7 Explanatory Gold Charts

A speed tells us much more than just a rally, but rather deep transformation of the role of gold in the global financial system

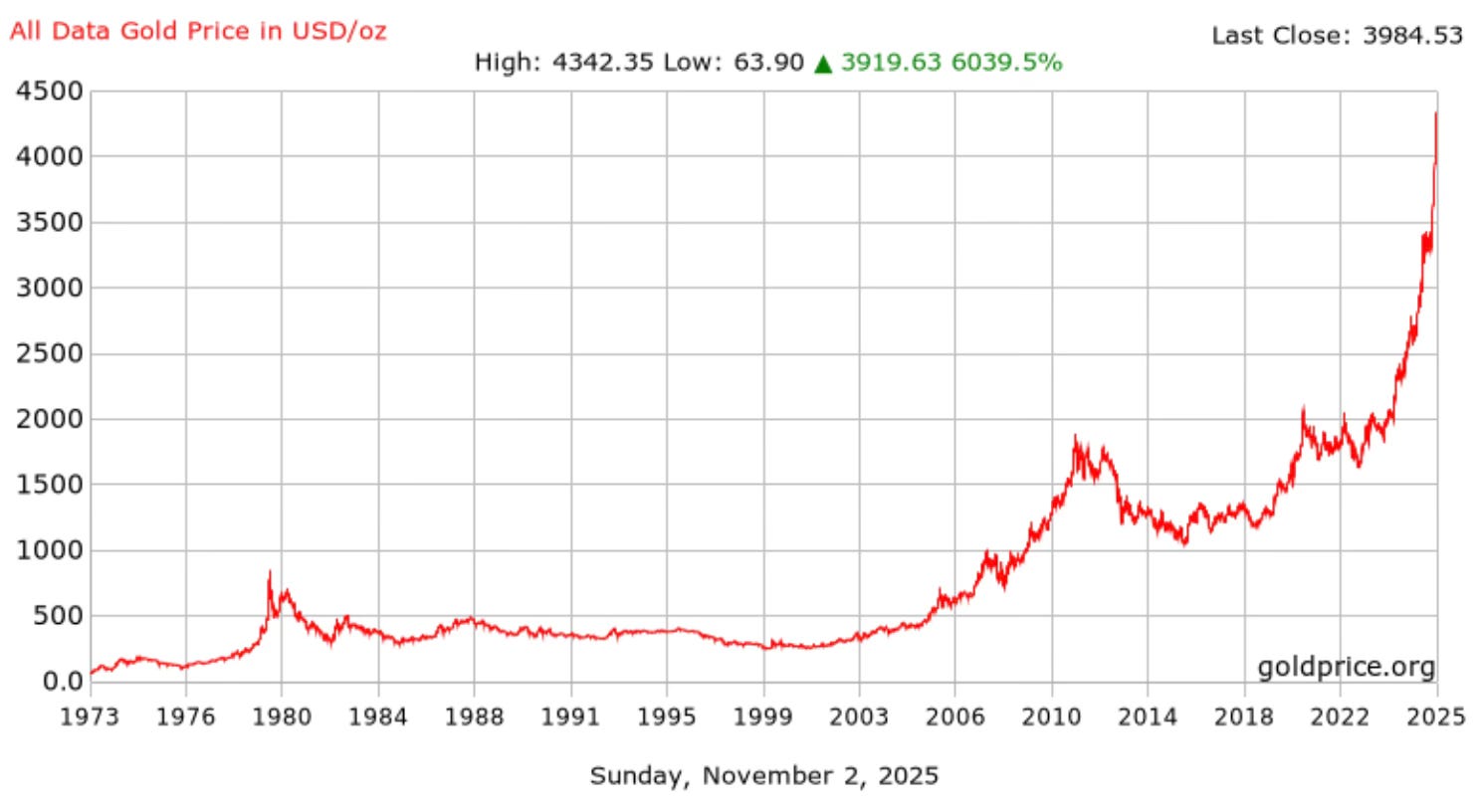

After taking 12 years to double from $1,000 to $2,000, gold doubled again in just five years, recently surpassing $4,000. Transition from $3,000 to $4,000 took just 200 days, and the jump to $4,400 took only 60. Now back to $4,000. What’s next?

It is no longer just a safe-haven asset, but a geopolitical variable, a sign of the times and a compass for navigating the monetary chaos we are experiencing. The 7 charts below should not be read as isolated images, but as chapters in the same story: return of gold to the center of the system.

