Back to 90s

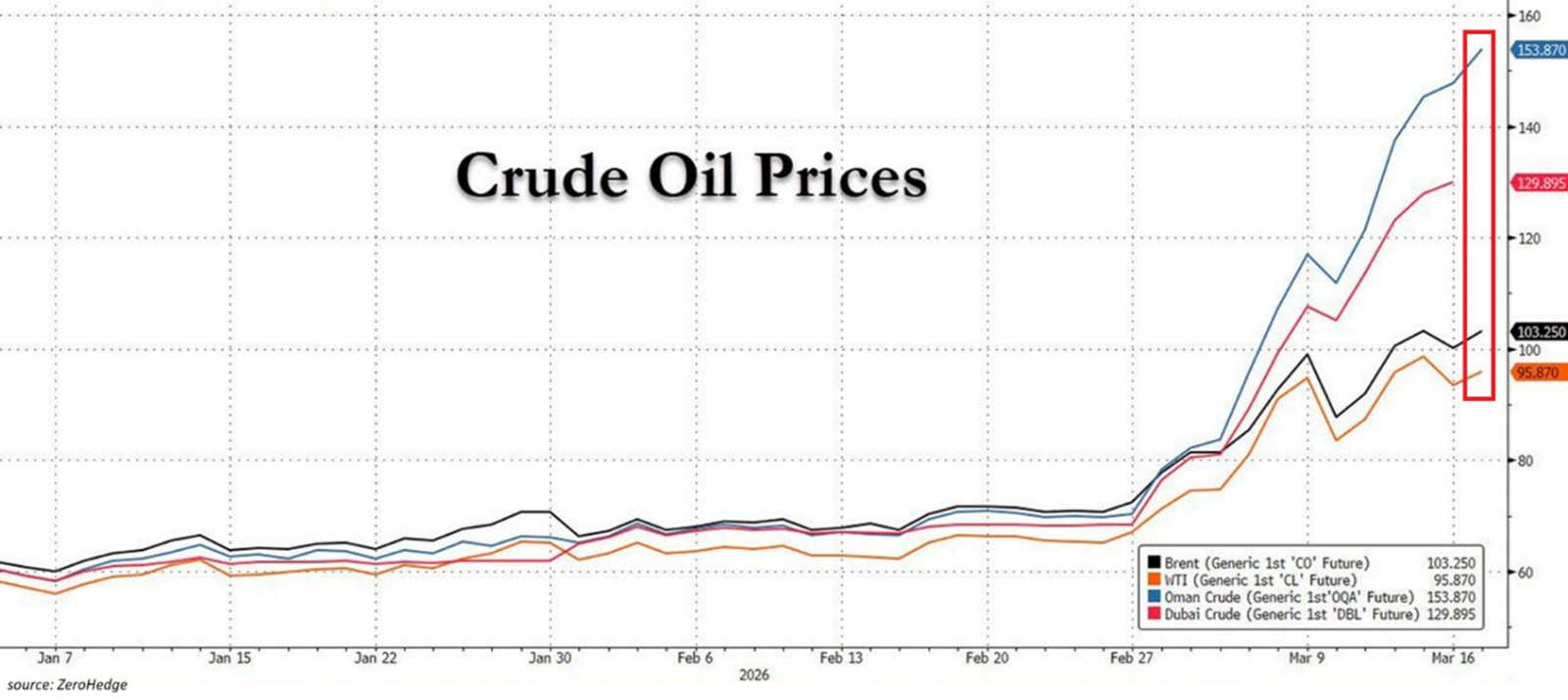

The new Gulf War served as trigger, but groundwork for a resurgence in oil prices and inflation had already been laid

In recent years, the global energy system has become more fragile, more vulnerable to shocks and less resilient than it appeared during the height of globalization. This means that when a supply risk emerges, price doesn’t merely react; it amplifies the signal. When oil prices move dramatically, they never do so in isolation: they bring with them a series of implications tend to unfold over time and market initially struggles to fully price in. It is not necessary for supply to be actually disrupted; it is enough for it to become uncertain. It is a dynamic has been seen many times throughout history and tends to repeat itself in the same way.

