry, which, after 2022-that is, the beginning of the war between Russia and Ukraine-found its place within the DAX Index. Although the weight is currently low (1.57%), we expect in the coming years an increase in government spending by various states in the European Union. Trump will certainly be a factor in this: before taking office he has already widely announced that those who want assistance and protection will have to pay for it, or seek domestic resources, there is no other way. The arms race is a theme heads of state have been forced to reintroduce within their own agendas: although the outgoing German government did its utmost to avoid this transition, wars on Europe's doorstep impose reflections.

Lacking the raw materials necessary for life (gas and fuels are inevitably among them, ed.), companies on the old continent are trying to reorganize themselves: technology, innovation and transformation are at the heart of the sectors that will ride major market trends in the coming years. Currently undervalued Real Estate and renewable energy, despite the very powerful hype blowing among the younger generation.

Valutazione dei pesi per settori ed industria

Un’importante cambiamento è stato apportato ai settori industriali dell’Indice DAX. Rivalutando il peso di alcuni titoli al rialzo (come ad esempio SAP passato dal 9% del 2023 a quasi il 16% del 2024, ndr) e il passaggio di altri titoli da un settore specifico all’altro, l’Indice tedesco sembra aver trovato un certo equilibrio. Spostato sempre verso l’industria tecnologica che molto probabilmente dominerà gli anni ‘20, la risalita da parte dei «prodotti industriali» e «assicurativi» è evidente. Mentre i consumi riprendono e la gente ha di nuovo necessità di beni e prodotti essenziali dopo la crisi del 2020, il settore assicurativo sembrava aver perso smalto e interesse da parte degli investitori. E’ invece nata una nuova frontiera nel settore servizi: dopo la pandemia l’interesse è tornato su prodotti che limitino le disgrazie (mancate prenotazioni, annullamenti, flessibilità nei viaggi, assicurazioni sanitarie, ndr) e anche il paniere ne ha giovato.

Il 2024 è stato anche l’anno della consacrazione del settore «spazio e difesa»: il nuovo arrivato Rheinmetall, storica industria bellica tedesca che, dopo il 2022 ovvero l’inizio della guerra tra Russia e Ucraina, ha trovato il suo posto all’interno dell’Indice DAX. Sebbene il peso sia attualmente basso (1,57%), ci aspettiamo nei prossimi anni un aumento nelle spese pubbliche dei vari stati nell’Unione Europea. Trump sarà sicuramente un fattore in tal senso: prima dell’insediamento infatti ha già ampiamente annunciato che chi vorrà assistenza e protezione dovrà pagare, oppure cercare risorse interne, non c’è altra strada. La corsa al riarmo è un tema che i capi di stato sono stati costretti a reintrodurre all’interno delle proprie agende: sebbene il governo tedesco uscente abbia fatto carte false per evitare questa transizione, le guerre alle porte dell’Europa impongono riflessioni.

Mancando di materie prime necessarie per la vita (il gas e i combustibili sono inevitabilmente tra questi, ndr), le aziende del vecchio continente stanno cercando di riorganizzarsi: tecnologia, innovazione e trasformazione sono alla base dei settori che nei prossimi anni cavalcheranno i principali trend di mercato. Attualmente sottovalutate Real Estate ed energie rinnovabili, nonostante il potentissimo hype che soffia tra le nuove generazioni.