Dopo aver impiegato dodici anni per raddoppiare da 1.000 a 2.000 dollari, l’oro ha raddoppiato nuovamente in soli cinque anni, superando recentemente i 4.000 dollari. Il passaggio da 3.000 a 4.000 dollari ha richiesto appena duecento giorni, e il salto a 4.400 dollari solo sessanta. Ora di nuovo a 4.000. What’s next?

Non è più solo un asset rifugio, ma una variabile geopolitica, un segnale dei tempi e una bussola per orientarsi nel caos monetario che stiamo vivendo. I sette grafici che seguono non vanno letti come immagini isolate, ma come capitoli di una stessa storia: il ritorno dell’oro al centro del sistema.

1. Gold returns to center stage: metal as a compass for the system

The first chart, the most intuitive and perhaps the most deceptive in its apparent simplicity, shows the unstoppable rise of the yellow metal in recent years. The price curve, now familiar to investors, traces the trajectory of an asset that has weathered banking crises, pandemics, wars and rate hikes without losing consistency. Gold no longer reacts to events: it anticipates them. Each acceleration tells the story of erosion of confidence in fiat money, each pause reflects the temporary illusion of stability. Market now seems to perceive gold as a moral and monetary compass, capable of measuring the growing distance between real and financial value. Today, more than ever, the precious metal represents the collective memory of a system in search of anchors.

1. L’oro torna protagonista: il metallo come bussola del sistema

Il primo grafico, quello più intuitivo e forse più ingannevole nella sua apparente semplicità, mostra l’ascesa inarrestabile del metallo giallo negli ultimi anni. La curva dei prezzi, ormai familiare agli investitori, disegna la traiettoria di un asset che ha attraversato crisi bancarie, pandemie, guerre e rialzi dei tassi, senza perdere coerenza. L’oro non reagisce più agli eventi: li anticipa. Ogni sua accelerazione racconta l’erosione della fiducia nel denaro fiat, ogni pausa riflette la temporanea illusione di stabilità. Il mercato sembra ormai percepire l’oro come una bussola morale e monetaria, capace di misurare la distanza crescente tra il valore reale e quello finanziario. Oggi, più che mai, il metallo prezioso rappresenta la memoria collettiva di un sistema in cerca di ancore.

2. The return of flows: global funds rediscover gold

The second chart reveals a crucial detail: capital flows to funds investing in physical gold have returned to positive territory after years of disinterest. The phenomenon doesn’t have characteristics of speculative trading, but rather those of a structural recomposition of global portfolios. Large managers, central banks and institutional investors seem to be reconsidering the strategic role of the metal, not as a tactical hedge, but as a core asset. In a context of persistent inflation, falling real yields and geopolitical uncertainty, gold is returning to what it has always been: the currency of those who don’t need to trust anyone. The silent but steady flows signal a change of regime. Gold is no longer a niche asset: it is back in the mainstream.

2. Il ritorno dei flussi: i fondi globali riscoprono l’oro

Il secondo grafico rivela un dettaglio cruciale: i flussi di capitale verso i fondi che investono in oro fisico sono tornati positivi dopo anni di disinteresse. Il fenomeno non ha i tratti del trading speculativo, ma quelli di una ricomposizione strutturale dei portafogli globali. I grandi gestori, le banche centrali e gli investitori istituzionali sembrano riconsiderare il ruolo strategico del metallo, non come copertura tattica, ma come asset core. In un contesto di inflazione persistente, rendimenti reali in calo e incertezza geopolitica, l’oro torna a essere ciò che è sempre stato: la valuta di chi non ha bisogno di fidarsi di nessuno. I flussi, silenziosi ma continui, segnalano un cambio di regime. L’oro non è più una nicchia: è tornato mainstream.