Il sistema energetico globale negli ultimi anni è diventato più fragile, più esposto a shock, meno ridondante di quanto apparisse nel periodo della globalizzazione piena. Questo significa che quando emerge un rischio sull’offerta, il prezzo non si limita a reagire, ma amplifica il segnale. E quando il petrolio si muove in modo così violento non lo fa mai in isolamento: si porta dietro una serie di implicazioni che tendono a svilupparsi nel tempo e che il mercato inizialmente fatica a prezzare nella loro interezza. Non serve che l’offerta venga realmente interrotta, è sufficiente che diventi incerta. È una dinamica che si è vista più volte nella storia e che tende a ripetersi sempre con le stesse modalità.

A look back at the past

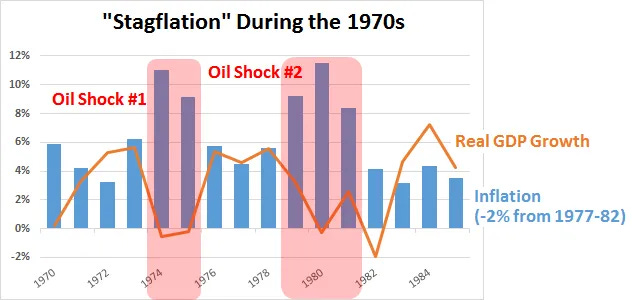

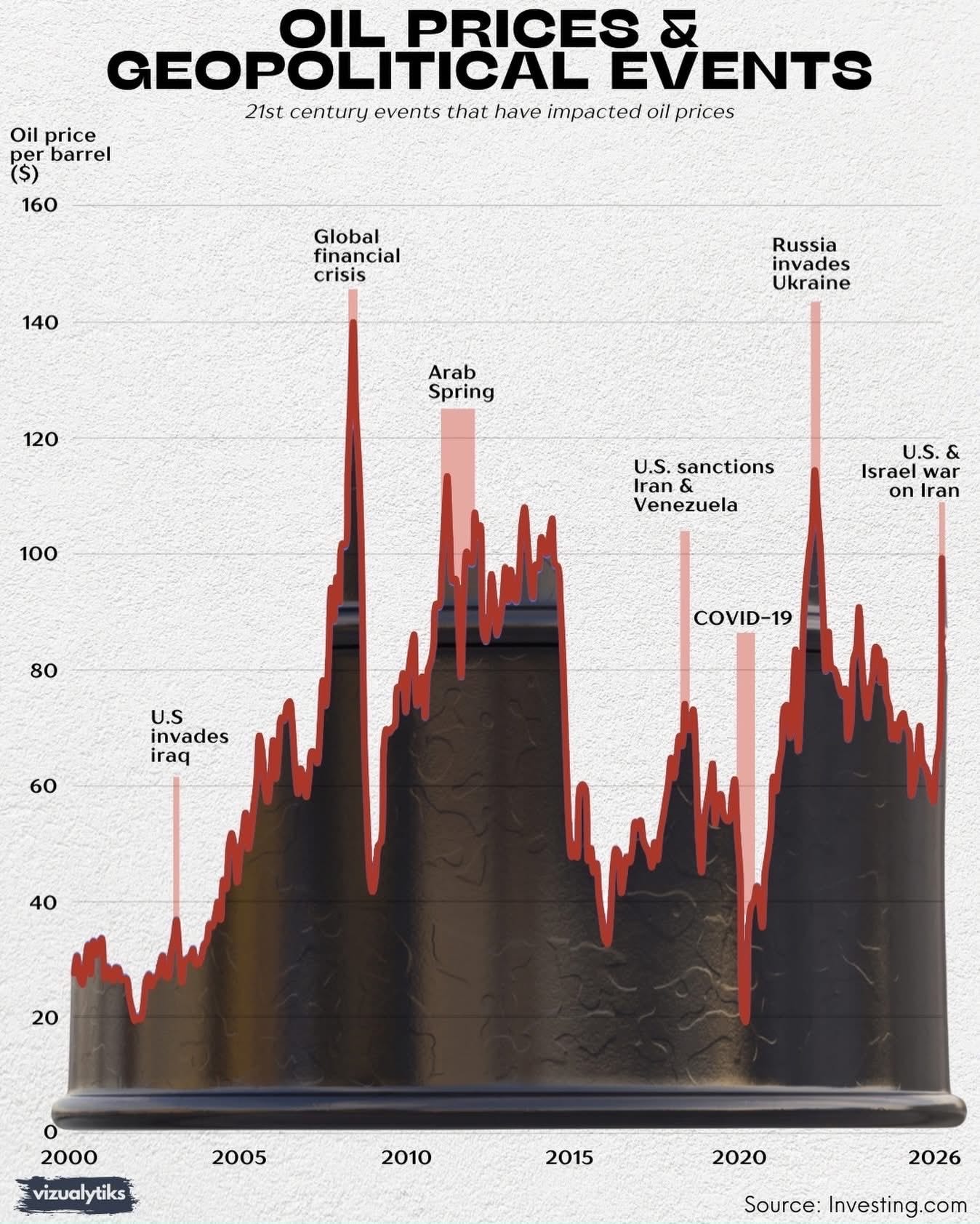

In the 1970s, the Western world learned what it means to face an externally imposed energy constraint. The OPEC embargo was not merely a political event; it was a shock that changed the way inflation was generated and perceived. Prices rose because energy suddenly became more expensive and scarcer, from there the effect spread throughout the entire economic system. Central banks were unprepared to manage that kind of inflation, because it didn’t stem from domestic excesses but from an external constraint, and response came too late, with all the consequences entailed.

In the 1990s, dynamics were less extreme but mechanism remained the same. The first Gulf War caused oil prices to double in a matter of months and the effect on inflation was immediate. It wasn’t a systemic crisis, but it was enough to tighten financial conditions and complicate the economic cycle at an already fragile stage. Even then, market initially underestimated the impact, convinced it was a temporary event, only to have to revise its expectations as shock spread to the real economy.