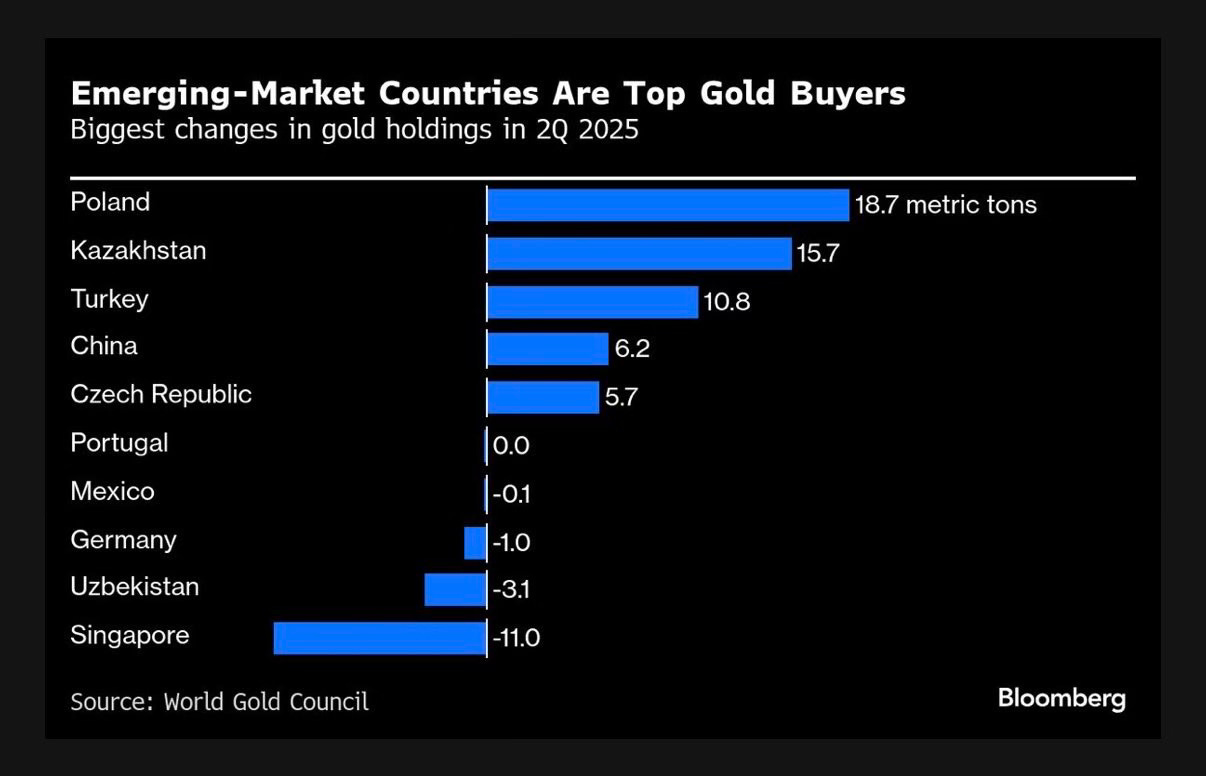

3. Physical demand rises: gold leaves London’s vaults

The third chart shows a lesser-known but highly significant phenomenon: transfer of physical gold from Western warehouses to emerging markets. For decades, London was the nerve center of the global gold market, the place that set prices and held reserves, but in recent years centrality has been eroding. A growing proportion of the gold registered in London is being withdrawn and transferred to Poland, Kazakhstan, Turkey, and China (more on this later, ed.), where demand is real, not financial. This shift is not only logistical: it is symbolic. It represents the shift in the global economic center of gravity from a system based on derivatives and futures to one based on physical delivery and actual ownership. In other words, gold is returning to where it is considered a value, not a hedge.

3. La domanda fisica sale: l’oro lascia i caveau di Londra

Il terzo grafico mostra un fenomeno meno noto ma di grande importanza: il trasferimento di oro fisico dai magazzini occidentali verso i mercati emergenti. Per decenni, Londra è stata il centro nevralgico del mercato aurifero mondiale, la piazza che decideva i prezzi e custodiva le riserve, ma da qualche anno quella centralità si sta erodendo. Una parte crescente dell’oro registrato a Londra viene ritirata e trasferita verso Polonia, Kazakistan, Turchia e Cina (ne parleremo più avanti, ndr), dove la domanda è reale, non finanziaria. Questo spostamento non è solo logistico: è simbolico. Rappresenta lo spostamento del baricentro economico globale, dal sistema basato su derivati e futures a uno basato su consegne fisiche e proprietà effettiva. In altre parole, l’oro sta tornando là dove viene considerato valore, non copertura.

4. The Asian market accelerates: China leads the new cycle

The fourth chart introduces the real turning point in this cycle: China as the engine of global gold accumulation. In recent years, Beijing has encouraged the purchase of gold not only by central bank, but also by households and businesses. The metal has entered balance sheets, savings plans and industrial strategies. Data from Swiss refineries and Hong Kong customs confirm a steady flow of bullion to China, where physical demand remains insatiable. This behavior has a clear strategic significance: gold is a hedge against dollar volatility and a bridge to the credibility of the yuan. China is not accumulating gold to protect itself: it is doing so to build the foundations of its future monetary architecture.