In the 2000s, during the subprime mortgage crisis, oil prices reached even higher levels, but in that case the demand component played a more significant role, driven by global growth and expansion of emerging markets. However, even then, rising energy prices helped push inflation upward just as the system began to show signs of strain. The Federal Reserve found itself managing a complex balancing act, and timing of its decisions was shaped precisely by this tension between growth and inflation.

The year 2020 deserves a separate mention, as it represents almost the opposite of all these dynamics. During the pandemic crisis, oil prices didn’t rise but plummeted, at times even falling into negative territory on the WTI, due to a simultaneous shock of falling demand and excess supply. In that case, energy acted as a deflationary force, helping to suppress prices and allowing central banks to intervene extremely aggressively without worrying about inflation.

Ritorno al passato

Negli anni settanta il mondo occidentale ha imparato cosa significa avere un vincolo energetico imposto dall’esterno. L’embargo dell’OPEC non fu solo un evento politico, fu uno shock che cambiò il modo in cui l’inflazione veniva generata e percepita. I prezzi salirono perché l’energia diventò improvvisamente più costosa e più scarsa, e da lì l’effetto si propagò a tutto il sistema economico. Le banche centrali non erano preparate a gestire un’inflazione di quel tipo, perché non nasceva da eccessi interni ma da una restrizione esterna, e la risposta arrivò in ritardo con tutte le conseguenze del caso.

Negli anni novanta la dinamica fu meno estrema ma il meccanismo rimase lo stesso. La prima Guerra del Golfo portò il petrolio a raddoppiare in pochi mesi e l’effetto sull’inflazione fu immediato. Non si trattò di una crisi sistemica, ma fu sufficiente per irrigidire le condizioni finanziarie e complicare il ciclo economico in una fase già fragile. Il mercato anche allora inizialmente sottovalutò l’impatto, convinto che si trattasse di un evento temporaneo, salvo poi dover rivedere le aspettative man mano che lo shock si trasmetteva all’economia reale.

Negli anni duemila durante la crisi dei mutui subprime, il petrolio raggiunse livelli ancora più elevati, ma lì la componente di domanda giocava un ruolo più importante, trainata dalla crescita globale e dall’espansione dei mercati emergenti. Tuttavia anche in quel caso l’aumento dei prezzi energetici contribuì a spingere l’inflazione verso l’alto proprio mentre il sistema iniziava a mostrare segni di cedimento. La Federal Reserve si trovò a gestire un equilibrio complesso, e il tempismo delle sue decisioni fu condizionato proprio da questa tensione tra crescita e inflazione.

Una parentesi a parte merita il 2020, perché rappresenta quasi l’opposto di tutte queste dinamiche. Durante la crisi pandemica il petrolio non è salito ma è crollato, arrivando in alcuni momenti persino in territorio negativo sul WTI, a causa di uno shock simultaneo di domanda e di eccesso di offerta. In quel caso l’energia ha agito come forza deflattiva, contribuendo a comprimere i prezzi e permettendo alle banche centrali di intervenire in modo estremamente aggressivo senza preoccuparsi dell’inflazione.

Old Ghosts

If we put the episodes described above together, a fairly clear pattern emerges: when oil prices rise significantly, inflation ceases to be a purely domestic phenomenon and once again becomes driven by external factors. This completely changes the nature of inflation itself. It is no longer something can be managed solely through domestic demand or the cost of money, but becomes the result of a constraint acting upstream of the economic system.

This is exactly what we are beginning to see today. The shift from $50 to $100 per barrel of oil is not just a matter of price; it is a signal that market is reintroducing a premium for energy risk had been progressively compressed in recent years. For a long time, it was taken for granted that energy was available, accessible, and relatively stable. This allowed for the construction of an entire macroeconomic framework based on low inflation, low interest rates and a certain predictability in economic dynamics. When this assumption breaks down, even just partially, everything else begins to shift.

Inflation is the first point of transmission. Energy permeates everything, not just direct consumption but the entire cost structure of businesses. Initially, companies try to absorb the increase by squeezing margins, but this process has its limits. When prices remain high, or continue to rise, pressure shifts to final prices. It is a gradual but persistent mechanism, and above all, it is difficult to reverse quickly because once prices are adjusted, they rarely come back down at the same speed.