4. Il mercato asiatico accelera: la Cina guida il nuovo ciclo

Il quarto grafico introduce la vera svolta di questo ciclo: la Cina come motore dell’accumulazione globale di oro. Negli ultimi anni, Pechino ha incentivato l’acquisto di oro non solo da parte della banca centrale, ma anche di famiglie e imprese. Il metallo è entrato nei bilanci, nei piani di risparmio, nelle strategie industriali. I dati delle raffinerie svizzere e delle dogane di Hong Kong confermano un flusso costante di lingotti verso la Cina, dove la domanda fisica resta insaziabile. Questo comportamento ha un chiaro significato strategico: l’oro è la copertura contro la volatilità del dollaro e il ponte verso la credibilità dello yuan. La Cina non accumula oro per proteggersi: lo fa per costruire le fondamenta della sua futura architettura monetaria.

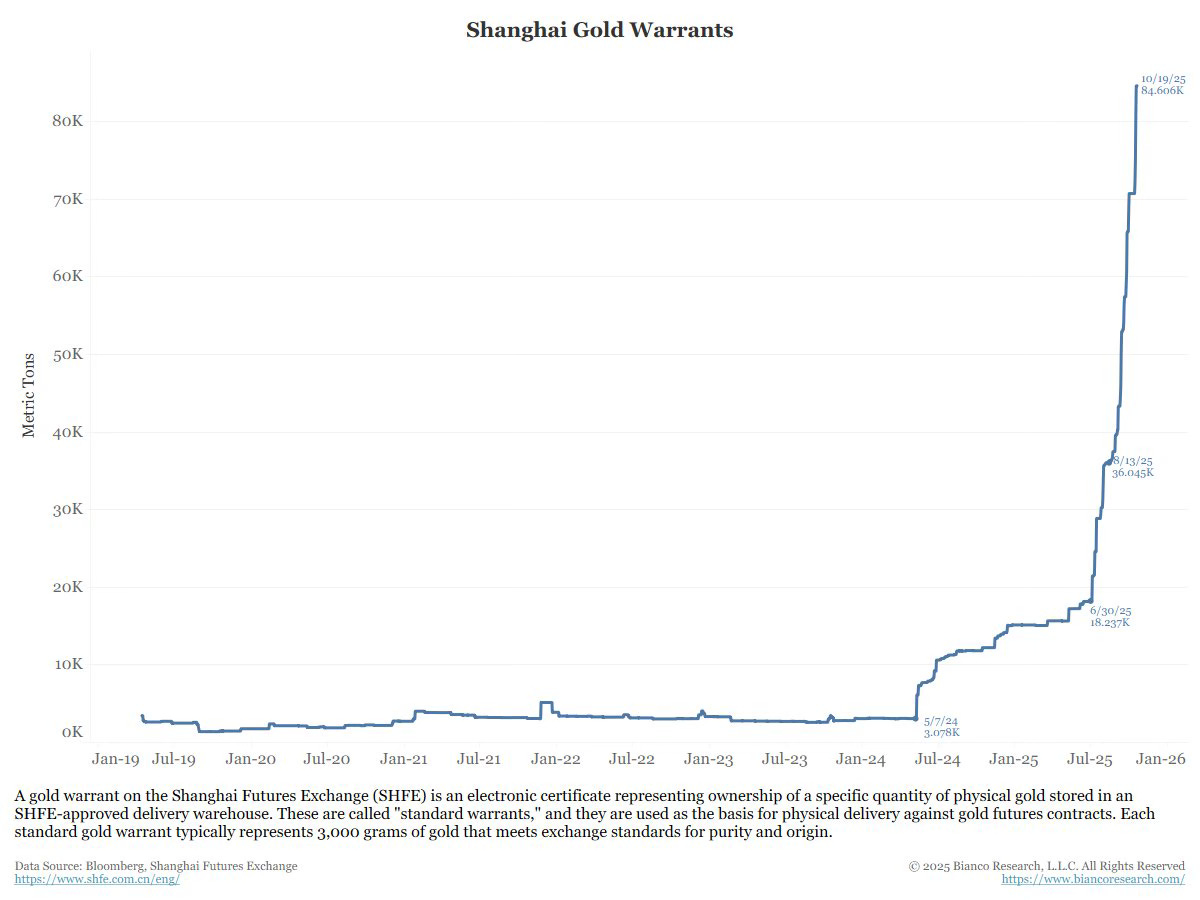

5. Shanghai Gold Warrants: the curve tells the story of new order

The fifth chart best illustrates the depth of the change. It shows the vertical explosion of Shanghai Gold Warrants, digital certificates representing ownership of physical gold held at the Shanghai Futures Exchange. Shanghai gold warrants are rising due to a combination of record demand for safe-haven assets, robust gold purchases by central banks (particularly by the People’s Bank of China, ed.) and intense price volatility that stimulates investor activity and arbitrage. Behind these numbers lies the emergence of a new real gold market, based on tangible ownership rather than derivative contracts. China is effectively building its own version of the gold clearing system, an alternative to the London one. And this is not a technical detail: it is the premise for a new monetary infrastructure, in which trust is no longer delegated but guaranteed by the metal itself.

5. Shanghai Gold Warrants: la curva che racconta il nuovo ordine

Il quinto grafico è quello che più di tutti descrive la profondità del cambiamento. Mostra l’esplosione verticale dei Shanghai Gold Warrants, i certificati digitali che rappresentano proprietà di oro fisico custodito presso la Shanghai Futures Exchange. I warrant sull’oro di Shanghai stanno aumentando a causa di una combinazione di domanda record di beni rifugio, robusti acquisti di oro da parte delle banche centrali (in particolare da parte della Banca popolare cinese, ndr) e un’intensa volatilità dei prezzi che stimola l’attività degli investitori e l’arbitraggio. Dietro questi numeri si cela la nascita di un nuovo mercato dell’oro reale, basato sul possesso tangibile e non su contratti derivati. La Cina sta di fatto costruendo la sua versione del sistema di clearing aurifero, alternativa a quello londinese. E questo non è un dettaglio tecnico: è la premessa per una nuova infrastruttura monetaria, in cui la fiducia non è più delegata ma garantita dal metallo stesso.