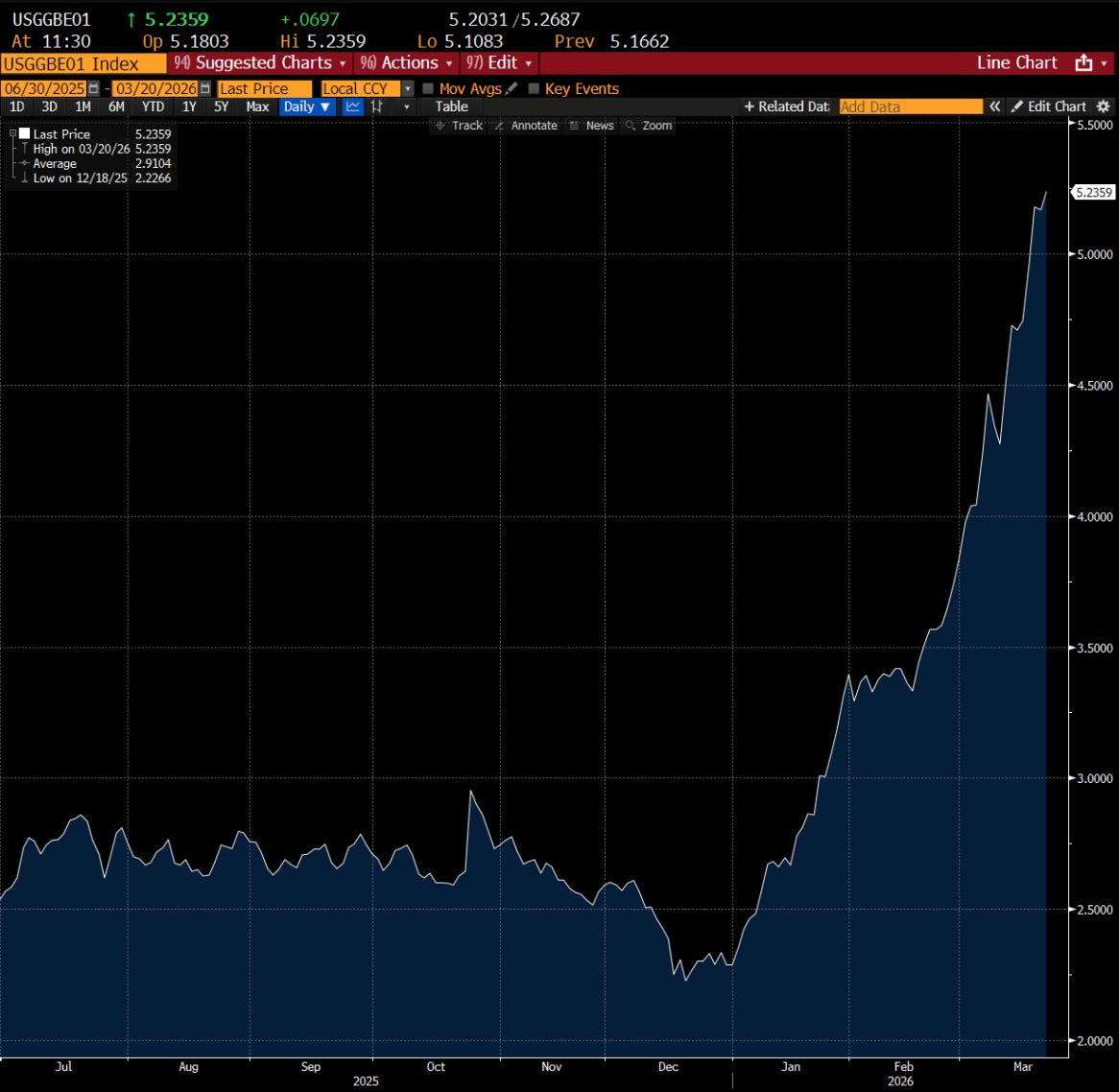

Over the past two years, the idea had taken hold that inflation was a problem on the verge of being resolved, something would follow a fairly steady downward trajectory. However, this scenario assumed the most volatile components, particularly energy, would remain under control. With oil prices doubling in just a few months, this assumption is losing ground. Even if inflation doesn’t spike immediately, its underlying dynamics are changing. It becomes less predictable, more sensitive to shocks, and more difficult to bring back to target levels in a stable manner.

Vecchi fantasmi

Se si mettono insieme gli episodi sopra descritti, emerge una costante abbastanza chiara: quando il petrolio accelera in modo significativo, l’inflazione smette di essere un fenomeno puramente domestico e torna a essere guidata da fattori esterni. Questo cambia completamente la qualità dell’inflazione stessa. Non è più qualcosa che può essere gestito solo attraverso la domanda interna o il costo del denaro, ma diventa il risultato di un vincolo che agisce a monte del sistema economico.