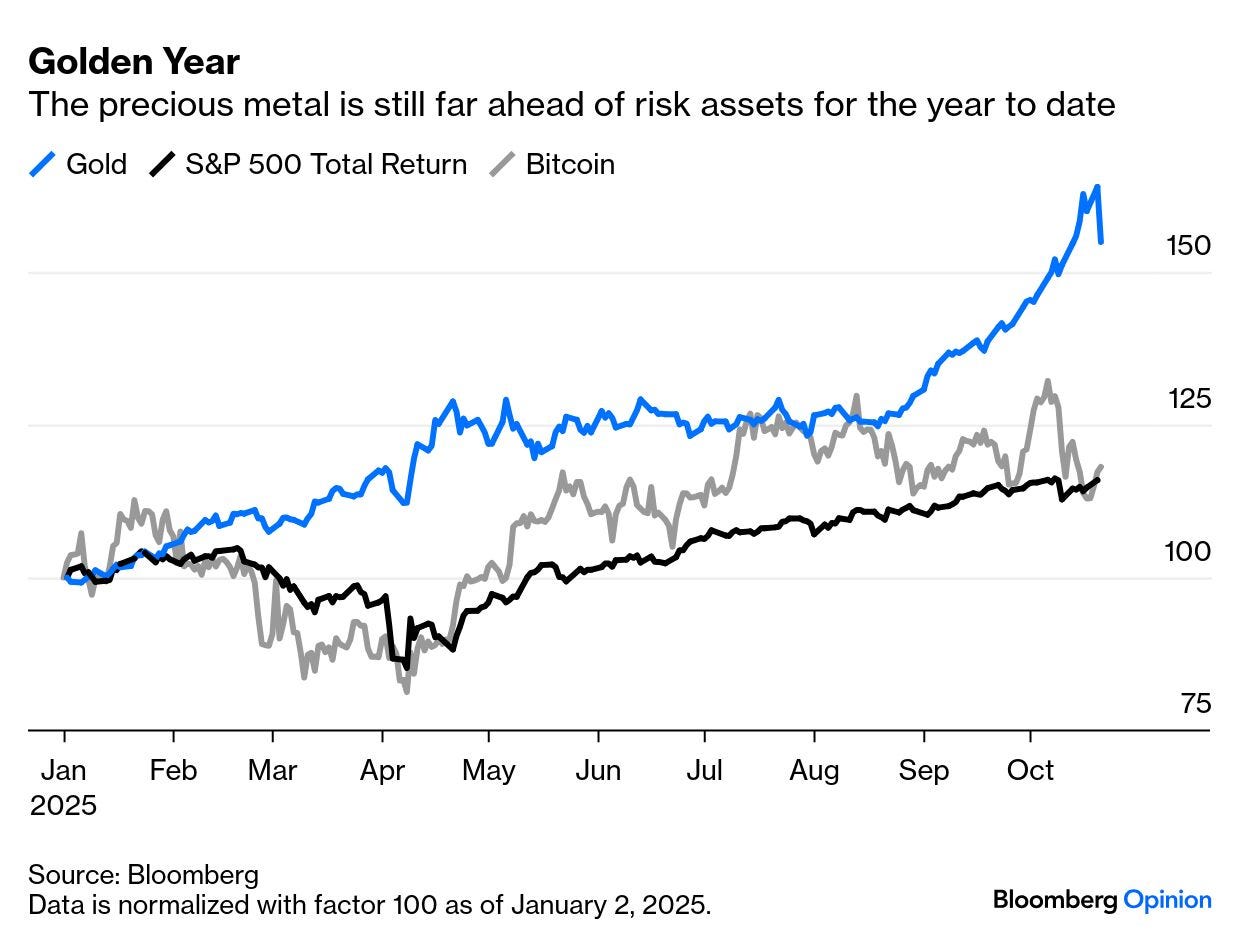

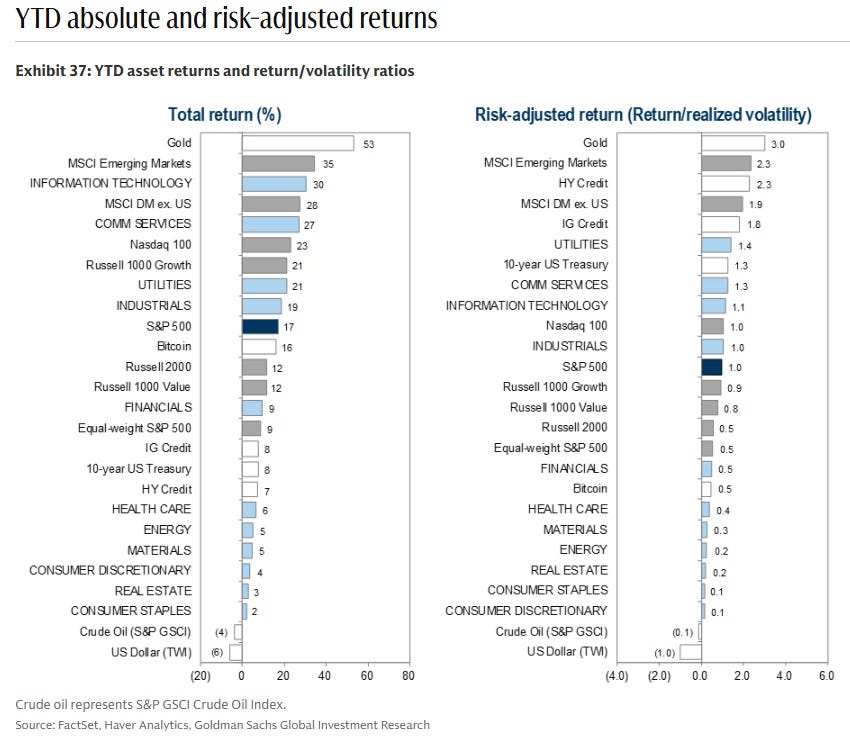

6. Gold dominates in terms of return and stability in 2025

The sixth chart shows a surprising but unequivocal fact: in 2025, gold was the asset with the best absolute performance and the best risk-adjusted return among all major global asset classes. With a total return of 53% since the beginning of the year, gold clearly outperformed US equities, emerging markets, and even the technology sector, which had dominated the last decade. Even more significant is the volatility-adjusted return indicator (return/realized volatility): with a value of 3.0, gold ranks well above all other assets, signaling not only directional strength but also stability of movement. In other words, this is not a speculative flare-up, but a solid, sustained, and steady rise. This dynamic is even more interesting when you consider that bond yields have been moving in uncertain territory, the dollar has lost ground, and Western stock markets have begun to show signs of saturation.

6. L’oro domina per rendimento e stabilità nel 2025

Il sesto grafico mostra un dato tanto sorprendente quanto inequivocabile: nel 2025, l’oro è stato l’asset con la migliore performance assoluta e il miglior rendimento corretto per il rischio tra tutte le principali classi di investimento globali. Con un total return del 53% da inizio anno, l’oro ha superato nettamente l’azionario americano, i mercati emergenti e persino il settore tecnologico, che pure aveva dominato l’ultimo decennio. Ancora più significativo è l’indicatore di rendimento aggiustato per la volatilità (return/realized volatility): con un valore di 3.0, l’oro si colloca ben al di sopra di tutti gli altri asset, segnalando non solo forza direzionale, ma anche stabilità del movimento. Questa dinamica è ancor più interessante se si considera che i rendimenti obbligazionari si sono mossi in territorio incerto, il dollaro ha perso terreno e le borse occidentali hanno iniziato a mostrare segni di saturazione.

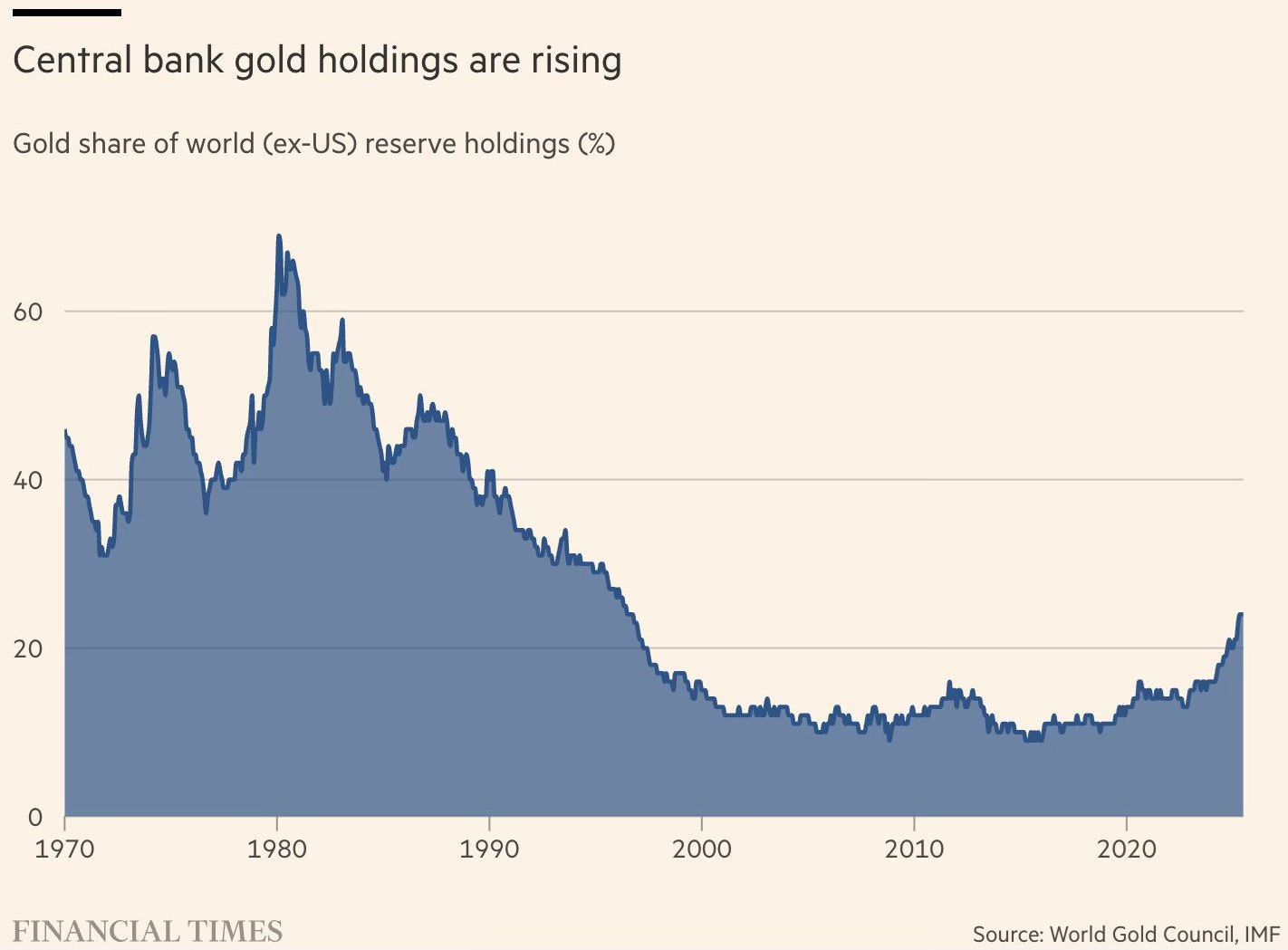

7. Central banks are returning to gold

The last chart closes the circle with a signal that goes beyond the market and touches on the monetary sphere: gold reserves of central banks (excluding the United States) have returned to their highest levels in over thirty years. After a long decline that began in the 1980s, when confidence in the dollar and government bonds seemed sufficient to guarantee systemic stability, the share of gold held as reserves has returned to strong growth. Today, the percentage of global reserves allocated to gold is once again approaching 30%, a level not seen since the immediate aftermath of the end of Bretton Woods. This is not an escape from the system, but a silent realignment of its pillars: a slow return to substance in an era dominated by leverage and digital trust.

7. Le banche centrali stanno tornando all’oro

L’ultimo grafico chiude il cerchio con un segnale che va oltre il mercato e tocca la sfera monetaria: le riserve auree delle banche centrali (esclusi gli Stati Uniti) sono tornate ai massimi da oltre trent’anni. Dopo un lungo declino iniziato negli anni Ottanta, quando la fiducia nel dollaro e nelle obbligazioni governative sembrava sufficiente a garantire stabilità sistemica, la quota di oro detenuta come riserva è tornata a crescere in modo deciso. Oggi, la percentuale di riserve mondiali allocate in oro si avvicina di nuovo al 30%, un livello che non si vedeva dai tempi immediatamente successivi alla fine di Bretton Woods. Non è una fuga dal sistema, ma un riassetto silenzioso dei suoi pilastri: un lento ritorno alla sostanza in un’epoca dominata dalla leva e dalla fiducia digitale.

Conclusion: the role of gold in future portfolios