È esattamente quello che si sta iniziando a vedere oggi. Il movimento da 50 a 100 dollari del petrolio non è solo una questione di prezzo, è il segnale che il mercato sta reintroducendo un premio per il rischio energetico che negli ultimi anni era stato progressivamente compresso. Per molto tempo si è dato per scontato che l’energia fosse disponibile, accessibile, relativamente stabile. Questo ha permesso di costruire un intero impianto macro basato su inflazione bassa, tassi contenuti e una certa prevedibilità delle dinamiche economiche. Quando questa assunzione viene meno, anche solo in parte, tutto il resto inizia a muoversi.

L’inflazione è il primo punto di trasmissione. L’energia entra ovunque, non solo nei consumi diretti ma in tutta la struttura dei costi delle imprese. In una prima fase le aziende cercano di assorbire l’aumento comprimendo i margini, ma questo processo ha un limite. Quando il prezzo resta elevato, o continua a salire, la pressione si trasferisce sui prezzi finali. È un meccanismo graduale ma persistente, e soprattutto è difficile da invertire rapidamente perché una volta che i prezzi vengono adeguati difficilmente tornano indietro con la stessa velocità.

Negli ultimi due anni si era creata l’idea che l’inflazione fosse un problema in via di risoluzione, qualcosa che avrebbe seguito una traiettoria discendente abbastanza regolare. Questo scenario presupponeva però che le componenti più instabili, in particolare l’energia, rimanessero sotto controllo. Con il petrolio che raddoppia in pochi mesi questa ipotesi perde consistenza. Anche se l’inflazione non esplode immediatamente, cambia la sua dinamica di fondo. Diventa meno prevedibile, più sensibile agli shock, più difficile da riportare su livelli target in modo stabile.

The domino effect on Central Banks

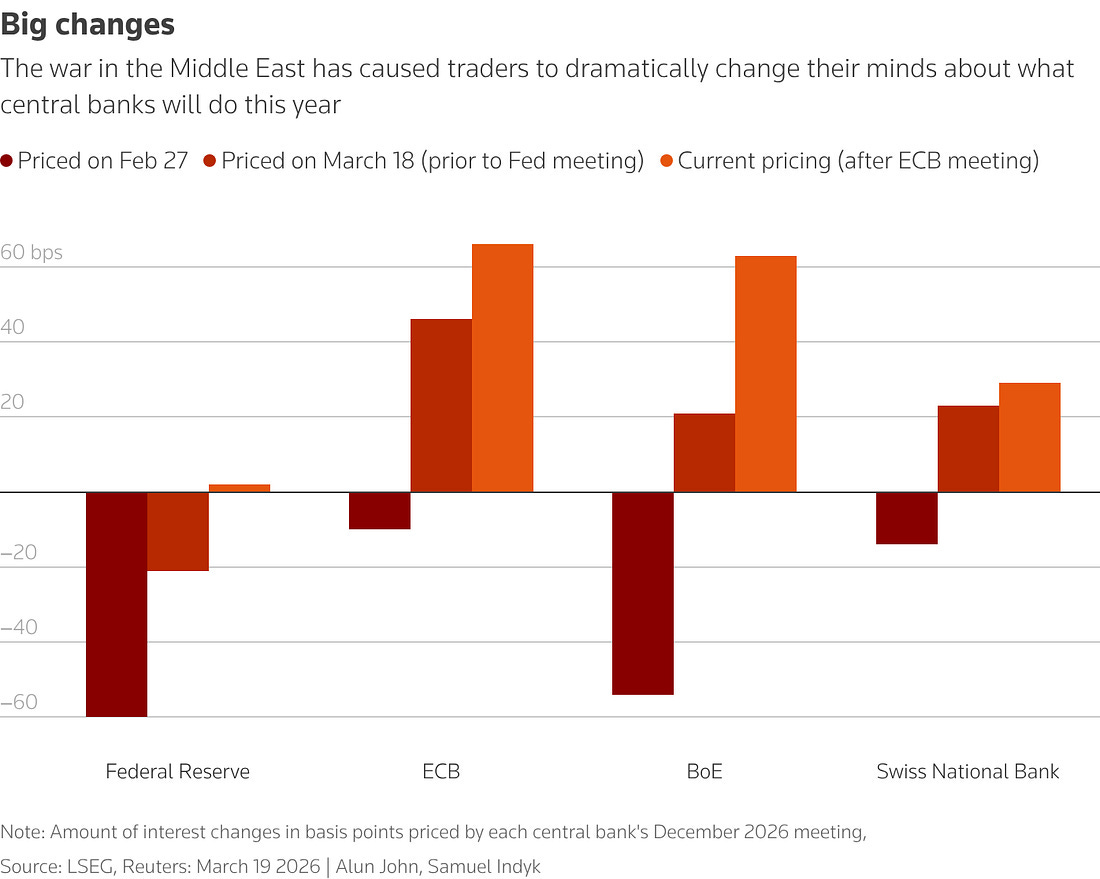

This is where central banks come into play, and this is where things really get complicated. In the United States, Federal Reserve finds itself in a position that, in some ways, resembles situations seen in the past. On the first hand, there is an economy beginning to slow under the weight of already high interest rates; on the other, there is the risk that inflation will stop falling or even rise again due to energy costs. In such a situation, monetary policy loses much of its effectiveness. Raising rates doesn’t solve the root of problem, but lowering them too soon risks legitimizing a higher level of inflation.

Historically, in these phases, Fed tends to move with great caution, often maintaining a restrictive stance longer than expected. Not necessarily to directly fight the energy shock, but to prevent it from turning into a rise in inflation expectations. It is a subtle but fundamental difference, because expectations are what can make a shock temporary or turn it into something persistent.

In Europe, the situation is different. Eurozone doesn’t have the same energy independence as United States, and this means every rise in oil prices is reflected more directly in the real economy. The European Central Bank therefore finds itself managing inflation that may be fueled by external factors while growth remains weak. It is a combination drastically reduces room for maneuver, because every choice has a clear cost. Cutting rates too soon risks reigniting price pressures; keeping them high for too long risks further squeezing an already fragile economy.

L’effetto domino sulle Banche Centrali

A questo punto entrano in gioco le banche centrali, ed è qui che il quadro si complica davvero. Negli Stati Uniti la Federal Reserve si trova in una posizione che ricorda, per certi versi, momenti già visti in passato. Da un lato c’è un’economia che inizia a rallentare sotto il peso di tassi già elevati, dall’altro c’è il rischio che l’inflazione smetta di scendere o addirittura risalga a causa dell’energia. In una situazione del genere la politica monetaria perde gran parte della sua efficacia. Alzare i tassi non risolve il problema alla radice, ma abbassarli troppo presto rischia di legittimare un livello di inflazione più alto.

Storicamente, in queste fasi, la Fed tende a muoversi con grande cautela, spesso mantenendo una postura restrittiva più a lungo del previsto. Non necessariamente per combattere direttamente lo shock energetico, ma per evitare che questo si trasformi in un aumento delle aspettative di inflazione. È una differenza sottile ma fondamentale, perché le aspettative sono ciò che può rendere temporaneo uno shock oppure trasformarlo in qualcosa di persistente.

In Europa il discorso è ancora più delicato. L’Eurozona non ha la stessa autonomia energetica degli Stati Uniti e questo significa che ogni aumento del petrolio si riflette in modo più diretto sull’economia reale. La Banca Centrale Europea si trova quindi a gestire un’inflazione che può essere alimentata da fattori esterni mentre la crescita resta debole. È una combinazione che riduce drasticamente lo spazio di manovra, perché qualsiasi scelta ha un costo evidente. Tagliare i tassi troppo presto rischia di riaccendere le pressioni sui prezzi, mantenerli alti troppo a lungo rischia di comprimere ulteriormente un’economia già fragile.

Instability & volatility: deadly combination or a temporary problem?