The return of gold to the center of global strategies is not just an emotional or cultural reflex: it is a rational response to a hyper-indebted, fragile and increasingly polarized financial system. Its value today is measured not only in dollars per ounce, but in its ability to represent a form of financial independence. For those building diversified portfolios, gold remains a pillar of balance. In this sense, the Permanent Portfolio, with its logic of balancing stocks, bonds, cash, and gold, offers an interesting starting point. Not as dogma, but as a flexible architecture capable of adapting to the cycles of economic history. Within that structure, gold continues to play its original role: not as a gamble, but as a foundation.

Conclusione: il ruolo dell’oro nei portafogli del futuro

Il ritorno dell’oro al centro delle strategie globali non è soltanto un riflesso emotivo o culturale: è una risposta razionale a un sistema finanziario iperindebitato, fragile e sempre più polarizzato. Il suo valore oggi non si misura solo in dollari per oncia, ma nella sua capacità di rappresentare una forma di indipendenza patrimoniale. Per chi costruisce portafogli diversificati, l’oro resta un pilastro di equilibrio. In questo senso, il Portafoglio Permanente, con la sua logica di bilanciamento tra azioni, obbligazioni, liquidità e oro, offre un punto di partenza interessante. Non come dogma, ma come architettura flessibile, capace di adattarsi ai cicli della storia economica. L’oro, all’interno di quella struttura, continua a svolgere il suo ruolo originario: non quello di scommessa, ma di fondamento.

The acceleration in Gold has been nothing short of breathtaking in the past two years. It's basically what every "Gold Bug's" fever dream was since 2008. Sometimes things take way longer to unfold, but then they unfold in a hockey stick-like manner.

That Shanghai chart is important, and also don't forget that the PBC does not report their Gold purchases openly & correctly.

They will hold more in their vaults nowadays than visible in your chart #2, probably even much more judging by Gold outflows in COMEX.

The Gold holdings are just a sign that trust is lost and this is accelerating with Trump's trade wars (as is DXY decelerating since then).

I am just writing a 4-part series where Gold plays an essential role to explain things for anyone who wants to read some general primers - (Part 1 & 2 are live, 3 coming this Friday, 4 next week)

Part 2 - The Rise and Fall of Money:

https://substack.com/@realmontycarlo/p-177375623

Equity Management Associates thinks gold could go to $30 K an ounce in a “monetary panic”. https://substack.com/home/post/p-177825737