This tension is typical of periods when inflation is driven by energy prices. It is not a new situation, but the market had ceased to view as central. Over the past fifteen years, a certain confidence has developed in central banks’ ability to control the economic cycle, intervene in a timely manner and stabilize inflationary trends. Today, this confidence is being put to the test, because the shock stems from a variable that cannot be controlled using traditional tools.

The result is a more unstable system, not necessarily in crisis, but certainly less linear. Interest rate expectations become more volatile, inflation forecasts more scattered and markets more sensitive to every geopolitical development. It is a change is occurring gradually but tends to solidify over time. Looking back, every phase of a sharp rise in oil prices has produced effects that extended well beyond the initial moment. Extreme scenarios didn’t always materialize, but these were rarely isolated incidents. Energy prices have always had the capacity to profoundly influence the economic cycle, because they act as a base cost for the entire system.

Today we are in a phase where this mechanism is reactivating. It is not yet clear how far it will develop, but it is already evident that the context has changed. The greatest risk is to continue thinking as if nothing has changed, expecting a rapid return to an equilibrium likely no longer exists in the same form.

Frankly, I think that, despite all this uncertainty, we’ll end the year above opening levels, even if this won’t meet investors’ expectations of double-digit returns. While it is true returns are eroding, it is equally true that conditions for those entering the market today are more attractive, thanks in part to a correction in multiples had long been difficult to sustain. Despite this, market is steadily adapting to a context in which energy is once again becoming a central variable. And when that happens, everything else ceases to be as stable as before. It’s best to get used to it, quickly.

Instabilità e volatilità: mix letale o problema passeggero?

Questa tensione è tipica delle fasi in cui l’inflazione è guidata dall’energia. Non è una situazione nuova, ma è una situazione che il mercato aveva smesso di considerare come centrale. Negli ultimi quindici anni si è sviluppata una certa fiducia nella capacità delle banche centrali di controllare il ciclo economico, di intervenire in modo tempestivo e di stabilizzare le dinamiche inflattive. Oggi questa fiducia viene messa alla prova, perché lo shock arriva da una variabile che non può essere controllata con gli strumenti tradizionali.

Il risultato è un sistema più instabile, non necessariamente in crisi, ma sicuramente meno lineare. Le aspettative sui tassi diventano più volatili, le previsioni sull’inflazione più disperse, i mercati più sensibili a ogni sviluppo geopolitico. È un cambiamento che avviene gradualmente, ma che tende a consolidarsi nel tempo. Se si guarda al passato, ogni fase di forte rialzo del petrolio ha prodotto effetti che si sono estesi ben oltre il momento iniziale. Non sempre si è arrivati a scenari estremi, ma raramente si è trattato di episodi isolati. Il prezzo dell’energia ha sempre avuto la capacità di influenzare il ciclo economico in modo profondo, proprio perché agisce come un costo di base per l’intero sistema.

Oggi siamo in una fase in cui questo meccanismo si sta riattivando. Non è ancora chiaro fino a che punto si svilupperà, ma è già evidente che il contesto è cambiato. Il rischio più grande è continuare a ragionare come se nulla fosse cambiato, aspettandosi un ritorno rapido a un equilibrio che probabilmente non esiste più nelle stesse forme.

Francamente penso che, nonostante tutta questa incertezza, alla fine dell’anno ci ritroveremo sopra i livelli di apertura, anche se questo non soddisferà le aspettative di performance a doppia cifra degli investitori. Se è vero che i rendimenti si stanno erodendo, è altrettanto vero che le condizioni per chi entra oggi sono più interessanti, anche grazie a un ridimensionamento di multipli che per lungo tempo sono stati difficili da sostenere. Nonostante questo, il mercato si sta adattando in modo costante a un contesto in cui l’energia torna a essere una variabile centrale. E quando questo accade, tutto il resto smette di essere stabile come prima. Conviene abituarsi, in fretta.